Get Texas Sales Tax Exemption Certificate Form

In the state of Texas, organizations and individuals making purchases for specific purposes may be eligible to benefit from a sales tax exemption. The Texas Sales Tax Exemption Certificate, form 01-315, plays a crucial role in this process, allowing qualified purchasers, such as schools or government agencies, to buy goods without paying the state sales tax. This document, to be completed by the purchaser, requires details such as the name and address of the purchasing entity, contact information, and a description of the items being purchased. It also demands a statement of the exemption's basis, affirming the purchaser's understanding of the legal obligations and consequences tied to the certificate's misuse. Specifically, it underscores the purchaser's liability for sales tax should the exemption claim not adhere to relevant laws or if the purchased items are used differently than stated. Importantly, this form clarifies that it is not applicable for motor vehicle transactions and that neither an "Exemption Number" nor a "Tax Exempt" number is needed for its validity. Designed to be presented to the seller rather than sent to the Comptroller of Public Accounts, it underscores the responsibility placed on the purchaser to use the exemption appropriately and warns of the penalties associated with fraudulent claims. This certificate is a testament to Texas's regulatory framework's complexity regarding tax exemptions and the diligence required in claiming such privileges.

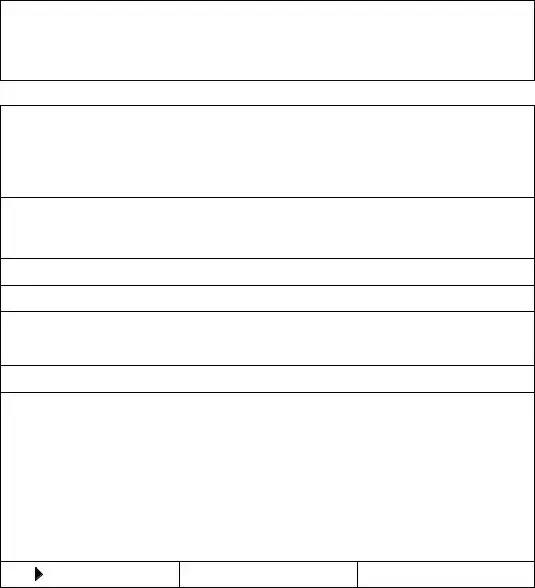

Texas Sales Tax Exemption Certificate Example

TAXES SALES TAX EXEMPTION CERTIFICATE

Name of purchaser, firm or agency

HOUSTON INDEPENDENT SCHOOL DISTRICT

Address (Street & number, P.O. Box or Route number) |

Phone (Area code and number) |

|

4400 W. 18th St. |

|

(713) |

City, State, ZIP code |

|

|

Houston, Texas |

77092 |

|

I, the purchaser named above, claim an exemption from payment of sales taxes for the purchase of taxable items described below or on the attached order or invoice from:

Seller : ____________________________________________________

Street address: ____________________________ City, State, Zip code:_________________________

Description of items to be purchased, or on the attached order or invoice :

Purchaser claims this exemption for the following reasons:

I understand that I will be liable for payment of sales tax which may become due for failure to comply with the provisions of the state, city, metropolitan transit authority, city transit department and/or country sales and use tax laws and Comptroller rules regarding exempt purchases. Liability for the tax will be determined by the price paid for the taxable items purchased or the fair market rental value for the period of time used.

I understand that it is a misdemeanor to give an exemption certificate to the seller for taxable items which I know, at the time of purchase, will be used in a manner other than that expressed in this certificate and that upon conviction may be fined not more than $500 per offense.

sign Purchaser here

Title

Date

NOTE: This certificate cannot be issued for the purchase, lease or rental or a motor vehicle.

THIS CERTIFICATE DOES NOT REQUIRE A NUMBER TO BE VALID

Sales and Use Tax “Exemption Numbers” or “Tax Exempt” Numbers do not exist.

This certificate should be furnished to the supplier. Do not sent the completed Certificate to the Comptroller of Public Accounts.

