Get Tax St 100 Form

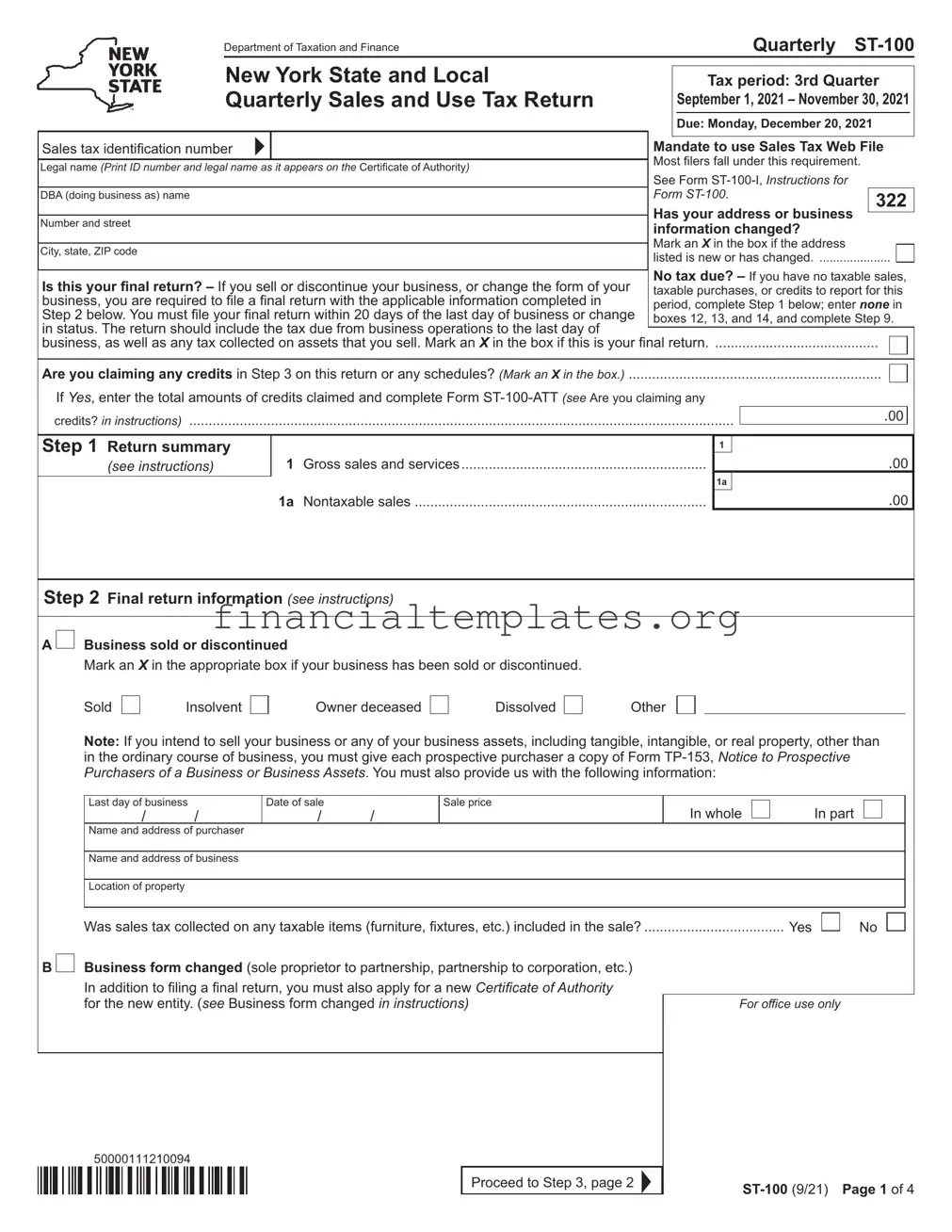

Facing the complex landscape of sales tax in New York State, the Quarterly ST-100 form emerges as a crucial document for businesses navigating through their tax obligations. Issued by the Department of Taxation and Finance for the third quarter covering September 1, 2021, through November 30, 2021, with a due date of December 20, 2021, this form encapsulates the need for meticulous record-keeping and precise reporting. It mandates businesses to disclose their gross sales and services, including both taxable and nontaxable sales, and to calculate sales and use taxes across various taxing jurisdictions with different rates. Significantly, the ST-100 form is designed to be filed using the Sales Tax Web File system, reflecting the state's push towards digital tax administration. This requirement captures most filers, streamlining the process and enhancing compliance. Additionally, the form accommodates situations such as business sales, discontinuations, or changes in business structure, requiring specific final return information and potentially new applications for a Certificate of Authority. Further complexity is introduced through the calculation of special taxes on services and products like passenger car rentals and vapor products, alongside provisions for claiming tax credits and advance payments. For vendors, the ST-100 outlines the conditions under which they may be eligible for vendor collection credit, emphasizing the importance of timely filing and full tax payment. Ultimately, the ST-100 form serves as a comprehensive tool for businesses to fulfill their sales tax duties while navigating through the intricacies of state and local tax regulations.

