Get Tax POA m 2848 Form

Navigating the complexities of tax matters often requires the help of a professional, whether for advice, filing, or representation before the IRS. In such situations, the empowerment of an individual or organization to act on another's behalf becomes essential. This is where the Tax Power of Attorney (POA), formally recognized as Form 2848, comes into play. It serves as a crucial document, authorizing a designated professional—typically an accountant, attorney, or other tax professionals—to manage tax-related issues with the IRS on behalf of someone else. The form outlines specific details about the extent of power granted, including which tax matters and periods are covered. Understanding the roles, responsibilities, and limitations embedded within Form 2848 not only ensures compliance with IRS requirements but also facilitates a smoother interaction with tax matters, safeguarding one's financial health while navigating through the often intricate tax landscape.

Tax POA m 2848 Example

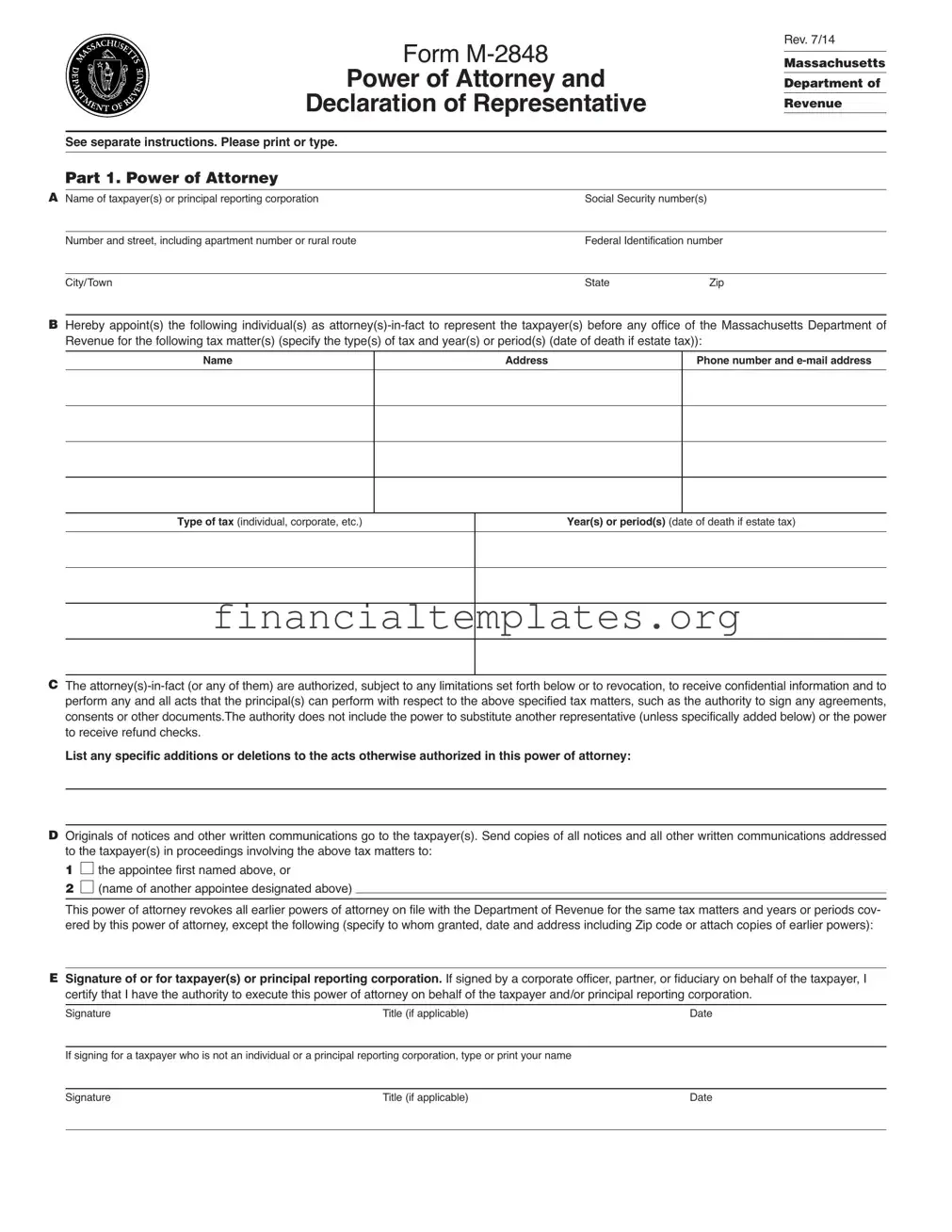

Form

Power of Attorney and

Declaration of Representative

Rev. 7/14

Massachusetts

Department of

Revenue

See separate instructions. Please print or type.

Part 1. Power of Attorney

A Name of taxpayer(s) or principal reporting corporation |

Social Security number(s) |

|

|

|

|

|

|

|

Number and street, including apartment number or rural route |

Federal Identification number |

|

|

|

|

|

|

City/Town |

State |

Zip |

BHereby appoint(s) the following individual(s) as

