Get Trs Qpp Loan Application Form

The Trs QPP Loan Application form plays a crucial role for individuals seeking to borrow against their Qualified Pension Plan (QPP) accumulations. This comprehensive application process is tailored for ensuring members can smoothly request funds from their pension accounts, but it's emphasized that this step should be taken after thorough consideration and understanding of the terms and conditions as outlined in the QPP Loans brochure. Applicants are urged to provide accurate and complete information to avoid any delays, including the initialing of any amendments made on the form. Interestingly, the process provides an online alternative for loan applications, although specific scenarios, such as borrowing in conjunction with retirement, still require the traditional paper submission. The procedure further outlines cancellation policies, eligibility for electronic fund transfers (EFT) for loan receipt, and the cross-impact of other loan amounts, like those from a Tax-Deferred Annuity (TDA) Program, on the potential QPP loan amount. Additionally, it mentions the IRS’s regulations regarding loan balances and the nuanced options for loan disbursement. Special attention is given to members close to retirement, specifying how loans at this stage are treated differently in terms of repayment and taxation. The importance of providing all requested details and adhering to deadlines is underscored, alongside the necessity of the form’s notarization to ensure the applicant’s identity and the legitimacy of the request. With various parts dedicated to differing member statuses and intentions, the application is designed to cater to a wide range of needs and circumstances, making it a vital tool for financial planning within the sphere of pension benefits.