Tax St 100 Example

Department of Taxation and Finance |

Quarterly |

|

New York State and Local |

Tax period: 3rd Quarter |

|

Quarterly Sales and Use Tax Return |

September 1, 2021 – November 30, 2021 |

|

|

Due: Monday, December 20, 2021 |

|

Sales tax identification number |

Mandate to use Sales Tax Web File |

|

|

Most filers fall under this requirement. |

|

Legal name (Print ID number and legal name as it appears on the Certificate of Authority) |

|

|

|

See Form |

|

DBA (doing business as) name |

Form |

|

|

|

322 |

|

Has your address or business |

|

Number and street |

information changed? |

|

|

Mark an X in the box if the address |

|

City, state, ZIP code |

|

|

|

listed is new or has changed |

|

|

No tax due? – If you have no taxable sales, |

|

Is this your final return? – If you sell or discontinue your business, or change the form of your |

taxable purchases, or credits to report for this |

|

business, you are required to file a final return with the applicable information completed in |

period, complete Step 1 below; enter none in |

|

Step 2 below. You must file your final return within 20 days of the last day of business or change |

boxes 12, 13, and 14, and complete Step 9. |

|

in status. The return should include the tax due from business operations to the last day of |

|

|

business, as well as any tax collected on assets that you sell. Mark an X in the box if this is your final return |

||

Are you claiming any credits in Step 3 on this return or any schedules? (Mark an X in the box.) |

|

|

If Yes, enter the total amounts of credits claimed and complete Form |

|

|

credits? in instructions) |

.00 |

|

Step 1 Return summary

(see instructions)

1 Gross sales and services................................................................

1a Nontaxable sales ...........................................................................

1

1a

.00

.00

Step 2 Final return information (see instructions)

A

Business sold or discontinued

Business sold or discontinued

Mark an X in the appropriate box if your business has been sold or discontinued.

Sold

Insolvent

Owner deceased

Dissolved

Other

Note: If you intend to sell your business or any of your business assets, including tangible, intangible, or real property, other than in the ordinary course of business, you must give each prospective purchaser a copy of Form

Last day of business |

|

Date of sale |

|

Sale price |

In whole |

|

In part |

|

|

|

|

|

|

|

|||||

/ |

/ |

/ |

/ |

|

|

|

|

||

|

|

|

|||||||

Name and address of purchaser |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name and address of business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location of property |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Was sales tax collected on any taxable items (furniture, fixtures, etc.) included in the sale? |

Yes |

No

B  Business form changed (sole proprietor to partnership, partnership to corporation, etc.)

Business form changed (sole proprietor to partnership, partnership to corporation, etc.)

In addition to filing a final return, you must also apply for a new Certificate of Authority for the new entity. (see Business form changed in instructions)

For office use only

50000111210094

Proceed to Step 3, page 2

Page 2 of 4

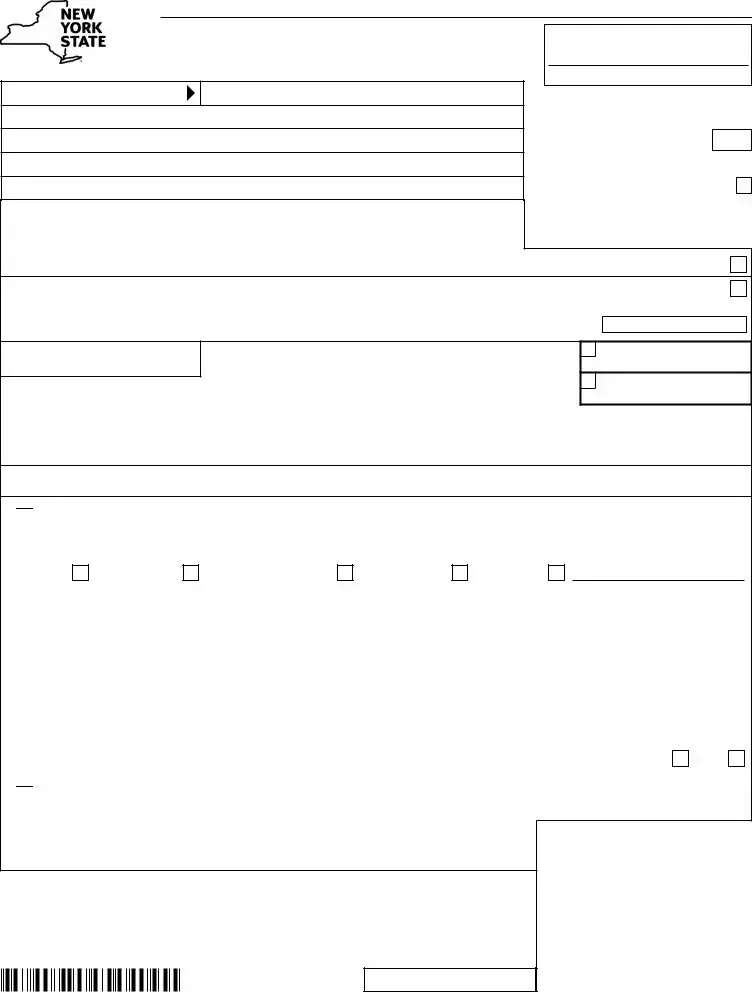

Sales tax identification number

322

Quarterly

Step 3 Calculate sales and use taxes |

|

|

|

Column C |

|

|

|

Column D |

|

Column E |

|

|

Column F |

||

|

|

|

Taxable sales |

+ |

|

Purchases subject |

× Tax rate |

= |

Sales and |

||||||

|

(see instructions) |

|

|

|

and services |

|

|

|

to tax |

|

|

|

|

use tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(C + D) × E |

|

Enter the total from Schedule FR, page 4, step 6, box 18 (if |

|

|

|

|

|

|

|

|

|

2 |

|

|

|||

any) in box 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|||

Enter the total paper bag fee from Schedule E, box 1 (if any) in box 2a. |

|

|

|

|

|

|

|

|

|

2a |

|

|

|||

Enter the sum of any totals from Schedules A, B, H, N, T and W (if any).... |

3 |

|

.00 |

|

4 |

|

.00 |

|

|

5 |

|

|

|||

|

Column A |

Column B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxing jurisdiction |

Jurisdiction code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

.00 |

4% |

|

|

|

|

|

New York State only |

NE |

0021 |

|

|

|

|

|

|

|

|

|

||||

Albany County |

AL |

0181 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Allegany County |

AL |

0221 |

|

|

.00 |

|

|

|

.00 |

8½% |

|

|

|

|

|

Broome County |

BR |

0321 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Cattaraugus County (outside the following) |