Name

Address

Phone number and

Type of tax (individual, corporate, etc.)

Year(s) or period(s) (date of death if estate tax)

CThe

List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

DOriginals of notices and other written communications go to the taxpayer(s). Send copies of all notices and all other written communications addressed to the taxpayer(s) in proceedings involving the above tax matters to:

1 □

the appointee first named above, or

the appointee first named above, or

2 □

(name of another appointee designated above)

(name of another appointee designated above)

This power of attorney revokes all earlier powers of attorney on file with the Department of Revenue for the same tax matters and years or periods cov- ered by this power of attorney, except the following (specify to whom granted, date and address including Zip code or attach copies of earlier powers):

ESignature of or for taxpayer(s) or principal reporting corporation. If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer and/or principal reporting corporation.

Signature |

Title (if applicable) |

Date |

If signing for a taxpayer who is not an individual or a principal reporting corporation, type or print your name

Signature |

Title (if applicable) |

Date |

|

|

|

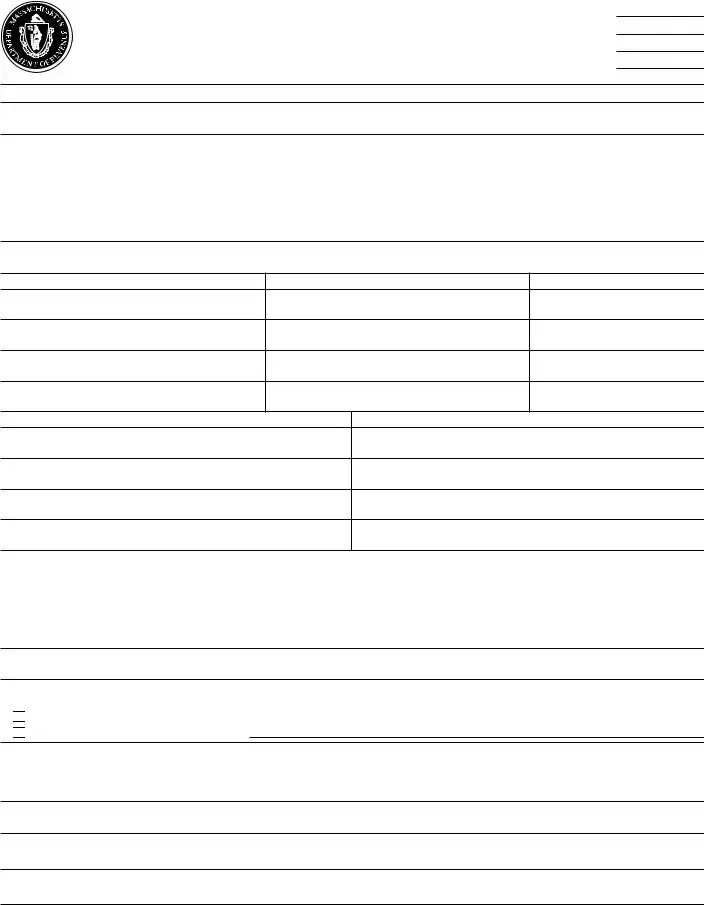

F If the power of attorney is granted to a person other than an attorney, certified public accountant, public accountant or enrolled agent, the taxpayer(s) signature must be witnessed or notarized below.