Document Specifics

| Fact Name | Description |

|---|---|

| Form Number | 01-315 (Rev. 1-88/3) |

| Form Title | SALES TAX EXEMPTION CERTIFICATE |

| Example Purchaser | HOUSTON INDEPENDENT SCHOOL DISTRICT |

| Purchaser Address | 4400 W. 18th St., Houston, Texas 77092 |

| Purchaser Phone Number | (713) 556-6400 |

| Exemption Certificate Use | For claiming exemption from payment of sales taxes on purchases of taxable items. |

| Buyer Responsibility | Purchaser is liable for sales tax due for non-compliant use of the purchased items. |

| Legal Consequence of Misuse | Misuse of the certificate is a misdemeanor, punishable by a fine of not more than $500 per offense. |

| Exemption Certificate Special Note | This certificate cannot be used for the purchase, lease, or rental of a motor vehicle. |

| Handling of Certificate | The certificate should be furnished to the supplier, not sent to the Comptroller of Public Accounts. |

Guide to Writing Texas Sales Tax Exemption Certificate

Filling out the Texas Sales Tax Exemption Certificate form is a straightforward process that grants organizations the ability to make tax-exempt purchases for qualifying items. Whether it's for a school, non-profit, or government agency, understanding how to properly complete this document is crucial to ensure compliance with Texas tax laws. It's not just about filling out a form; it's about affirming your organization's rights and responsibilities under the law.

Here are the steps needed to properly fill out the form:

- Name of purchaser, firm or agency: Enter the official name of the entity that is claiming the exemption. Example: HOUSTON INDEPENDENT SCHOOL DISTRICT.

- Address (Street & number, P.O. Box or Route number): Provide the complete mailing address of the purchaser. Example: 4400 W. 18th St.

- Phone (Area code and number): Include the telephone number, with area code, of the purchaser. Example: (713) 556-6400.

- City, State, ZIP code: Fill in the city, state, and ZIP code. Example: Houston, Texas 77092.

- Under the section that states "I, the purchaser named above, claim an exemption from payment of sales taxes for the purchase of taxable items described below or on the attached order or invoice from:", you will:

- Write the name of the seller.

- Provide the seller's street address.

- Fill in the seller's city, state, and ZIP code.

- Description of items to be purchased, or on the attached order or invoice: Clearly describe the items you are intending to purchase tax-free. Be as specific as possible to avoid any confusion.

- Under "Purchaser claims this exemption for the following reasons:" indicate the basis of your claim for tax exemption. This reason must align with Texas tax exemption laws and eligibility criteria.

- Read the statement following the claim reason carefully. This is your acknowledgment of the rules governing tax-exempt purchases and the penalties for misuse.

- Signature of Purchaser: The authorized representative of the purchasing entity must sign the form.

- Title: Provide the title of the individual signing the form, indicating their position in the organization.

- Date: Indicate the date the certificate is being signed.

After completing the form, ensure it's handed over to the supplier and not sent to the Comptroller of Public Accounts. Remember, this certificate empowers your organization to make essential purchases without the added burden of sales tax, provided those purchases comply with Texas law. It's not just a piece of paper; it's a testament to your organization's commitment to following the state's legal framework for tax exemptions.

Understanding Texas Sales Tax Exemption Certificate

What is the Texas Sales Tax Exemption Certificate?

A Texas Sales Tax Exemption Certificate allows purchasers, such as the Houston Independent School District listed on the form, to buy or lease items without paying sales tax on them. This applies to specific purchases as detailed in the form or attached orders or invoices. The certificate is a declaration by the purchaser that the items will be used in a manner that qualifies for tax exemption, per certain conditions laid out by Texas law and the Comptroller's rules.

Who can use this exemption certificate?

This certificate is designed for use by organizations or entities, like school districts, that are exempt from paying sales taxes in Texas. These entities claim exemption for purchases related to their exempt operations. Use of this certificate is not restricted to educational institutions; it can also be utilized by other eligible organizations provided their purchases meet the criteria for tax exemption under Texas tax laws.

What responsibilities does the purchaser have when using this certificate?

By signing the exemption certificate, the purchaser is acknowledging their understanding of the laws and obligations related to exempt purchases. This includes the responsibility to ensure that the purchased items are used in ways that comply with the tax-exempt purposes stated. Misuse of the certificate, where taxable items are purchased under the guise of exemption but used for non-exempt purposes, can result in a misdemeanor charge with fines up to $500 per offense. Additionally, the purchaser accepts liability for any sales tax, penalties, and interest that may become due if the terms of the exemption are violated.

Is a number required for this certificate to be valid?

No, a specific exemption number or “tax exempt” number is not needed for the certificate to be considered valid. The misconception that such a number is required persists, but the form itself clarifies that validity comes from accurately filling out and furnishing the certificate to the seller for tax-exempt purchases. Therefore, ensuring the form is completed correctly and in full is crucial for its acceptance and validity.

Should this certificate be submitted to the Texas Comptroller?

No, the completed Texas Sales Tax Exemption Certificate should not be sent to the Comptroller of Public Accounts. The correct procedure is for the purchaser to furnish the certificate to the supplier or seller of the goods. It serves as proof that the purchase is made by an entity eligible for tax exemption. The seller keeps the certificate on file as evidence of the exempt sale, in case of an audit by the Texas Comptroller.