CA |

0481 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Olean (city) |

OL |

0441 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Salamanca (city) |

SA |

0431 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Cayuga County (outside the following) |

CA |

0511 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Auburn (city) |

AU |

0561 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Chautauqua County |

CH |

0651 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Chemung County |

CH |

0711 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Chenango County (outside the following) |

CH |

0861 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Norwich (city) |

NO |

0831 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Clinton County |

CL |

0921 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Columbia County |

CO |

1021 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Cortland County |

CO |

1131 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Delaware County |

DE |

1221 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Dutchess County |

DU |

1311 |

|

|

.00 |

|

|

|

.00 |

8⅛%* |

|

|

|

|

|

Erie County |

ER |

1451 |

|

|

.00 |

|

|

|

.00 |

8¾% |

|

|

|

|

|

Essex County |

ES |

1521 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Franklin County |

FR |

1621 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Fulton County (outside the following) |

FU |

1791 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Gloversville (city) |

GL |

1741 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Johnstown (city) |

JO |

1751 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Genesee County |

GE |

1811 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Greene County |

GR |

1911 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Hamilton County |

HA |

2011 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Herkimer County |

HE |

2121 |

|

|

.00 |

|

|

|

.00 |

8¼% |

|

|

|

|

|

Jefferson County |

JE |

2221 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Lewis County |

LE |

2321 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Livingston County |

LI |

2411 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Madison County (outside the following) |

MA |

2511 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Oneida (city) |

ON |

2541 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Monroe County |

MO |

2611 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Montgomery County |

MO |

2781 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Nassau County |

NA 2811 |

|

|

.00 |

|

|

|

.00 |

8⅝%* |

|

|

|

|

||

Niagara County |

NI |

2911 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Oneida County (outside the following) |

ON |

3010 |

|

|

.00 |

|

|

|

.00 |

8¾% |

|

|

|

|

|

|

Rome (city) |

RO |

3015 |

|

|

.00 |

|

|

|

.00 |

8¾% |

|

|

|

|

Utica (city) |

UT |

3018 |

|

|

.00 |

|

|

|

.00 |

8¾% |

|

|

|

|

|

Onondaga County |

ON |

3121 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Ontario County |

ON |

3211 |

|

|

.00 |

|

|

|

.00 |

7½% |

|

|

|

|

|

Orange County |

OR |

3321 |

|

|

.00 |

|

|

|

.00 |

8⅛%* |

|

|

|

|

|

Orleans County |

OR |

3481 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Oswego County (outside the following) |

OS |

3501 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

Oswego (city) |

OS |

3561 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

Otsego County |

OT |

3621 |

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

|

|

|

|

6 |

|

|

|

7 |

|

|

|

|

8 |

|

|

Column subtotals; also enter on page 3, boxes 9, 10, and 11: |

|

|

.00 |

|

|

|

.00 |

|

|

|

|

|

|||

50000211210094

Quarterly

322

Sales tax identification number

Step 3 Calculate sales and use taxes (continued)

|

Column A |

|

Column B |

|

Column C |

|

|

Column D |

|

Column E |

|

|

Column F |

||||

|

Taxing jurisdiction |

|

Jurisdiction |

|

Taxable sales |

+ |

Purchases subject |

× Tax rate |

= |

Sales and use tax |

|||||||

|

|

|

code |

|

and services |

|

|

to tax |

|

|

|

|

|

(C + D) × E |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|

|

|

|

Putnam County |

|

PU 3731 |

|

|

|

.00 |

|

|

|

.00 |

8⅜% |

|

|

|

|

||

Rensselaer County |

|

RE 3881 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|

|

|

|

Rockland County |

|

RO 3921 |

|

|

|

.00 |

|

|

|

.00 |

8⅜% |

|

|

|

|

||

St. Lawrence County |

|

ST 4091 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Saratoga County (outside the following) |

|

SA 4111 |

|

|

|

.00 |

|

|

|

.00 |

7% |

|

|

|

|

||

|

Saratoga Springs (city) |

|

SA 4131 |

|

|

|

.00 |

|

|

|

.00 |

7% |

|

|

|

|

|

Schenectady County |

|

SC 4241 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Schoharie County |

|

SC 4321 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Schuyler County |

|

SC 4411 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Seneca County |

|

SE 4511 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Steuben County |

|

ST 4691 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|

|

|

|

Suffolk County |

|

SU 4711 |

|

|

|

.00 |

|

|

|

.00 |

8⅝% |

|

|

|

|

||

Sullivan County |

|

SU 4821 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Tioga County |

|

TI 4921 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Tompkins County (outside the following) |

|

TO 5081 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

|

Ithaca (city) |

|

IT 5021 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

|

Ulster County |

|

UL 5111 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Warren County (outside the following) |