The person(s) signing as or for the taxpayer(s) (check and complete one):

D

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

Signature of witness |

Date |

|

|

Signature of witness |

Date |

|

|

D appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed. |

|

|

|

Signature of notary |

Date |

|

|

Part 2. Declaration of Representative. All representatives must complete this section.

I declare that I am not currently under suspension or disbarment from practice within the Commonwealth or in any jurisdiction, that I am aware of regula- tions governing the practice of attorneys, certified public accountants, public accountants, enrolled agents and others, and that I am one of the following:

1a member in good standing of the bar of the highest court of the jurisdiction shown below;

2duly qualified to practice as a certified public accountant or public accountant in the jurisdiction shown below;

3enrolled as an agent under the requirements of Treasury Department Circular No. 230;

4a bona fide officer of the taxpayer organization or principal reporting corporation;

5a

6a member of the taxpayer’s immediate family (spouse, parent, child or sibling);

7a fiduciary for the taxpayer;

8other (attach statement)

and that I am authorized to represent the taxpayer identified in Part 1 for the tax matters specified there.

Designation (insert appropriate

number from above list)

Jurisdiction (state, etc.)

or enrollment card number

Signature

Date

Made fillable by FormsPal.

printed on recycled paper

printed on recycled paper

Form

General Information

To protect the confidentiality of tax records, Massachusetts law generally prohibits the Department of Revenue from disclosing information contained in tax returns or other documents filed with it to persons other than the tax- payer or the taxpayer’s representative. For your protection, the Department requires that you file a power of attorney before it will release tax information to your representative. The power of attorney will also allow your represen- tative to act on your behalf to the extent you indicate. Use Form

You may use Form

For certain corporate excise matters under MGL ch 63. By executing this agreement an officer of a principal reporting corporation filing under MGL ch 63, § 32B represents that the principal reporting corporation is authorized to execute this agreement as agent for all corporations that par- ticipated in, or were required to participate in, such filing for any component of the corporate excise reported or required to be reported under any sec- tion of MGL ch 63 by any such corporation whether relating to the income measure,

A principal reporting corporation acts on behalf of all corporations that partic- ipated in, or were required to participate in, a filing under MGL ch 63, § 32B, as stated in the preceding paragraph. Consequently, in the case of such a filing by a principal reporting corporation, the references in this agreement to “taxpayer(s)” shall include all such corporations.

Filing the Power of Attorney. You must file the original, a photocopy or facsimile transmission (fax) of the power of attorney with each DOR office in which your representative is to represent you. You do not have to file another copy with other DOR officers or counsel who later have the matter under consideration unless you are specifically asked to provide an addi- tional copy.

Revoking a Power of Attorney. If you previously filed a power of attorney and you want to revoke it, you may use Form

If you want to revoke a power of attorney without executing a new one, send a signed statement to each office of DOR in which you filed the earlier power of attorney you are now revoking. List in this statement the name and address of each representative whose authority is being revoked.