Trs Qpp Loan Application Example

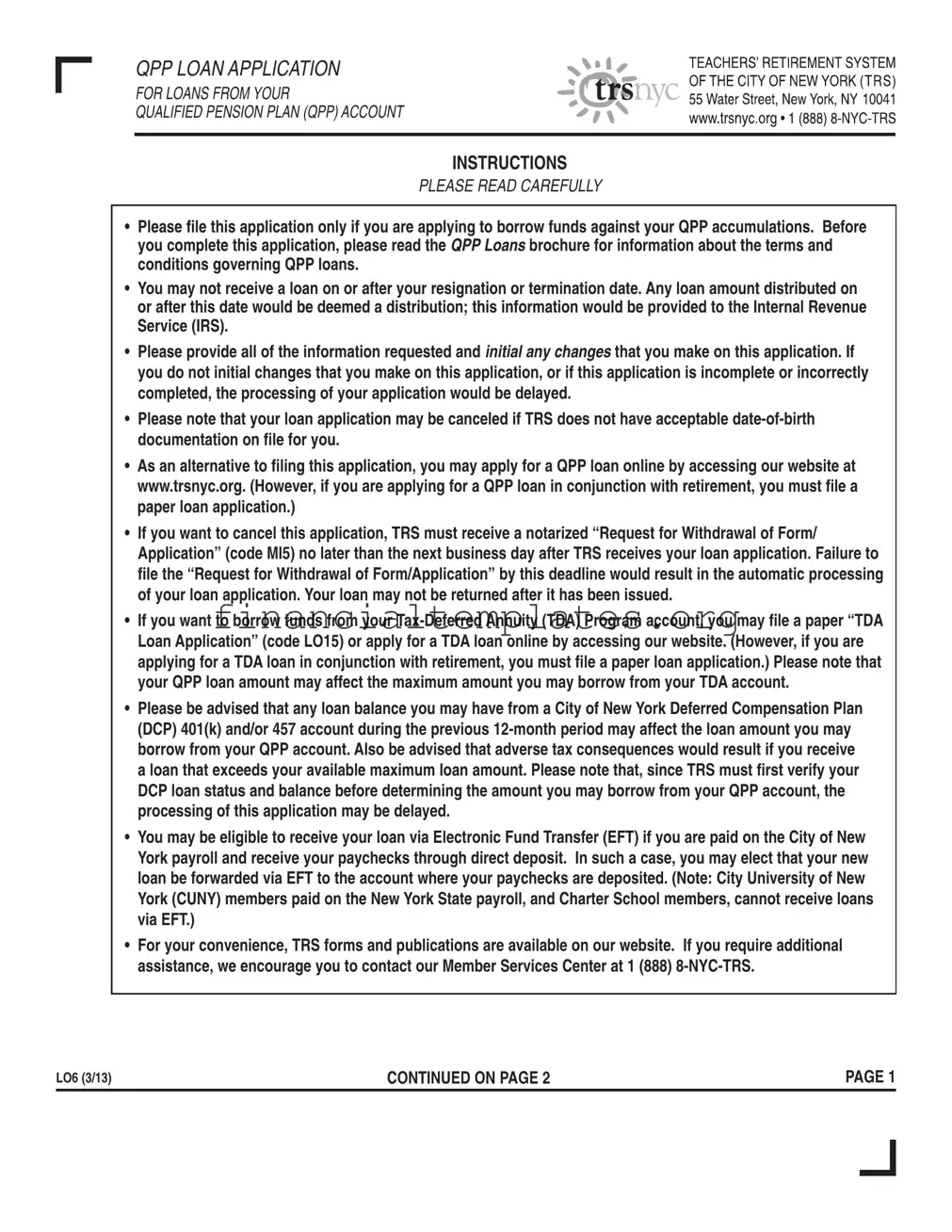

QPP LOAN APPLICATION

FOR LOANS FROM YOUR

QUALIFIED PENSION PLAN (QPP) ACCOUNT

INSTRUCTIONS

PLEASE READ CAREFULLY

•PleaseilethisapplicationonlyifyouareapplyingtoborrowfundsagainstyourQPPaccumulations.Before youcompletethisapplication,pleasereadtheQPP Loansbrochureforinformationaboutthetermsand conditionsgoverningQPPloans.

•Youmaynotreceivealoanonorafteryourresignationorterminationdate.Anyloanamountdistributedon orafterthisdatewouldbedeemedadistribution;thisinformationwouldbeprovidedtotheInternalRevenue Service(IRS).

•Pleaseprovidealloftheinformationrequestedandinitial any changesthatyoumakeonthisapplication.If youdonotinitialchangesthatyoumakeonthisapplication,orifthisapplicationisincompleteorincorrectly completed,theprocessingofyourapplicationwouldbedelayed.

•Asanalternativetoilingthisapplication,youmayapplyforaQPPloanonlinebyaccessingourwebsiteat www.trsnyc.org.(However,ifyouareapplyingforaQPPloaninconjunctionwithretirement,youmustilea paperloanapplication.)

•Ifyouwanttocancelthisapplication,TRSmustreceiveanotarized“RequestforWithdrawalofForm/ Application”(codeMI5)nolaterthanthenextbusinessdayafterTRSreceivesyourloanapplication.Failureto ilethe“RequestforWithdrawalofForm/Application”bythisdeadlinewouldresultintheautomaticprocessing ofyourloanapplication.Yourloanmaynotbereturnedafterithasbeenissued.

•PleasebeadvisedthatanyloanbalanceyoumayhavefromaCityofNewYorkDeferredCompensationPlan

•YoumaybeeligibletoreceiveyourloanviaElectronicFundTransfer(EFT)ifyouarepaidontheCityofNew Yorkpayrollandreceiveyourpaychecksthroughdirectdeposit.Insuchacase,youmayelectthatyournew loanbeforwardedviaEFTtotheaccountwhereyourpaychecksaredeposited.(Note:CityUniversityofNew York(CUNY)memberspaidontheNewYorkStatepayroll,andCharterSchoolmembers,cannotreceiveloans viaEFT.)

•Foryourconvenience,TRSformsandpublicationsareavailableonourwebsite.Ifyourequireadditional

LO6 (3/13) |

CONTINUEDONPAGE2 |

PAGE 1 |

CONTINUEDFROMPAGE1

InPartA: All information must be provided.

InPartB:

1)Please indicate the amount you want to borrow. You may specify a dollar amount or write “maximum” to borrow the maximum loan amount available to you. PleasenotethatthemaximumamountyoumayrequestforaQPPloanatretirementis 75%ofyouraccumulatedcontributions(includingthebalanceintheemployeeportionofyourAdditionalMember Contributions(AMCs),ifapplicable);additionalrestrictionsonloanamountsapplytoloansformemberswhoare notretiringandmembersonaleaveofabsence.PleaseseetheQPP Loansbrochureformoreinformation. In addition, if your requested loan amount exceeds your maximum QPP loan amount, you must elect whether to receive the maximum QPP loan amount available to you or have your application canceled.

Note:IRS regulations do not allow outstanding loan balances to be combined with new loans. Any new loan

requested would be treated as a separate loan, and each loan balance would be subject to the interest, applicable insurance charges, and repayment terms in effect when the loan is issued.

2)You must elect the repayment period for your QPP loan (unless you are filing for a QPP loan in conjunction with retirement).