|

WA 5281 |

|

|

|

.00 |

|

|

|

.00 |

7% |

|

|

|

|

||

|

Glens Falls (city) |

|

GL 5211 |

|

|

|

.00 |

|

|

|

.00 |

7% |

|

|

|

|

|

Washington County |

|

WA 5311 |

|

|

|

.00 |

|

|

|

.00 |

7% |

|

|

|

|

||

Wayne County |

|

WA 5421 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|

|

|

|

Westchester County (outside the following) |

|

WE 5581 |

|

|

|

.00 |

|

|

|

.00 |

8⅜% |

|

|

|

|

||

|

Mount Vernon (city) |

|

MO 5521 |

|

|

|

.00 |

|

|

|

.00 |

8⅜%* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

|

|

|

|

|

New Rochelle (city) |

|

NE 6861 |

|

|

|

.00 |

|

|

|

.00 |

8⅜% |

|

|

|

|

||

|

White Plains (city) |

|

WH 6513 |

|

|

|

.00 |

|

|

|

.00 |

8⅜%* |

|

|

|

|

|

|

Yonkers (city) |

|

YO 6511 |

|

|

|

.00 |

|

|

|

.00 |

8⅞%* |

|

|

|

|

|

Wyoming County |

|

WY 5621 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

Yates County |

|

YA 5721 |

|

|

|

.00 |

|

|

|

.00 |

8% |

|

|

|

|

||

New York City/State combined tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[New York City includes counties of Bronx, Kings (Brooklyn), |

NE 8081 |

|

|

|

.00 |

|

|

|

.00 |

8⅞%* |

|

|

|

|

|||

New York (Manhattan), Queens, and Richmond (Staten Island)] |

|

|

|

|

|

|

|

|

|

|

|||||||

New York State/MCTD |

|

NE 8061 |

|

|

|

.00 |

|

|

|

.00 |

4⅜%* |

|

|

|

|

||

New York City - local tax only |

|

NE 8091 |

|

|

|

.00 |

|

|

|

.00 |

4½% |

|

|

|

|

||

|

|

|

|

|

|

|

.00 |

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

.00 |

|

|

|

|

|

|

|

Column subtotals from page 2, boxes 6, |

7, and 8: |

9 |

|

|

.00 |

10 |

|

|

.00 |

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If the total of box 12 + box 13 = $300,000 or more, |

12 |

|

|

|

13 |

|

|

|

|

|

|

14 |

|

|

||

|

see page 1 of instructions. |

Column totals: |

|

|

|

.00 |

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

Internal code |

|

|

Column G |

|

Column H |

|

|

Column J |

|

|||

Step 4 Calculate special taxes (see instructions) |

|

|

|

|

= |

||||||||||||

|

|

|

|

|

Taxable receipts |

× Tax rate |

Special taxes due |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(G × H) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Passenger car rentals (outside the MCTD) |

|

|

|

PA |

0012 |

|

|

|

|

.00 |

12% |

|

|

|

|

||

Passenger car rentals (within the MCTD) |

|

|

|

PA |

0030 |

|

|

|

|

.00 |

12% |

|

|

|

|

||

Information & entertainment services furnished via telephony and telegraphy |

|

IN |

7009 |

|

|

|

|

.00 |

5% |

|

|

|

|

||||

Vapor products |

|

|

|

VA |

7060 |

|

|

|

|

.00 |

20% |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Total special taxes: |

15 |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 5 Other tax credits and advance payments (see instructions) |

|

|

|

|

Internal code |

|

|

Column K |

|||||||||

|

|

|

|

|

|

|

|

|

Credit amount |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Credit for prepaid sales tax on cigarettes |

|

|

|

|

|

|

|

|

|

CR C8888 |

|

|

|

|

|||

Overpayment being carried forward from a prior period |

|

|

|

|

|

|

|

|

C |

|

|

|

|

||||

Advance payments (made with Form |

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

||

|

|

|

Total tax credits, advance payments, and overpayments: |

16 |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*4⅜% = 0.04375; |

8⅜% = 0.08375; |

7⅜% = 0.07375; |

8⅝% = 0.08625; |

8⅛% = 0.08125; |

8⅞% = 0.08875 |

Proceed to Step 6,

page 4

50000311210094

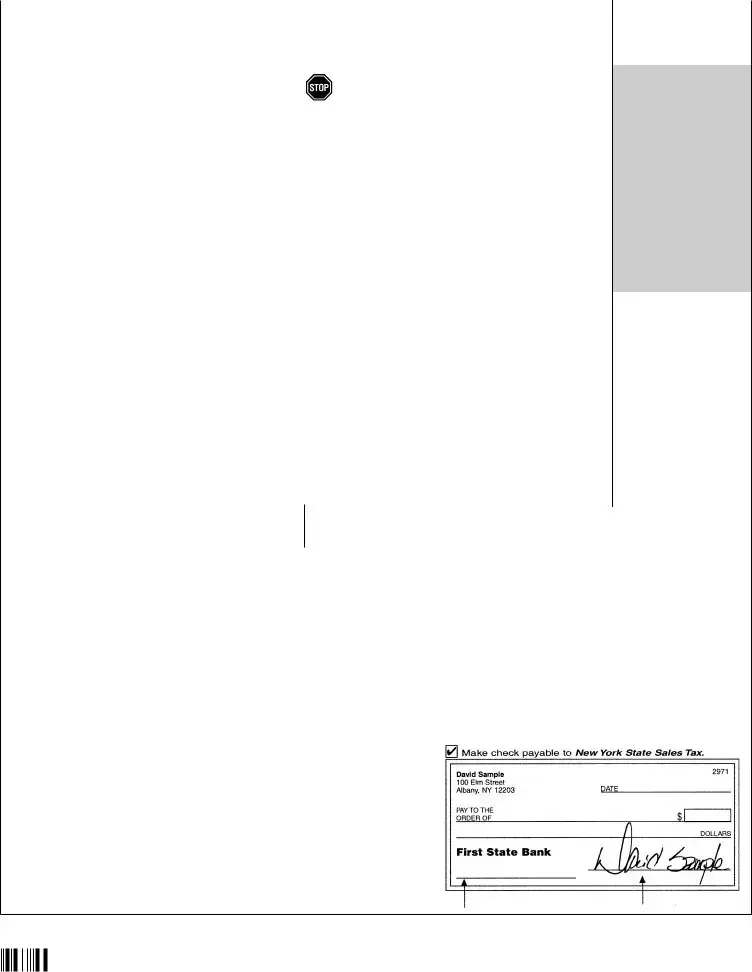

Page 4 of 4 |

|

Sales tax identification number |

|

|

|

|

|

|

322 |

Quarterly |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 6 Calculate taxes due |