How to Complete Form

Part 1. Power of Attorney

A. Taxpayer’s name, identification number and address.

a.For individuals.Enter you name, social security number and address in the space provided. If joint returns involved, and you and your spouse are designating the same representative(s), also enter your spouse’s name and social security number and your spouse’s address (if different).

b.For a corporation, partnership or association.Enter the name, federal identification number and business address. If the Power of Attorney for a partnership will be used in a tax matter in which the name and social secu- rity number of each partner have not previously been sent to DOR, list the name and social security number of each partner in the available space at the end of the form or on an attached sheet.

c. For a principal reporting corporation. Enter the name, federal identifi- cation number and business address of the principal reporting corporation.

d. For a trust. Enter the name, title and address of the fiduciary, and the name and federal identification number of the trust.

e. For an estate. Enter the name, title and address of the decedent’s per- sonal representative, and the name and identification number of the estate. The identification number for an estate is the decedent’s social security number and includes the federal identification number if the estate has one.

B.Appointee(s) and tax matters and years or periods.Enter the name(s), address(es) and telephone number(s) of the individual(s) you appoint. Your representative must be an individual and may not be an organization, firm or partnership.

Consider each tax imposed by the Commonwealth for each tax period as a separate tax matter. In the columns provided, clearly identify the type(s) of tax(es) and the year(s) or period(s) for which the power is granted. You may list any number of years or periods and types of taxes on the same power of attorney. If the matter relates to estate tax, enter the date of the taxpayer’s death instead of the year or period.

If the power of attorney will be used in connection with a penalty that is not related to a particular tax type, such as personal income or corporate, enter the section of the General Laws which authorizes the penalty in the “type of tax” column.

C. Powers granted by Form

If you do not want your representative to be able to perform any of these or other specific acts, or if you want to give your representative the power to delegate authority or substitute another representative, insert language ex- cluding or adding these acts in the blank space provided.

D. Where you want copies to be sent. The Department of Revenue rou- tinely sends originals of all notices to the taxpayer. You may also have copies of all notices and all other written communications sent to your rep- resentative. Please check box 1 if you want copies of all notices or all com- munications sent to the first appointee named at the top of the form. Check box 2 if you want copies sent to one of your other appointees. In this case, list the name of the appointee.

E. Signature of taxpayer(s). For individuals: If a joint return is involved and both spouses will be represented by the same individual(s), both must sign the power of attorney unless one authorizes the other (in writing) to sign for both. In that case, attach a copy of the authorization. However, if the spouses are to be represented by different individuals, each may execute a power of attorney.

For a partnership: All partners must sign unless one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if under state law the partner has authority to bind the partnership.

For a corporation or association: An officer having authority to bind the en- tity must sign.

For a principal reporting corporation: An officer having authority to bind the principal reporting corporation of a combined group.

If you are signing the power of attorney for a taxpayer who is not an indi- vidual, such as a corporation or trust, please type or print your name on the line below the signature line at the bottom of the form.

F. Notarizing or witnessing the power of attorney. A notary public or two individuals with no stake in the tax matter must witness a power of at- torney unless it is granted to an attorney, certified public accountant, public accountant or enrolled agent.

Part 2. Declaration of Representative

Your representative must complete Part 2 to make a declaration containing the following:

1.A statement that the representative is authorized to represent you as a certified public accountant, public accountant, attorney, enrolled agent, member of your immediate family, etc. If entering “eight” in the “designation” column, attach a statement indicating your relationship to the taxpayer.

2.The jurisdiction recognizing the representative, if applicable. For an attor- ney, certified public accountant or public accountant: Enter in the “jurisdic- tion” column the name of the state, possession, territory, commonwealth or District of Columbia that has granted the declared professional recogni- tion. For an enrolled agent: Enter the enrollment card number in the “juris- diction” column.

3.The signature of the representative and the date signed.