3)You must elect how you would like your loan disbursed. (Please note that loan checks may no longer be placed on hold for pickup at TRS.) If you are paid on the City of New York payroll and receive your paychecks through direct deposit, you may be eligible to have your QPP loan forwarded via EFT to the account where your paychecks are deposited. If you cannot receive your QPP loan via EFT (e.g., you are not paid on the City of New York payroll, you do not receive paychecks through direct deposit, or TRS is unable to confirm the applicable bank account information on file), your loan check will be mailed to your home address.

Note:In order for a loan check to be mailed to your home address or forwarded via EFT on a given Wednesday, TRS must generally receive your loan application by the close of business on Wednesday of the preceding week; the funds would be available on Fridays. (If a holiday occurs during a given week, TRS must receive your loan application by the first business day of that week.) However, checks for loans taken in conjunction with retirement are normally issued the third Wednesday after your effective retirement date.

4)You must provide additional information if you are on a leave of absence without pay.

InPartC: You must complete this part ONLY if you are a Tier I or II member, and you have applied for an excess withdrawal. Please note that an excess withdrawal may affect the loan amount for which you are eligible.

InPartD: You must complete this part ONLY if you are filing this application for a QPP loan taken in conjunction with retirement.

Please be advised that TRS must receive this application no later than one business day before your effective retirement date, and that your loan taken in conjunction with retirement would be distributed after your effective retirement date. (Ifthisapplicationisnot precededbyoriledinconjunctionwithanapplicationforretirement,yourloanwouldbesubjecttothesamerestrictions thatapplytomemberswhoarenotretiring.)

1)QPP loans at retirement are not repaid to TRS. Instead, they would be treated as taxable distributions (unless you receive a distribution of

2)You must elect how your QPP loan at retirement will be distributed. Distribution methods include Direct Cash Payment (i.e., funds that TRS distributes directly to you by mail or via EFT) and Direct Rollover (i.e., funds that TRS pays directly to one or more eligible Individual Retirement Accounts (IRAs) or other successor program(s) that you designate).

LO6 (3/13) |

CONTINUEDONPAGE3 |

PAGE2 |

CONTINUEDFROMPAGE2

3)IRSregulationsrequireTRStowithhold20%ofanytaxableloanamountthatyoudonotdirectlyrollovertoan eligibleIRAorothersuccessorprogram(s). The withheld amount would be sent to the IRS as a credit toward your federal income taxes for the year of distribution. If you receive a Direct Cash Payment, you may elect to roll over any taxable portion of the amount you receive, or roll over an amount equal to the entire taxable distribution, by replacing the amount withheld by TRS with funds from another source; however, this rollover must occur within 60 days of notification by TRS.

4)If you currently have an outstanding QPP loan balance, TRS is required to withhold an amount equaling 20% of the taxable portions of your existing loan balance and of your new loan amount that you do not instruct us to directly roll over to one or more eligible IRAs or other successor program(s). If you elect to receive your loan taken in conjunction with retirement as a Direct Cash Payment, the withholding from the prior outstanding loan must be taken, even if all or part of the new loan is

5)The minimum amount that TRS will directly roll over to a successor program is $200. (Thisamountmaybegreater, dependingonthesuccessorprogram’sminimumrequirements;anydesignatedDirectRolloveramountthatdoes notmeetthesuccessorprogram’sminimumrequirementswillbesentdirectlytoyouasaDirectCashPayment, lessanyrequiredwithholding.) Any payment less than $200 will be sent directly to you and will not be subject to the 20% withholding.

6)Any amount that is distributed through a Direct Rollover is not taxable until it is received as income and is not subject to any withholding.

7)If you are eligible to receive

InPartE: You must sign and date this application in the presence of a notary public, who must then complete Part F.

InPartF: You must have this application notarized.

LO6 (3/13) |

CONTINUEDONPAGE4 |

PAGE 3 |

Thispageintentionallyleftblank.

LO6 (3/13) |

CONTINUEDONPAGE5 |

PAGE4 |

QPP LOAN APPLICATION

FOR LOANS FROM YOUR

QUALIFIED PENSION PLAN (QPP) ACCOUNT

Pleasereadtheinstructionsbeforecompletingthisapplication.

(NOTE:Pleaseprintinblackorblueink,andinitialanychangesthatyoumakeonthisapplication.)