|

|

Add Sales and use tax column total (box 14) to Total special |

|

|

|

|

|

Taxes due |

|||||||||||||||||

|

|

taxes (box 15) and subtract Total tax credits, advance |

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

payments, and overpayments (box 16). Enter result in box 17. |

|

|

|

|

|

|||||||||||

|

Box 14 |

|

|

+ |

Box 15 |

|

|

|

|

Box 16 |

= |

|

17 |

|

|

|

|

|||||||||

|

amount |

$ |

|

amount $ |

|

|

|

|

amount $ |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 7 Calculate vendor collection credit |

|

If you are filing this return after the due date and/or not paying the |

|

|

|

|

|

|

|

|

||||||||||||||||

|

full amount of tax due, STOP! You are not eligible for the vendor |

|

|

|

|

|

|

|

|

|||||||||||||||||

or pay penalty and interest (see instructions) |

|

collection credit. If you are not eligible, enter 0 in box 18 and go to 7B. |

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

7A |

Vendor collection credit worksheet |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

1 |

Enter the box 14 amount |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

2 |

Enter the amount from Schedule E, box 1 |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

3 |

Subtract line 2 from line 1 |

|

$ |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

4 |

Enter the box 15 amount |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

5 |

Add lines 3 and 4 |

|

$ |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

6Enter the amount from Schedule FR as instructed on the schedule (if any).

|

|

|

Enter this amount as a positive number |

$ |

|

|

|

|

|

|

|

|

7 |

Add lines 5 and 6 |

|

$ |

|

|

|

|

|

||||

............................................................................................. |

Vendor collection credit |

|||||||||||

|

|

8 Credit amount (multiply line 7 by 5% (.05)) |

$ |

|

|

|

VE 7706 |

|||||

|

|

|

Enter the line 8 amount or $200, whichever is less, in box 18. |

18 |

|

|

||||||

|

|

|

|

|

|

|||||||

|

OR Pay penalty and interest if you are filing late |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

Penalty and interest |

|||||

|

|

|

|

|

|

|

|

|

|

19 |

|

|

|

7B |

Penalty and interest are calculated on the amount in box 17, Taxes due. |

|

|||||||||

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 8 Calculate total amount due |

Make check or money order payable to New York State Sales |

|

Total amount due |

|||||||||

Tax. Write on your check your sales tax identification number, |

|

|||||||||||

|

|

|

(see instructions) |

|

|

|

|

|||||

|

|

|

|

Taking vendor collection credit? Subtract box 18 from box 17. |

20 |

|

|

|||||

|

8A |

|

Amount due: |

|

||||||||

|

|

Paying penalty and interest? Add box 19 to box 17. |

|

|

|

|||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

Enter your payment amount. This amount should match your |

21 |

|

|

|||||

|

8B |

|

Amount paid: |

|

||||||||

|

|

amount due in box 20. |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 9 Sign and mail this return (see instr.)

Please be sure to keep a completed copy for your records.

Must be postmarked by Monday, December 20, 2021, to be considered filed on time. See below for complete mailing information.

Third – |

|

Do you want to allow another person to discuss this return with the Tax Dept? (see instructions) |

Yes |

|

|

|

(complete the following) No |

|

|

||||||||||||

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Designee’s name |

|

Designee’s phone number |

|

Personal identification |

|

|

|

|

||||||||||||

|

|

|

|

|

|||||||||||||||||

party |

|

|

|

( |

) |

|

|

|

|

|

number (PIN) |

|

|

|

|

||||||

designee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Designee’s email address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Authorized |

Signature of authorized person |

|

|

|

Official title |

|

|

|

|

|

|

|

|

|

|

||||||

person |

|

Email address of authorized person |

|

|

|

|

|

|

Telephone number |

|

|

|

|

Date |

|||||||

|

|

|

|

|

|

|

|

|

|

( |

|

) |

|

|

|

|

|

|

|

|

|

Paid |

|

Firm’s name (or yours if |

|

|

|

|

|

Firm’s |

EIN |

|

|

|

|

|

Preparer’s |

PTIN or SSN |

|||||

preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of individual preparing this return |

Address |

|

|

|

|

City |

|

|

|

|

|

State |

ZIP code |

|||||||

use |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Email address of individual preparing this return |

Telephone number |

|

Preparer’s NYTPRIN |

|

NYTPRIN |

Date |

||||||||||||||

(see instr.) |

|

|

|

( |

|

) |

|

|

|

|

|

|

|

|

excl. code |

|

|

|

|||

Where to file your return and attachments

Web File your return at www.tax.ny.gov (see Highlights in instructions).