Document Specifics

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA Form 2848 is used to authorize an individual, typically a tax professional, to represent a taxpayer before the IRS. |

| Scope of Authority | This form lets the appointed individual perform tasks such as requesting tax records, communicating with the IRS, and representing the taxpayer in audits, appeals, and collection matters. |

| State-Specific Forms | Some states have their own version of a tax power of attorney form, which may be governed by state tax law. Taxpayers should use their state’s specific form when dealing with state tax matters. |

| Duration | The duration of the authorization is typically noted on the form itself and can be specified by the taxpayer. It usually ends automatically at a set future date or upon completion of the specified tax matter. |

Guide to Writing Tax POA m 2848

When preparing to handle tax matters, it's crucial to properly complete the Tax Power of Attorney (POA) Form M-2848. This form grants authority to an individual, typically a tax professional or attorney, to discuss and manage tax affairs on your behalf with the tax authorities. Accuracy and attention to detail in filling out this document are paramount to ensure that the powers granted reflect your wishes without any misunderstandings. Following a step-by-step approach ensures the process is handled efficiently and correctly.

Steps for Filling Out the Tax POA M-2848 Form

- Identify the Taxpayer: Start by providing the complete name, social security number (SSN), or employer identification number (EIN) of the taxpayer. If the POA is for a married couple filing jointly, include information for both individuals.

- Appoint the Representative(s): Enter the name(s), mailing addresses, and telephone numbers of the individual(s) being authorized as representative(s). If designating more than one representative, indicate whether they are required to act together.

- Specify Tax Matters: Clearly outline the specific tax matter(s) your representative will have the power to handle. This includes the type of tax, the tax form number, and the year(s) or period(s) involved.

- Define the Power of Attorney’s Scope: Detail the extent of authority you are granting to your representative, including any specific powers you do not wish to grant. It is important to be as precise as possible to avoid any confusion or unintended authority.

- Include Any Additional Acts Authorized: If applicable, list any additional acts you authorize your representative to perform on your behalf. This section can include requests for confidential tax information or the authority to negotiate and sign agreements with the tax authorities.

- Retention/Revocation of Prior POAs: Indicate whether you wish to retain any previously filed power(s) of attorney. If you choose not to retain them, this will automatically revoke all prior POAs upon filing this document.

- Sign and Date the Form: The taxpayer(s) must sign and date the form. If filing jointly, both spouses need to sign if they are both granting authority to the representative(s). Ensure that the date of signature is current, as outdated forms may be rejected.

- Representative’s Declaration: The representative(s) designated in the form must complete the declaration section, which includes providing their tax identification number(s), address, and phone number. They must also sign and date the form, agreeing to the declarations made.

After completing the Tax POA M-2848 form, it should be submitted to the appropriate tax authority, as directed in the instructions. The process of granting power of attorney for tax matters is a significant step that allows your representative to communicate with tax agencies on your behalf and make important decisions. Ensuring that the form is filled out accurately and thoroughly will facilitate a smoother interaction with tax authorities and help in managing your tax-related issues more effectively.

Understanding Tax POA m 2848

What is the Tax POA Form 2848?

The Tax Power of Attorney (POA) Form 2848 is a document that grants an individual or organization the authority to represent another person in matters related to the Internal Revenue Service (IRS). This form allows the appointed representative to receive confidential tax information and take actions such as signing agreements, making requests, and providing responses to the IRS on behalf of the taxpayer.

Who can be appointed as a representative on Form 2848?

Individuals eligible to be appointed as representatives include attorneys, certified public accountants (CPAs), enrolled agents, enrolled retirement plan agents, and enrolled actuaries. The representative must have the authorization to practice before the IRS. It's important that the person chosen is trusted and has the necessary qualifications to handle tax matters competently.

How can I complete Form 2848?

To complete Form 2848, you must provide your name, taxpayer identification number (e.g., Social Security Number), and the tax matters and years or periods you want the representation to cover. Additionally, you need to specify the name and credentials of the appointed representative, their CAF number (if they have one), their address, and telephone number. Both the taxpayer and the representative must sign and date the form.

What tax matters can be covered by Form 2848?

Form 2848 can cover a wide range of tax matters including, but not limited to, federal income, gift, and estate taxes. It can also specify particular years and types of forms. Be precise in describing the tax matters, years, and forms to ensure that the authorization is accurately matched to your needs.