Common mistakes

When completing the Texas Sales Tax Exemption Certificate, attention to detail is crucial. Even minor mistakes can lead to unexpected tax liabilities or penalties. Below are seven common pitfalls to avoid:

- Incorrect or Incomplete Purchaser Information: Often, individuals mistakenly provide incomplete or incorrect information regarding the name, address, and phone number of the purchaser, firm, or agency. This foundational information should be double-checked for accuracy to ensure it corresponds exactly with official records.

- Failure to Specify the Seller's Information Fully: Leaving blanks or providing partial information in the seller's details section can invalidate the certificate. Every field, including the seller's name, street address, city, state, and zip code, must be thoroughly completed to meet the form's requirements.

- Inaccurate Description of Items: At times, the description of items to be purchased, or the information provided on the attached order or invoice, lacks specificity or clarity. It's critical to detail precisely what items are being purchased tax-free, as vague or unclear descriptions could lead to the exemption being questioned.

- Not Clearly Stating the Exemption Reason: The form requires that purchasers specify why they claim tax exemption. A common error is providing a vague or incorrect justification for the exemption, which can result in the rejection of the certificate.

- Omitting Signature, Title, or Date: Neglecting to sign the certificate, specify the purchaser's title, or include the date effectively renders the document invalid. These elements are essential for confirming the exemption's authenticity and timeframe.

- Assuming Exemption Applies to Non-Qualified Purchases: A significant misstep is assuming that the exemption automatically applies to all purchases, including those explicitly excluded by law, such as motor vehicles. Always verify that the items purchased fall within the permissible categories for tax exemption.

- Using an "Exemption Number" or "Tax Exempt" Number: Despite common belief, Texas Sales and Use Tax Exemption Certificates do not require a number to be valid. Providing such a number, or believing one is necessary, can cause confusion and potentially delay processing.

In summary, meticulously filling out the Texas Sales Tax Exemption Certificate with accurate and complete information is paramount. By sidestepping these common errors, purchasers can ensure their transactions are smoothly processed without the hassle of audits or penalties. Remembering details such as clearly stating the purpose of exemptions, providing comprehensive descriptions of items, and including all necessary signatures, will facilitate a straightforward and compliant tax exemption process.

Documents used along the form

When navigating the requirements for tax exemptions in Texas, particularly for organizations such as schools, non-profits, or government bodies, a comprehensive understanding of the necessary documentation is essential. The Texas Sales Tax Exemption Certificate form is a crucial document for these entities to purchase goods without paying state sales tax. However, to fully leverage tax exemptions and ensure compliance, several other forms and documents often accompany this certificate during various transactions. Here's a closer look at some of these key documents.

- Application for Texas Identification Number Form (AP-152): This form is used to apply for a Texas Taxpayer Identification Number that is required for tax reporting purposes.

- Annual Resale Certificate for Sales Tax (01-339): Businesses can use this certificate to purchase items for resale without paying sales tax.

- Request for Tax Clearance Letter (Form 05-359): A necessary document for businesses winding up operations. It confirms all state taxes have been paid.

- Sales and Use Tax Return (Form 01-114): Filed by vendors to report taxable sales and remit the collected tax to the state.

- Exemption Certification for Agriculture and Timber Operations (Form 01-924): Allows individuals involved in agriculture and timber to make tax-exempt purchases related to their operations.

- Motor Vehicle Tax Exemption Certificate (Form 14-312): Specifically for the purchase, lease, or rental of motor vehicles by qualifying entities like governmental bodies without paying the motor vehicle sales tax.

- Hotel Occupancy Tax Exemption Certificate (Form 12-302): For qualifying organizations and employees of exempt organizations to claim exemption from the state hotel occupancy tax.

- Purchase Exemption Certification (Form 01-931): Utilized by nonprofit and tax-exempt organizations for purchasing goods without sales tax.

- Direct Pay Permit Application (Form 01-777): Allows businesses to directly pay sales and use taxes on taxable purchases instead of through their vendors.

- Customs Broker’s Power of Attorney (Form 01-339): Granted by importers to customs brokers, authorizing them to act on their behalf in customs matters, including claiming tax exemptions on imported goods.

Understanding and properly utilizing these documents can considerably streamline the process of claiming exemptions and ensuring tax compliance. These forms each serve distinct roles—from establishing an entity’s eligibility for tax exemptions, to reporting and directly paying taxes, to specific use cases such as for agricultural operations or in international trade. For businesses and organizations eligible for Texas sales tax exemptions, maintaining up-to-date knowledge and careful record-keeping of these forms is crucial for financial efficiency and legal compliance.