(If you are not required to Web File, mail your return and attachments to: NYS Sales Tax Processing, PO Box 15168, Albany NY

If using a private delivery service rather than the U.S. Postal Service, see Publication 55, Designated Private Delivery Services.

|

December 10, 2021 |

New York State Sales Tax |

X,XXX.XX |

(your payment amount) |

|

|

|

Don’t forget to write your sales tax |

Don’t forget to |

ID number, |

sign your check |

Need help?

|

|

|

|

|

|

|

|

|

50000411210094 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See Form |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Document Specifics

| Fact Name | Description |

|---|---|

| Form Identification | ST-100 New York State and Local Quarterly Sales and Use Tax Return |

| Tax Period Covered | 3rd Quarter (September 1, 2021 – November 30, 2021) |

| Filing Due Date | Monday, December 20, 2021 |

| Web File Mandate | Most filers are required to use Sales Tax Web File |

| Instructions for Use | Refer to Form ST-100-I for detailed filing instructions |

| Final Return Indications | Indicate if the return is final due to sale, discontinuation, or change in business form |

| Credits Claiming | If claiming credits, mark the appropriate box and enter the total amounts of credits claimed |

| Governing Law | New York State Tax Law governs the requirements and conditions of the ST-100 form |

Guide to Writing Tax St 100

Filling out the New York State ST-100 Form is a necessary task for businesses reporting their quarterly sales and use tax. This process involves accurately detailing your gross sales, taxable sales, and applicable taxes while considering any changes in your business operation that might have occurred during the quarter. Here are the steps to guide you through this process and help ensure your filing is both accurate and compliant.

- Locate your Sales tax identification number and enter it at the top of the form.

- Under the section labelled "Legal name," print the ID number and legal name as they appear on your Certificate of Authority.

- If your address or business information has changed, mark an X in the corresponding box and provide the new or updated address details.

- If you have no taxable sales, taxable purchases, or credits to report for this period, enter none in Step 2 below.

- In the "Final return information" segment, indicate if your business has been sold or discontinued by marking an X in the appropriate box. Fill in the necessary information if this applies.

- Proceed to the "Calculate sales and use taxes" section. Here, you will need to enter itemized details of your taxable sales and purchases subject to tax, applying the correct tax rate for each taxing jurisdiction. Fill in columns A through F as instructed.

- Capture any calculated taxes due from special taxing districts, if applicable to your business operations, in Step 4.

- In Step 5, list any other tax credits, advance payments, or overpayments that apply to this return period.

- Calculate your total taxes due by adding your sales and use tax total to your total special taxes, then subtracting any total tax credits, advance payments, and overpayments.

- For businesses eligible, calculate the vendor collection credit or complete the information required if paying penalty and interest due to late filing or payment.

- Calculate the total amount due. If paying penalty and interest, include this in your total payment.

- Review your completed ST-100 form, ensuring all information is correct and you've signed where necessary.

- Mail your completed return by the due date listed on the form's header to avoid penalties. If you're filing online, follow the instructions for web submission provided by the New York State Department of Taxation and Finance.

Remember, accurate and timely filing of your ST-100 Form is crucial to remain in good standing with tax authorities and to avoid unnecessary penalties. Always keep a copy of your filed return for your records.

Understanding Tax St 100

FAQs about the ST-100 Form: New York State Quarterly Sales and Use Tax Return

What is the ST-100 form used for?

The ST-100 form is used by businesses to report and pay quarterly sales and use taxes to the New York State Department of Taxation and Finance. It covers the total sales, taxable sales, purchases subject to use tax, and calculates the sales and use taxes owed for the quarter.

When is the ST-100 form due?

The due date varies by quarter. For example, for the 3rd quarter (September 1 - November 30), the form is due by December 20 of the same year. It's crucial to check the specific quarter's due date to submit on time.

Who is required to file this form?

Most businesses with a sales tax permit in New York State are required to file the ST-100 form quarterly. This includes entities making taxable sales, leases, or rentals of tangible personal property and certain services.

What if I have no taxable sales for the quarter?

Even if you have no taxable sales or purchases subject to use tax during the quarter, you're still required to file the ST-100 form. You should enter "0" in the taxable sales and purchases sections.

Can I file the ST-100 form online?

Yes, the New York State Department of Taxation and Finance encourages or requires most filers to submit the ST-100 form via the Sales Tax Web File system. This online filing method is efficient and provides immediate confirmation of receipt.

How do I calculate what I owe?

To calculate the taxes owed, you'll need to enter your taxable sales and purchases subject to tax in the respective sections, apply the correct tax rates for your jurisdiction(s), and add up the total tax due. Special taxes and credits, such as for prepaid sales tax on cigarettes or overpayments, should also be factored into your calculations.

What if I sell or discontinue my business?

If you sell or discontinue your business, you're required to file a final ST-100 form within 20 days of the last day of business. You must mark the appropriate box indicating it's your final return and include the date of sale, sale price, and information about the purchaser if applicable.

Common mistakes

When completing the Tax St 100 form, which is a quarterly sales and use tax return for New York State, there are common mistakes that filers should diligently avoid to ensure their filing is accurate and compliant. By recognizing these errors, taxpayers can save time, avoid potential penalties, and ensure their tax reporting reflects their actual sales activity more accurately. Here are four of those mistakes:

- Incorrect Sales Tax Identification Number: One of the most critical pieces of information on the ST-100 form is the Sales Tax Identification Number. This number uniquely identifies your business and ensures that your payments and filings are correctly recorded. Entering an incorrect number can lead to processing delays or misapplied payments.

- Failing to Report All Taxable and Nontaxable Sales: All gross sales, both taxable and nontaxable, must be reported accurately. Some filers mistakenly report only taxable sales or omit nontaxable sales like wholesale sales, government sales, or sales for resale. Reporting comprehensive sales figures is essential for accurate tax calculations and compliance.

- Overlooking Jurisdiction Codes for Taxable Sales: The ST-100 form requires filers to break down their sales by jurisdiction to apply the correct tax rates. Many filers skip or inaccurately fill out this section, especially if they have sales across different counties or cities. Each jurisdiction has specific codes, and sales need to be allocated correctly to ensure the right tax amount is applied.