Is there a validity period for Form 2848?

Yes, Form 2848 remains valid until the expiration date specified by the taxpayer on the form. If no expiration date is provided, it will remain in effect until it is revoked. It is recommended to review and, if necessary, update your Form 2848 periodically to ensure it reflects current authorizations and representative information.

Can I revoke a previously filed Form 2848?

Yes, you can revoke a previously filed Form 2848 by submitting a new Form 2848 with box 6 checked, indicating that the previous authorization is revoked. Additionally, writing a statement of revocation detailing the extent of revocation and mailing it to the IRS can also effectively revoke the form.

Where do I send the completed Form 2848?

The completed Form 2848 should be sent to the IRS office handling the matter. If there is no current matter pending, you can find the appropriate IRS address based on your location by referring to the instructions for Form 2848. This ensures the form is processed promptly and linked to the taxpayer's records accurately.

Can Form 2848 be used for state tax matters?

No, Form 2848 is specifically designed for authorizing representation only before the IRS relating to federal tax issues. For state tax matters, you will need to check with your state's tax agency to see if they have a similar form or process for authorizing representation.

Common mistakes

Filling out the Tax Power of Attorney (POA), IRS Form 2848, can be a nuanced task. Given its importance in granting someone else the authority to handle your tax matters, precision is critical. Unfortunately, errors are not unusual. Here are six common mistakes that people tend to make:

Not specifying the tax form number. It's essential to detail the specific tax forms your representative will have access to. Without this clarity, the IRS may not recognize the POA for your intended purposes.

Failing to define the tax years or periods. The POA needs clear dates. If the dates are too broad or incorrectly listed, it may limit your representative's ability to effectively manage your taxes.

Including incorrect taxpayer information. Even simple mistakes in your name, address, or Social Security Number (SSN) can invalidate the POA. Accuracy is non-negotiable.

Omitting the representative's qualifications. Whether your representative is an attorney, a certified public accountant, or holds another designation, their qualifications must be explicitly identified.

Forgetting to sign and date the form. An unsigned form is as good as not having one. Your signature, along with the date, confirms your consent to the POA and its stipulations.

Not using the most current form. The IRS updates forms regularly. Using an outdated version can lead to processing delays or the form being outright rejected.

Avoiding these errors can greatly streamline the process, ensuring that your tax affairs are managed efficiently and in accordance with your wishes. Remember, when in doubt, consulting with a tax professional can provide valuable guidance and peace of mind.

Documents used along the form

When dealing with tax matters, particularly when authorizing someone else to handle these affairs on one's behalf, a Tax Power of Attorney (POA) Form 2848 is crucial. This form allows an individual to grant authority to a tax professional or other designated representative to communicate with the IRS, obtain confidential tax information, and perform actions like signing agreements. However, this form is often just one component of a suite of documents needed to manage tax issues comprehensively or when dealing with broader financial or legal tasks. Below are seven additional forms and documents that are frequently used alongside Form 2848.

- Form 8821, Tax Information Authorization - This document grants permission to another party to access tax information, but not to represent the taxpayer to the IRS. It's useful for tax preparers or financial advisors who need tax information to provide advice or prepare tax returns.

- Form 1040, U.S. Individual Income Tax Return - The primary form used by individuals to file their annual income tax returns. It's often connected to the POA process because the designated representative might need to review, prepare, or amend these returns on behalf of the taxpayer.

- Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return - This form is required for reporting the estate of a deceased person. A legal representative might need a Power of Attorney to complete and file this return, particularly in complicated estate situations.

- Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return - Used to report gifts that exceed the annual exclusion amount. Similar to estate returns, managing gift tax obligations might necessitate a Power of Attorney.

- Form 941, Employer's Quarterly Federal Tax Return - For business owners, this form is essential for reporting payroll taxes. A POA might be required if a tax professional or other representative is managing a business's payroll duties.