PARTA: All information must be provided.

|

First Name |

|

MI Last Name |

Social Security Number (last 4 digits only) |

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

X |

|

X |

|

X |

|

|

|

|

X |

|

X |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

Permanent Home Address |

|

|

|

|

|

|

|

|

|

Apt. No. |

TRS Membership Number |

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

State Zip Code |

Primary Phone Number (Check one: |

|

Home |

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

|

|

|

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Alternate Phone Number (Check one: |

|

|

Home |

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

|

|

|

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Work

Work

Mobile)

Mobile)

Please keep your personal information with TRS up to date. We will update our records based on the information you provide above, so do not enter a temporary address; instead, TRS suggests that you consult the U.S. Postal Service about having your mail forwarded on a temporary basis. To register any changes to your permanent address (and/or phone number), please access our website or file a “Member’s Change of Address Form” (code DM13) with TRS.

If you are providing new information above, please indicate the effective date:

PARTB:Please provide all applicable information below.

Please indicate the QPP loan amount you are requesting to borrow, or write “maximum” to request the maximum QPP loan amount available to you:

$

If you specified a dollar amount (rather than writing “maximum”), please write the requested amount on the line below. For example, if you want to borrow $1,000, please write “One Thousand Dollars.”

___________________________________________________

Please choose ONE of the following options and write your initials in the space provided.

____

____

I elect to receive the maximum QPP loan amount available to me if the requested QPP loan amount specified above is greater than my maximum available QPP loan amount.

I elect to have my loan application canceled if the requested QPP loan amount specified above is greater than my maximum available QPP loan amount.

LO6 (3/13) |

CONTINUEDONPAGE6 |

PAGE5 |

CONTINUEDFROMPAGE5

Please indicate your loan repayment period (if applicable):

Months

If you are a Tier I or II member, your repayment period may not exceed 48 months. If you are a Tier III, IV, or VI member, your repayment period may not exceed 60 months.

Please select how you would like to receive your QPP loan. In order to elect EFT, you must receive your paychecks through direct deposit:

by Mail address.)

by Mail address.)

via EFT (If you are ineligible to receive your loan via EFT, your loan check would be mailed to your home

Are you on a leave of absence without pay? Yes

No

If you are on a leave of absence, when did your leave of absence begin? (M/D/Y)

If you are on a leave of absence, you would automatically receive a

If you would prefer to begin making payments immediately, please check this box:

PART C: Please complete the following ONLY if you are a Tier I or II member.

Have you filed for an excess withdrawal within the last six months? Yes

No

If you checked “Yes,” please indicate the date that you filed for an excess withdrawal: (M/D/Y)

PARTD: Please complete the following ONLY if you are filing this application for a QPP loan in conjunction with retirement. TRSmust receivethisapplicationnolaterthanonebusinessdaybeforeyoureffectiveretirementdate.

Do you want your loan to be limited to the amount of your

No

Please note that, under IRS regulations, your

Please indicate your effective retirement date: (M/D/Y)

Please choose ONE of the following options and write your initials in the space provided.

_____

_____

LO6 (3/13) |

CONTINUEDONPAGE7 |

PAGE 6 |

CONTINUEDFROMPAGE6

PARTE: Please read the following statement and sign and date below in the presence of a notary.

I confirm that I have read the QPP Loans brochure and that I understand the terms and conditions of this loan. I certify that all of the information presented on this application is accurate, that I am in active service or on a leave of absence, and that I am not precluded by any court from borrowing against my QPP accumulations. I am aware that any loan balance I may have from a City of New York DCP account during the previous

MEMBER’S SIGNATURE __________________________________________________ DATE (M/D/Y) ________________

PARTF:TO BE COMPLETED BY A NOTARY (NOTE: Attestation made outside the U.S. must be executed before an American consul.)

State of ____________________________ )

)s.s.:

County of __________________________ )

On the _______________ day of __________________________, __________, before me personally appeared the person

known to me to be ____________________________________________________________________________________,

the individual who executed the foregoing instrument and acknowledged to me that (s)he executed the same. Signature: _______________________________________________________

Official Title: ______________________________________________________

Expiration Date of Commission: ______________________________________

LO6 (3/13) |

PAGE7 |

|

|

Document Specifics

| Fact Name | Description |

|---|---|

| Eligibility for Loan Application | Applicants can only apply for a QPP loan if they are borrowing against their QPP accumulations and must not apply if they are resigning or have been terminated, as such situations turn the loan into a distribution subject to IRS reporting. |

| Application Completion Requirements | All requested information must be provided, and any changes made on the application must be initialed. Incomplete or incorrectly completed applications will delay processing. |

| Loan Disbursement Options | Applicants eligible for EFT due to being on the City of New York payroll and receiving paychecks through direct deposit can opt for this disbursement method. Others will receive the loan check by mail. |

| Notarization Requirement | The application must be signed and dated in the presence of a notary public, who then completes a necessary part of the application to validate it. |

Guide to Writing Trs Qpp Loan Application

Filling out the QPP Loan Application is a process that allows you to request a loan from your Qualified Pension Plan (QPP) accumulations. This step should be taken with consideration of the terms, conditions, and potentially changing your retirement or financial planning. Before starting, make sure you've read the QPP Loans brochure thoroughly to understand the implications of taking out a loan against your QPP accumulations. Let's break down the steps needed to complete the application:

- Gather all necessary information, including your social security number (last 4 digits), permanent home address, TRS membership number, and primary and alternate phone numbers.