Similar forms

The Resale Certificate, similar to the Texas Sales Tax Exemption Certificate, serves a pivotal role in the transaction process between vendors and resellers. Where the Texas Sales Tax Exemption Certificate allows organizations to avoid paying sales tax on purchases that are deemed exempt, the Resale Certificate enables businesses to purchase goods without paying sales tax, on the condition that the items bought are to be resold in the course of business. Both forms operate under the principle of tax exemption, albeit for different reasons, but they share the common thread of requiring the purchaser's acknowledgment that the items will be used in a manner consistent with the claimed exemption. Noncompliance or misuse of either certificate can lead to tax liabilities, penalties, or fines.

The Use Tax Certificate is a document that bears resemblance to the Texas Sales Tax Exemption Certificate, though it serves a distinct function regarding tax liabilities for purchases made outside one's tax jurisdiction. Use tax is a complementary tax to sales tax, incurred when goods are purchased tax-free from out-of-state sellers for use, storage, or consumption within the purchaser's state. The Texas Sales Tax Exemption Certificate prevents sales tax at the point of sale on eligible transactions, whereas the Use Tax Certificate is more about self-assessing tax obligations on items that were not taxed at the time of purchase. Both documents underscore the importance of understanding and adhering to tax obligations for exempt transactions.

Non-Profit Exemption Certificates provide tax-exempt status for eligible non-profit organizations, such as charities and educational institutions, much like how the Texas Sales Tax Exemption Certificate does for specific purchases by qualifying entities. The Non-Profit Exemption Certificate specifically applies to organizations that meet certain criteria and can exempt them from a range of taxes, including sales and use taxes on purchases relevant to their non-profit mission. The parallel with the Texas Sales Tax Exemption Certificate lies in the provision that purchases must be related to the organization's exempt purpose, underlining the necessity of compliance with tax laws to maintain exemption benefits.

The Direct Pay Permit operates in a similar realm as the Texas Sales Tax Exemption Certificate, providing a special permit to certain taxpayers, allowing them to directly remit tax to the state rather than to the vendor at the point of sale. Like the Texas Sales Tax Exemption Certificate, the Direct Pay Permit system is used to streamline tax exemption claims on qualifying purchases. However, it shifts the payment and reporting of taxes from the vendor to the purchaser. Both arrangements demand meticulous record-keeping and an understanding of what purchases qualify for exemptions, with the goal of ensuring accurate tax reporting and compliance.

Finally, the Agricultural Exemption Certificate parallels the Texas Sales Tax Exemption Certificate, offering tax exemptions for purchases related to agricultural production. This certificate allows farmers and ranchers to avoid paying sales tax on items such as feed, seed, and farm equipment, assuming these purchases are used directly in agricultural production. Similar to the Texas Sales Tax Exemption Certificate, the Agricultural Exemption Certificate necessitates that buyers certify their intent to use the purchased goods in a manner consistent with their qualification for exemption. Misrepresentation or misuse of the certificate exposes the purchaser to potential tax liabilities and penalties, emphasizing the importance of honesty in claiming tax-exempt purchases.

Dos and Don'ts

When filling out the Texas Sales Tax Exemption Certificate form, there are several dos and don'ts to keep in mind to ensure the process is completed correctly and efficiently. Below is a guide to help you navigate this process:

Dos:

- Provide accurate information: Ensure that all details about the purchaser, firm, or agency, including the name, address, and phone number, are correct and current.

- Clearly describe the items: Give a detailed description of the items to be purchased tax-exempt. If the space isn't sufficient, attach an order or invoice with the detailed list.

- State the exemption reason clearly: Specify the reason for claiming the tax exemption. Make sure it is one of the valid reasons recognized by the law.

- Sign and date the certificate: Do not forget to sign the certificate and add the date. An unsigned certificate might not be considered valid.

- Ensure the seller's information is complete: Fill in the seller's name, street address, city, state, and zip code to prevent any processing delays.

- Keep a copy for your records: After providing the completed certificate to the seller, keep a copy for future reference or in case of an audit.

- Understand the limitations: Acknowledge that this exemption certificate cannot be used for the purchase, lease, or rental of a motor vehicle.

Don'ts:

- Do not guess details: Avoid filling in any part of the form with uncertain information. Verify all details before entering them.

- Do not leave sections blank: Ensure no sections of the form are left incomplete. Each part of the form collects critical information.

- Do not misuse the certificate: It is unlawful to use this certificate for items that will not be used as stated. Misuse could lead to penalties.

- Do not send the certificate to the wrong place: The completed certificate should be furnished to the supplier, not sent to the Comptroller of Public Accounts.