- Form 990, Return of Organization Exempt From Income Tax - Non-profits file this form to maintain their tax-exempt status. Managers of non-profit organizations may need to grant POA to ensure accurate filing and compliance.

- Form W-9, Request for Taxpayer Identification Number and Certification - Often used in business transactions, this form provides a taxpayer identification number. A representative might need to manage or submit W-9 forms on behalf of an individual or business, especially in complex financial situations.

A Power of Attorney for tax matters, symbolized through Form 2848, serves as a cornerstone document, empowering individuals to ensure their tax affairs are managed appropriately and efficiently, even in their absence. The complementary forms mentioned provide a framework to address specific tax-related tasks or broader financial responsibilities. In totality, these documents facilitate a comprehensive approach to managing tax obligations, complying with tax laws, and strategically planning for one's financial future. Understanding the role and importance of each can significantly ease the process of tax planning and management.

Similar forms

The Tax Power of Attorney (POA) Form 2848 is akin to the General Power of Attorney document, as both establish a legal relationship where one party grants another party the authority to act on their behalf. The General Power of Attorney, however, is broader, allowing the agent to make decisions across a wide range of the principal's affairs, not limited to tax matters. This distinction delineates the tax-focused intent of Form 2848 from the more universal applicability of the General Power of Attorney.

Similarly, the Durable Power of Attorney resonates with the essence of the Tax POA Form 2848. The key attribute they share is the enduring nature of the authority granted, where the Durable Power of Attorney remains in effect even if the principal becomes incapacitated. Nevertheless, the scope of the Durable Power of Attorney extends beyond tax issues to encompass financial and health-related decisions, differentiating it by its broader purview compared to the tax-specific mandate of Form 2848.

The Limited Power of Attorney document parallels the Tax POA Form 2848 in that it confers a narrowly defined authority from the principal to the agent. Whereas the Tax POA focuses exclusively on tax-related matters, a Limited Power of Attorney could be tailored to any specific task or decision. The similarity lies in the precise limitation of powers granted, although the nature of these powers can vary widely outside of the tax realm.

The Healthcare Power of Attorney shares with Form 2848 the critical element of representation. In both documents, an individual designates someone else to act on their behalf. However, while the Tax POA pertains strictly to tax matters, a Healthcare Power of Attorney is designed exclusively for making medical decisions when the principal is unable to do so. This fundamental difference in focus underscores the varying contexts in which such delegated authority operates.

Form 2848 also bears resemblance to the Springing Power of Attorney, with both types of POA activating under specified conditions. Form 2848 takes effect upon submission and acceptance by the IRS, granting tax representation rights. Conversely, a Springing Power of Attorney becomes effective only upon the occurrence of a predetermined event, often the principal's incapacitation, showing how conditional triggers play a crucial role in activating these powers.

The Financial Power of Attorney aligns with the Tax POA in its purpose to manage the principal's affairs, specifically in financial matters. The Tax POA Form 2848 is a subset of financial powers, strictly dealing with tax issues. This indicates a shared domain but also highlights the specialized focus of Form 2848 within the broader spectrum of financial management represented by a Financial Power of Attorney.

A Business Power of Attorney and the Tax POA Form 2848 share common ground in the aspect of operating within specific spheres of authority. A Business Power of Attorney allows an agent to make business-related decisions, similar to how Form 2848 enables tax-related decisions. The core similarity is the delegation of specific types of decisions, emphasizing the strategic specialization in each document.

The Real Estate Power of Attorney and Tax POA Form 2848 both involve delegation for transactions, albeit in different arenas. While the Real Estate Power of Attorney permits an agent to handle buying, selling, and managing property, Form 2848 limits the agent's authority to tax matters. Nevertheless, both documents streamline the process by empowering another to act within defined boundaries, demonstrating how delegation is tailored to particular needs and contexts.