- On Part A: Fill in your first name, middle initial (MI), last name, and the other requested personal information. Remember to use black or blue ink and to initial any changes you make on the application.

- In Part B, indicate the amount you wish to borrow by either specifying a dollar amount or writing "maximum" to borrow the highest amount available to you.

- If specifying a dollar amount, also write out the amount in words.

- Choose whether to receive the maximum loan amount available if your requested amount exceeds your maximum available loan amount, or to have your application canceled under these circumstances. Initial your choice.

- Select the repayment period for your QPP loan, unless you're applying in conjunction with retirement.

- Choose your preferred method of loan disbursement. If you're eligible for Electronic Fund Transfer (EFT) and prefer this method, indicate so. Otherwise, confirm your mailing address for the check.

- If you're on a leave of absence without pay, provide the additional required information.

- If you're a Tier I or II member applying for an excess withdrawal, complete Part C.

- If the application is for a QPP loan taken in conjunction with retirement, complete Part D. This includes deciding on the distribution method for your QPP loan at retirement.

- Sign and date the application in the presence of a notary public (Part E).

- Have the application notarized (Part F).

After submitting your application, it's important to remember a few next steps. Should you need to cancel your application, make sure TRS receives a notarized “Request for Withdrawal of Form/Application” by the next business day after submission. Meanwhile, it's wise to keep a copy of your completed form for your records and monitor your loan disbursement according to the method you selected. If any issues arise or if you have questions, don't hesitate to contact TRS for assistance.

Understanding Trs Qpp Loan Application

Who is eligible to apply for a QPP loan?

Individuals eligible to apply for a Qualified Pension Plan (QPP) loan include members who are actively contributing to their QPP account and have not reached their resignation or termination date. It's crucial to verify your eligibility by confirming your active participation and ensuring that the Teachers Retirement System (TRS) has the correct date-of-birth documentation on file for you.

Can I apply for a QPP loan online?

Yes, you can apply for a QPP loan online by visiting the official TRS website, except in cases where you are applying in conjunction with retirement. For those specific scenarios, a paper loan application must be filed. Applying online is a convenient and efficient way to submit your application.

What information do I need to provide on the loan application?

All sections of the QPP loan application must be completed accurately. This includes providing your requested loan amount, choosing your repayment period (unless you are applying in conjunction with retirement), and deciding on the preferred method of loan disbursement. Remember, any changes made on the application must be initialed, and the form needs to be signed in the presence of a notary public.

How much can I borrow from my QPP account?

The maximum loan amount you can request is typically 75% of your accumulated contributions, including balances in the employee portion of your Additional Member Contributions (AMCs) if applicable. However, restrictions apply for members not retiring, and those on a leave of absence. The exact amount available may vary depending on other factors like outstanding loan balances from other plans within the previous 12-month period.

What happens if I resign or terminate my employment?

If you resign or terminate your employment, you cannot receive a loan from your QPP account. Any loan amount distributed on or after your resignation or termination date would be considered a distribution and reported to the Internal Revenue Service (IRS).

What are the tax implications of receiving a QPP loan?

Loans from your QPP account are subject to specific tax rules. If you take a loan and the amount exceeds your available maximum loan amount, adverse tax consequences may apply. Additionally, for loans taken at retirement, there are certain withholdings by TRS that may also affect your tax situation. It's advisable to consult with a tax professional regarding these matters.

Can my QPP loan be canceled once it's processed?

If you decide to cancel your QPP loan application, TRS must receive a notarized “Request for Withdrawal of Form/Application” no later than the next business day after your application was received. Once a loan has been issued, it cannot be returned, highlighting the importance of being certain about your loan request before submission.

How is the loan disbursed?

Loan disbursements are typically handled either through mailing a check to your home address or via Electronic Fund Transfer (EFT) directly to a bank account if you are eligible. The eligibility for EFT depends on being paid on the City of New York payroll and receiving paychecks through direct deposit among other factors.

What if I'm on a leave of absence?