- Do not forget the document is legally binding: Remember, providing false information can result in fines. Treat the document with the seriousness it requires.

- Do not use the certificate for personal items: The certificate is intended for specific tax-exempt purchases. It should not be used for personal shopping.

- Do not overlook the detail about motor vehicles: Be aware that this certificate explicitly excludes motor vehicles from tax exemptions.

Misconceptions

When it comes to navigating the complexities of sales tax exemptions in Texas, certain misunderstandings frequently arise, particularly regarding the Texas Sales Tax Exemption Certificate form. Addressing these misconceptions is crucial for both purchasers and sellers to ensure compliance and avoid unnecessary penalties.

Misconception 1: A special number is needed to validate the exemption certificate. Unlike what many believe, the Texas Sales Tax Exemption Certificate does not require a unique number for it to be considered valid. The clarification that "Sales and Use Tax 'Exemption Numbers' or 'Tax Exempt' Numbers do not exist" directly combats this common misunderstanding.

Misconception 2: The certificate must be sent to the Comptroller. Another frequent error is the belief that the completed exemption certificate must be submitted to the Comptroller of Public Accounts. In reality, the certificate should be furnished to the supplier, and there is no requirement to send it to the Comptroller’s office.

Misconception 3: The exemption certificate covers motor vehicle purchases, leases, or rentals. It's important to note that this certificate specifically excludes the purchase, lease, or rental of a motor vehicle. This limitation is clearly stated, yet it often catches purchasers by surprise.

Misconception 4: Any purchase made with the certificate is exempt from sales tax. Just because an exemption certificate has been issued does not mean all purchases made with it are automatically exempt from sales tax. The items to be purchased must match the description on the certificate or accompanying order or invoice, and they must be used in a manner consistent with the stated exemption reason.

Misconception 5: Misuse of the certificate carries no penalties. There's a serious consequence for knowingly using an exemption certificate for taxable items intended to be used in a manner different from that expressed in the certificate. The document clearly warns that misuse is a misdemeanor that may result in a fine of not more than $500 per offense, dispelling any notion that there’s no accountability for improper use.

Understanding these facets of the Texas Sales Tax Exemption Certificate form ensures that businesses and organizations can navigate tax exemptions confidently, thereby avoiding common pitfalls and ensuring compliance with state sales and use tax laws.

Key takeaways

When it comes to navigating tax exemptions in Texas, understanding the nuances of the Sales Tax Exemption Certificate is critical. Below are nine key takeaways that should guide purchasers and businesses in filling out and using this form properly:

- Who Uses the Certificate: The Texas Sales Tax Exemption Certificate is designed for use by individuals or entities such as the Houston Independent School District that are eligible to claim exemption from sales taxes.

- Required Information: Essential details that must be provided include the name of the purchaser, firm, or agency, their address, phone number, and a description of the items being purchased.

- Exemption Justification: Purchasers must specify the reasons they're claiming an exemption for the items described in the certificate or attached documents.

- Purchaser Liability: It's understood by the purchaser that they will be liable for sales tax payment if it's determined that the purchase does not comply with the applicable state and local tax laws and regulations.

- Legal Consequences: Misuse of the exemption certificate, such as claiming exemption for taxable items that will be used in a way other than what's stated, can result in misdemeanor charges. Convictions may carry fines of up to $500 per offense.

- Uses of the Certificate: This form is applicable for most tangible personal property and services. However, it cannot be used for the purchase, lease, or rental of motor vehicles.

- Certificate Number Not Required: A notable aspect of the Texas Sales Tax Exemption Certificate is that it does not require a certificate number to be valid. Unlike in some states, “Exemption Numbers” or “Tax Exempt” numbers are not used or issued.

- Proper Submission of the Certificate: The completed certificate should be furnished directly to the supplier of the goods or services being purchased. It should not be sent to the Comptroller of Public Accounts.

- Keeping Records: Both the purchaser and the seller need to keep a copy of the certificate on file. This is essential for documentation and verification purposes should questions about the tax-exempt purchase arise in the future.

Handling the Texas Sales Tax Exemption Certificate with care ensures compliance with tax laws and avoids potential legal and financial repercussions. Whether you're an educational institution, nonprofit, or eligible business, understanding these takeaways is crucial to leveraging tax exemptions effectively.

Popular PDF Documents

Irs Form 3911 Instructions - Facilitates the resolution of discrepancies or delays in the receipt of IRS-issued payments, including refunds and stimulus funds.

Schedule B 941 Form 2023 - Allows for a thorough review and correction of payroll records, ensuring accuracy in tax filings.