- Incorrectly Calculating Sales and Use Taxes: It's crucial to apply the correct tax rate to your taxable sales and purchases. Misinterpreting the tax rates for different jurisdictions or incorrectly adding taxable sales and purchases can result in underpaying or overpaying your taxes. Always double-check the current tax rates for each jurisdiction where you have made sales.

In addition to these common mistakes, it is equally important to make sure that the form is signed and filed by the due date to avoid penalties and interest. Ensuring accuracy in each step of filling out the ST-100 form not only complies with tax laws but also effectively manages your tax liabilities.

Documents used along the form

Filling out the Tax St 100 form, also known as the New York State and Local Quarterly Sales and Use Tax Return, often involves more than just completing this single document. Businesses might also need to handle several other forms and documents to ensure full compliance with tax regulations. Understanding these additional requirements can make the tax process smoother and more efficient.

- Form ST-100-I: This is the instruction booklet for the ST-100 form. It provides detailed guidelines on how to properly fill out the form, making sure businesses report their sales and use tax accurately.

- Form ST-100-ATT: This attachment is used if you're claiming any credits on your ST-100 return. It allows businesses to itemize and document these credits clearly.

- Form TP-153: Notice to Prospective Purchasers of a Business or Business Assets. Businesses intending to sell must provide this form to each potential buyer to disclose tax liabilities on the business or assets for sale.

- Form ST-330: Sales and Use Tax Advance Payment. This form is utilized for making advance payments on sales and use tax, typically required under specific conditions or for certain businesses.

- Certificate of Authority: Though not a form, it's an essential document for businesses to legally collect sales tax within New York State. A new Certificate of Authority is needed if the form of business changes.

- Schedules A, B, H, N, T, and W: These schedules are various attachments to the ST-100 form used to report specific types of sales or to break down sales by jurisdiction. Businesses fill them out based on their sales activities and locations.

Each of these documents plays a vital role in ensuring that businesses accurately report and pay their sales and use taxes. Proper completion and submission of these forms are crucial for compliance with New York State's tax laws, helping to avoid penalties and ensure a smooth operation of business activities related to taxation.

Similar forms

The IRS Form 941, Employer's Quarterly Federal Tax Return, is quite similar to the Tax St 100 form. Both forms are used to report quarterly tax information, although the 941 form pertains to federal tax liabilities for employers, including withheld income taxes, Social Security, and Medicare taxes, while the ST-100 is specific to sales and use tax in New York. Each serves a critical role in helping businesses comply with tax obligations on a quarterly basis.

The Form W-2, Wage and Tax Statement, also bears resemblance to the Tax St 100 form. While the W-2 is an annual report detailing the amount of wages paid and taxes withheld for each employee, the ST-100 involves quarterly reporting of sales and use tax. Both are crucial for tax reporting purposes: the W-2 for personal income taxation and the ST-100 for sales and use tax compliance by businesses operating in New York State.

Form 1099, particularly the 1099-MISC, is another document similar to the Tax St 100 form in that it is used for reporting specific types of payments, but unlike the ST-100's focus on sales and use tax, the 1099 series reports payments like rents, royalties, and non-employee compensation. Each form plays a vital role in the broader tax ecosystem by ensuring comprehensive reporting of financial transactions relevant to taxation.

The State Unemployment Tax Act (SUTA) filings share a commonality with the Tax St 100 form. Both involve periodic reporting to taxation authorities—SUTA on a quarterly basis for unemployment taxes by employers, and the ST-100 for sales and use taxes. SUTA filings contribute to state unemployment insurance funds, paralleling how sales and use taxes support state and local budgets.

The Schedule C (Form 1040), Profit or Loss From Business, is used by sole proprietors to report annual earnings and expenses from their business operations, akin to how businesses report quarterly sales and use taxes through the ST-100 form. Both documents are essential for tax calculations, with Schedule C affecting individual income tax obligations and ST-100 affecting business taxation at the state and local level.

The Business Property Tax statement, similar to various state forms that businesses use to declare personal property for tax purposes, shares its purpose with the ST-100 in the sense that both involve the reporting of values that lead to tax liabilities. Whereas the Business Property Tax statement focuses on the valuation of business-owned personal property, the ST-100 concentrates on transactions subject to sales and use tax.

Lastly, the Excise Tax Returns, which are filed for specific types of business activities or products, bear resemblance to the ST-100 form in their targeted approach to taxation. While excise taxes might apply to specific goods like alcohol, tobacco, or fuel, the ST-100 encompasses a broad array of goods and services subject to sales and use taxes in New York State.

Dos and Don'ts

When you're preparing to fill out the Tax ST-100 form for New York State, it's crucial to approach the task with a mixture of diligence and knowledge. This sales and use tax return, notably for quarterly periods, demands accuracy and attention to detail. To facilitate a smoother process, here's a compilation of things you should and shouldn't do:

Do:- Verify Your Information: Ensure that your sales tax identification number, legal name, business address, and DBA (doing business as) name are current and match the details on your Certificate of Authority.

- Report All Taxable Sales and Purchases: Accurately report your gross sales, taxable sales, and taxable purchases to avoid penalties for underreporting.

- Claim Eligible Credits: If you're eligible for credits, make sure to claim them by accurately completing Step 3 on the return form and attaching the required Form ST-100-ATT.

- Use the Correct Tax Rates: Apply the correct tax rate for each jurisdiction where you've made taxable sales or purchases. Each county or city may have different rates.

- Check for Special Taxes: Don’t overlook the calculation of special taxes in Step 4 if applicable to your business, such as taxes on vapor products or passenger car rentals.

- Review Before Submission: Carefully review your completed form for any errors or inaccuracies. Double-check your calculations and the completeness of the information provided.