If you are on a leave of absence without pay, you must provide additional information on your loan application. This ensures that TRS can accurately assess your loan request considering your current employment status.

How soon will the funds be available after applying?

For the loan check to be mailed or forwarded via EFT, TRS generally needs to receive your application by the close of business on Wednesday of the preceding week, with funds available on Fridays. However, this timeline may vary, especially around holidays, and for loans taken in conjunction with retirement, which are usually issued the third Wednesday after your effective retirement date.

Common mistakes

-

Not reading the instructions carefully. Many applicants rush to fill out the form without taking the time to go through the instructions provided at the beginning of the application. This mistake can lead to misunderstanding the requirements, which may include essential details about the terms and conditions of the loan, eligibility criteria, and the documentation needed for the loan process. It is crucial to read these instructions carefully to ensure compliance and to understand the borrowing terms fully.

-

Failing to initial changes. When applicants make corrections or changes on the application form, they often forget to initial these changes as instructed. This oversight can lead to delays in the processing of the application because any uninitialed alterations might not be acknowledged by the reviewing authority, resulting in requests for clarification or the need to resubmit the form. Marking changes with initials is a simple step that ensures the application is processed efficiently and correctly reflects the applicant’s current information and requests.

-

Applying for the wrong loan type. Individuals may apply for a QPP loan when they intend to borrow funds from their Tax-Deferred Annuity (TDA) Program account, or vice versa, due to not understanding the differences between the two loan options. This mistake can result from not thoroughly reading the application’s instructions or not visiting the recommended website for more information. Knowing the specific loan type applicable to one's needs and applying correctly is essential to access the intended funds.

-

Requesting an incorrect loan amount. It is common for applicants to request a loan amount without knowing their maximum eligible amount, leading to applications for amounts either too low or exceeding their eligibility. This mistake can be avoided by specifying "maximum" to borrow the maximum amount available or by calculating the eligible amount based on the guidelines provided in the instructions. Incorrect loan amount requests result in delays or the need for adjustments, prolonging the time to receive the loan.

-

Not providing necessary information for loan disbursement. Applicants sometimes overlook or incorrectly fill out the section of the application concerning loan disbursement. This includes failing to indicate their preference for receiving the loan, such as through direct deposit or by mail, and not specifying the correct account information for Electronic Fund Transfer (EFT), if eligible. Ensuring all required disbursement information is correctly provided and matches the applicant's records is critical for the timely and accurate reception of loan funds.

By avoiding these common mistakes, individuals applying for a QPP loan can streamline the process, ensuring they meet all requirements and receive their funds in a timely manner. Attention to detail and a thorough understanding of the application instructions go a long way in achieving a smooth loan application experience.

Documents used along the form

Filing a QPP Loan Application is a significant step toward managing your finances, using your Qualified Pension Plan (QPP) accumulations smartly. However, it's often just one part of a broader financial or retirement strategy. Other forms and documents frequently accompany the QPP Loan Application, each serving a specific purpose in ensuring that your financial or retirement plan is comprehensive and tailored to your needs. Understanding these documents can help you navigate through the process more effectively.

- TDA Loan Application (code LO15): For individuals seeking to borrow from their Tax-Deferred Annuity (TDA) Program. This is another option for accessing funds, which may be influenced by the amount you borrow against your QPP.

- Member’s Change of Address Form (code DM13): Essential for updating your address and contact information with TRS. It ensures all correspondence and important documents reach you without delay.

- Request for Withdrawal of Form/Application (code MI5): If you change your mind about a loan application you've submitted, this form allows you to officially withdraw your application within a specified timeframe to prevent processing.

- Beneficiary Designation Form: This document lets you designate or change the beneficiary(ies) for your pension benefits, ensuring that your benefits are directed according to your wishes in the event of your death.

- Direct Deposit Authorization: Authorizes TRS to deposit your funds directly into your bank account, offering a convenient and secure way to receive your loan or other distributions.

- Loan Repayment Option Form: Allows you to select or change your repayment plan for your QPP or TDA loan, giving you flexibility to manage your repayment terms based on your financial situation.

- Application for Retirement: For those transitioning to retirement, this form initiates the process of calculating and receiving retirement benefits. It's critical for members who are applying for a loan in conjunction with retirement.

- IRS Form W-4P: Used to determine the correct amount of federal income tax to be withheld from your pension or annuity payments, including distributions from loans taken at retirement.

- Proof of Birth Documentation: Required to verify your age for retirement eligibility, loan applications, and ensuring accurate records for retirement benefits.

Navigating through loans and retirement planning involves considerable paperwork, but understanding these documents simplifies the process. Whether you're applying for a QPP loan, updating personal information, or planning for retirement, each document plays a vital role. They collectively ensure your financial strategies align with your goals, providing security and peace of mind for your future.

Similar forms

The Trs Qpp Loan Application form shares similarities with the 401(k) Loan Application, mainly in purpose and structure. Both forms are designed for individuals to borrow against their retirement savings, whether that's a Qualified Pension Plan (QPP) or a 401(k) plan. Applicants must provide personal information, loan amount desired, and repayment terms. The significance of accurate and complete information is emphasized in both to prevent processing delays. Furthermore, both applications underline the tax implications and repayment rules specific to their respective plans.

Another analogous document is the Mortgage Loan Application, commonly known as the Uniform Residential Loan Application. This similarity lies in the comprehensive financial detail required from the applicant, aiming to assess borrowing eligibility. Although one pertains to housing loans and the other to pension plan loans, both demand an extensive rundown of the borrower's financial health, including income, debts, and creditworthiness. Each form ultimately serves to evaluate whether the applicant qualifies for the loan under consideration.

The Home Equity Line of Credit (HELOC) Application also mirrors the Trs Qpp Loan Application in several respects. Both allow applicants to tap into a pre-existing asset for a loan – for the HELOC, it's the home's equity, and for the QPP loan, it's the accumulated pension funds. The requirement to specify the loan amount requested, decide on repayment options, and potential tax implications are pertinent parts of both applications. The decisive nature of specifying the amount reflects the borrower's intent to manage financial demands effectively.

Similarly, the Personal Loan Application from banks or financial institutions shares characteristics with the QPP loan form. Despite the differing sources of funds (personal savings versus pension accumulations), applicants must disclose personal and financial details to obtain approval. Both types of loans may specify the intended use of the funds, underlining the importance of the loan purpose. The emphasis on accurate completion to avoid processing delays is a common thread.

The Credit Card Application process, though generally more streamlined, shares the essence of evaluating an individual's creditworthiness and financial stability with the QPP loan application. Both inquire about the applicant's financial background, albeit for different end purposes: one for immediate financial credit and the other for retirement savings advancement. The assessment criteria in both aim to mitigate risk for the lender or plan administrator.

The Business Loan Application can be compared to the QPP loan form in regards to the level of detail required about the applicant's financial status. While the latter concerns an individual's retirement funds, the former is about a business's financial health. Both require a thorough examination of financial stability and the capacity to repay the borrowed amounts. Detailed financial information paves the way for assessing the feasibility of loan approval.

The Student Loan Application process is parallel in its requirement for detailed personal and financial information to ensure the applicant's eligibility for loan approval. Just as the QPP loan application evaluates an individual's standing and repayment terms, so does the student loan process, albeit focused on educational funding. The emphasis on understanding the loan terms and conditions before proceeding is crucial in both scenarios.

Car Loan Applications also align with the QPP loan form through their financial assessment aspect. Prospective borrowers must present their financial landscape to borrow against a specific asset – a vehicle in one case and pension accumulations in another. Both forms necessitate clear communication about loan terms, repayment schedules, and any associated fees or taxes that may apply, highlighting informed borrowing.

The Debt Consolidation Loan Application shares a common goal with the QPP loan application: to alleviate the borrower’s financial burden. Applicants disclose their financial situation to consolidate multiple debts into a single, more manageable loan, analogous to how individuals might use a QPP loan for financial relief. Detailed personal and financial information is crucial in both contexts to assess the applicant's repayment capacity.

Finally, the Medical Loan Application bears resemblance in its provision for individuals to finance health-related expenses, similar to how a QPP loan might cover various personal financial needs. Both types of applications scrutinize the borrower’s financial health and repayment strategy. The critical difference lies in the loans' intended use, yet the underlying principle of lending against one’s financial assets remains constant.

Dos and Don'ts

When filling out the TRS QPP Loan Application form, it’s crucial to follow the guidelines closely to ensure your application is processed smoothly. Here are seven dos and don'ts to keep in mind:

Do:

- Read the QPP Loans brochure before starting your application to understand the terms and conditions.

- Complete the form with all the requested information accurately.

- Initial any changes you make on the form to acknowledge the edits.

- Check if you are eligible for Electronic Fund Transfer (EFT) for quicker loan disbursement.

- Sign and date your application in the presence of a notary public as required.

- Apply online for convenience if you are not applying for a loan in conjunction with retirement.