- Sign and Date: Ensure the form is signed and dated. An unsigned form can be considered invalid and may result in processing delays or penalties.

- Miss the Deadline: Late filings can lead to penalties and interest charges. Ensure you mail the completed form or file it online by the due date indicated on the form.

- Estimate Figures: Avoid guessing or estimating figures. Use exact numbers where possible to ensure the accuracy of your return.

- Ignore Instructions: Failing to read the detailed instructions can lead to common mistakes. The instructions for Form ST-100 provide crucial guidance on how to complete each step properly.

- Forget to Report Non-Taxable Sales: Ensure you report non-taxable sales separately from taxable sales. This distinction is crucial for correct tax calculation.

- Omit Final Return Information: If you’re closing or selling your business, don’t forget to mark the form accordingly and provide the required final return information.

- Overlook Schedule Additions: If you have sales in multiple jurisdictions, ensure you complete all necessary schedules and include them with your return.

- Delay Addressing Discrepancies: If you notice discrepancies in your previously filed returns or payments, don't wait. Address these issues promptly to avoid compounding penalties.

By adhering to these guidelines, you can navigate the complexities of the Tax ST-100 form with greater confidence and accuracy, ensuring your business complies with New York State's taxation requirements.

Misconceptions

When it comes to navigating state tax forms, especially the New York State and Local Quarterly Sales and Use Tax Return (ST-100), there are several misconceptions that can lead to confusion, errors, and potentially costly mistakes for businesses. Here, we will clarify some common misunderstandings regarding the ST-100 form to ensure compliance and accuracy in filing.

Only businesses with a physical presence in New York need to file: One common misconception is that only businesses with a brick-and-mortar location in New York are required to file the ST-100 form. However, New York applies a "nexus" based approach, meaning that if you have a significant presence or economic nexus in the state, such as sales exceeding a certain threshold, you're required to file, regardless of physical presence.

Filing the ST-100 form is annual: The ST-100 form is a quarterly return, not annual. This means businesses need to file this form four times a year, covering sales and use tax collected in each quarter.

All sales must be reported on the ST-100 form: While the ST-100 form is used to report sales and use tax, not all sales are taxable. Businesses need to report total gross sales, but it's essential to differentiate between taxable and nontaxable sales on the form.

No tax due means no filing required: Even if a business did not collect any sales tax during the quarter, it is still required to file the ST-100 form, reporting "no tax due." Failure to file can result in penalties.

The ST-100 form only applies to goods: Both goods and services can be subject to sales tax in New York. The ST-100 form requires reporting on taxable sales of goods and services, depending on what's taxable under New York tax law.

Online Sales are exempt from ST-100 filing: The growth of e-commerce has blurred the lines of tax obligations. Online sales to New York residents may require filing the ST-100 form if your business has a nexus in New York.

The same tax rate applies to all sales: New York State has varied sales tax rates depending on the jurisdiction. The ST-100 form requires sales to be reported based on where the buyer takes possession of the goods or receives services, applying the correct tax rate accordingly.

One sales tax ID is enough for filing multiple ST-100 forms: If businesses operate under more than one entity or have different locations, they might need separate sales tax IDs and therefore might have to file separate ST-100 forms for each entity or location.

Business changes do not affect the ST-100 filing: Any significant changes, like selling or discontinuing the business, changing business structure, or changes in ownership, require specific reporting on the ST-100 form. Failing to report these changes can lead to inaccuracies and potentially penalties.

Credits or deductions are automatically calculated: It's the filer's responsibility to accurately account for and report any credits, deductions, and exemptions that the business is entitled to. These are not automatically calculated or applied when filing the ST-100 form.

Understanding these nuances can significantly impact how businesses approach their sales and use tax obligations in New York State. Correctly navigating the complexities of the ST-100 form is crucial for compliance and avoiding penalties. Always refer to the latest guidelines provided by the New York State Department of Taxation and Finance and consider consulting with a tax professional to ensure accuracy in your filings.

Key takeaways

Understanding the details and requirements of the ST-100 form, a New York State Quarterly Sales and Use Tax Return, is crucial for businesses to ensure compliance with state tax regulations. Here are key takeaways for efficiently managing this responsibility:

- The ST-100 form is designed for reporting taxable sales, services, and the collection of sales tax during the quarterly tax period. It's mandatory for businesses operating within New York State that are subject to sales tax.

- Filers are required to use the Sales Tax Web File system, indicating a push towards digital submissions for efficiency and ecological considerations. This mandate simplifies the process and allows for quicker processing of returns and payments.

- It is essential to report any changes in business information, such as a new address or a change in business status, on this form. Accurate and current information avoids processing delays and ensures that the Department of Taxation and Finance can provide timely updates and assistance.

- If your business has ceased operations or has been sold, the ST-100 form functions as a final return. This situation necessitates particular attention to detail, ensuring you report the taxable sales until the last day of business and handle the taxation of asset sales appropriately. Remember, this final return must be filed within 20 days following the cessation or sale of the business.

- For businesses applying tax credits or adjustments, precise calculation and documentation are required. This includes detailing any credits you're claiming and substantiating them with appropriate forms and records. Credits may impact the total tax due and need to be accurately reflected to maintain compliance and ensure correct tax liability.

In summary, the ST-100 form is a critical document for New York State businesses, requiring careful attention to details, including sales data, business changes, and potential tax credits. Properly managing this form promotes tax compliance, ensuring that businesses meet their state tax obligations without unnecessary complications.

Popular PDF Documents

Where Can I Get an Affidavit of Heirship Form - Directly contributes to the financial well-being of families, returning assets to the rightful owners.

Form 4506 - Form 4506 allows individuals and businesses to request copies of their tax documents from the IRS.