- Consider how any outstanding loan balances from a City of New York Deferred Compensation Plan (DCP) may affect your QPP loan amount.

Don't:

- Attempt to apply for a loan after your resignation or termination date.

- Leave any section incomplete or fill it out incorrectly, as this will delay your application process.

- Forget to check the loan amount and repayment period options available to you, especially if applying in conjunction with retirement.

- Ignore the necessity to have date-of-birth documentation on file with TRS as your application could be canceled without it.

- Overlook adverse tax consequences that may result from exceeding your available loan amount.

- Submit your application without reviewing it for accuracy and completeness.

- Delay in submitting a “Request for Withdrawal of Form/Application” if you change your mind, as it must be notarized and received no later than the next business day after your loan application is received by TRS.

Misconceptions

Many individuals face uncertainties when filling out the TRS QPP Loan Application form. Here are nine misconceptions clarified to ensure applicants are well-informed:

One widespread misconception is that the application process is overly complicated. While detailed, the instructions provided ensure applicants are well-guided through each step.

Applicants often believe they can apply for a loan after leaving their job. However, one cannot receive a loan on or after their resignation or termination date, as stated in the application instructions.

There's a false assumption that providing all requested information isn't crucial. The form explicitly requires all requested information, and failure to complete it accurately may delay processing.

Many think that if they make a mistake on the form, they can't correct it. In truth, applicants can make changes, but they must initial any changes made on the form to acknowledge them.

Some applicants wrongly assume they must submit a paper application. The instructions offer an alternative to file the application online, except when applying for a loan in conjunction with retirement.

A common misconception is that once the application is submitted, it cannot be canceled. In reality, there's a provision for cancellation if TRS receives a notarized “Request for Withdrawal of Form/Application” by the specified deadline.

There's a belief that TRS loans do not impact the maximum loan amount from other accounts. However, the application instructions specify that a QPP loan may affect how much one can borrow from their TDA account.

Some think that all members can receive their loan via Electronic Fund Transfer (EFT). The truth is, eligibility for EFT depends on certain conditions, such as being paid on the City of New York payroll and receiving paychecks through direct deposit.

Finally, there's an incorrect assumption that outstanding loan balances from other plans do not impact the QPP loan amount. The instructions clarify that any loan balance from a City of New York Deferred Compensation Plan during the previous 12 months may affect the available loan amount from the QPP account.

Understanding these misconceptions can help ensure that applicants have a smooth experience when applying for a QPP loan and avoid unnecessary delays or complications.

Key takeaways

When approaching the TRS QPP Loan Application form, it's crucial to keep several key points in mind to ensure the process goes smoothly and to maximize the benefits of your Qualified Pension Plan (QPP) loan. Below are nine vital takeaways:

Application Purpose: This application is specifically designed for individuals seeking to borrow against their QPP accumulations. It's important to apply only if you're seeking a loan based on your QPP.

Eligibility: You cannot receive a loan on or after your resignation or termination date. Any loan amount issued on or after this date will be considered a distribution and reported to the IRS.

Completeness and Accuracy: Ensure all requested information is provided and that any changes to the application are initialed. Failing to do so, or submitting an application that is incomplete or incorrectly filled out, will delay the processing of your application.

Documentation Requirements: Your loan application may be canceled if the TRS does not have acceptable date-of-birth documentation on file for you.

Alternative Application Methods: You have the option to apply for a QPP loan online, which may offer a more convenient application process, unless you are applying in conjunction with retirement.

Cancellation Process: If you wish to cancel your application, TRS must receive a notarized "Request for Withdrawal of Form/Application" by the next business day after your loan application is received.

Impact on Other Loans: The maximum amount you may borrow from your QPP might be affected by any existing loan balance from a City of New York Deferred Compensation Plan or a Tax-Deferred Annuity Program within the previous 12-month period.

Electronic Fund Transfer (EFT) Eligibility: If you are eligible, you may opt to have your loan disbursed via EFT, speeding up the process of receiving your funds.

Notarization: The application requires notarization. Ensure it is signed and dated in the presence of a notary public, who must then complete the relevant section.

Understanding these key elements before filling out the TRS QPP Loan Application form can help streamline the process, avoid common pitfalls, and ensure you are making the most informed decision regarding your pension plan benefits.

Popular PDF Documents

Irs Form 9423 Where to Mail - Specifies the limited scope of IRS proposed adjustments or changes that can be appealed using this form.

Are Irs Whistleblower Anonymous - The form requests details about the alleged violator, the type of violation, and any known financial information.