Dos and Don'ts

When handling the Tax Power of Attorney Form, also known as Form 2848, one is often navigating the intersection of legal authority and personal financial matters. This form allows you to grant a trusted individual the power to engage with the IRS on your behalf. To ensure the process is smooth and effective, it's essential to understand what to do and what not to do. Below are some guidelines to follow.

- Do ensure that all information provided is accurate and complete. This includes your full name, address, and taxpayer identification number (usually your Social Security Number), as well as the same information for your appointed representative.

- Don't forget to specify the tax matters and years/forms. You must indicate the specific tax forms or years you're granting your representative authority over. Vagueness can lead to unnecessary confusion or limitations on your representative's ability to act on your behalf.

- Do select the right representative. Your representative should be someone you trust, ideally with a professional background relevant to your tax matters, such as an accountant or tax attorney.

- Don't use the form for non-tax matters. Form 2848 is specifically designed for tax-related representations and should not be used as a general power of attorney form.

- Do sign and date the form. An original signature is required for the IRS to accept and process the form. Electronic signatures may not be accepted unless they meet specific IRS standards.

- Don't overlook the declaration of representative section. Your representative must complete this section, certifying they are eligible to represent you before the IRS. They must also provide their PTIN (Preparer Tax Identification Number).

- Do keep a copy for your records. After submitting Form 2848 to the IRS, make sure to retain a copy for yourself. This document is an important record of who has legal authority to deal with your taxes.

- Don't submit the form without reviewing it for errors. A simple mistake can delay processing or invalidate your form, so review it carefully before submission.

- Do use the most current form available. Tax laws and forms can change. Always use the latest version of Form 2848 to ensure compliance with current guidelines and requirements.

Properly executed, Form 2848 can empower someone with the necessary authority to act on your behalf in matters concerning the IRS, saving you time and potentially resolving issues more efficiently. Attention to detail and adherence to the above dos and don'ts will help streamline this process.

Misconceptions

The Tax Power of Attorney, more formally known as Form 2848, is an important document that allows an individual to authorize someone else to represent them before the Internal Revenue Service (IRS). However, there are several misconceptions surrounding this form that can complicate its understanding and use. Let's clarify some of these misunderstandings.

Only a lawyer can be your representative on Form 2848. This is a common misconception. In reality, the IRS allows various professionals to act as your representative. This list includes certified public accountants (CPAs), enrolled agents, and in some cases, family members. What matters is that the individual has the knowledge and qualifications to deal with tax matters effectively and ethically.

Form 2848 grants unlimited power to the representative. Although Form 2848 does give the representative the authority to perform a wide range of tax-related tasks on behalf of the taxpayer, its scope can be limited. The taxpayer has the power to restrict the form’s authority to specific issues, tax forms, or tax periods. This control helps safeguard the taxpayer's interests.

Once submitted, Form 2848 is irrevocable. This is not the case. A taxpayer can revoke a Power of Attorney (POA) at any time. This revocation can be accomplished either by submitting a new Form 2848 or by writing to the IRS office where the original was filed, clearly stating the desire to revoke the authorization and identifying the specific POA document by its date.

Filing Form 2848 automatically resolves tax issues. Filing this form is simply the first step in authorizing someone to assist with your tax matters. It does not, in itself, resolve any tax issues. The representative’s effectiveness in handling your tax affairs will depend on their expertise, the specific authorities granted by the form, and their ability to work with the IRS to address any concerns or disputes.

Form 2848 is only for individuals. This misconception overlooks the versatility of Form 2848. It can be used not only by individuals but also by businesses, estates, and trusts to authorize representation before the IRS. This wide applicability makes it a powerful tool for taxpayers of all types to ensure their tax matters are handled appropriately.

There is no expiration for Form 2848. In fact, Form 2848 does include a line for the taxpayer to specify the duration of the authorization. If no duration is specified, the IRS generally considers the authorization valid for five years from the date the form is received. It’s important for both taxpayers and their representatives to be mindful of this timeframe to ensure continuous representation if needed.

Understanding these nuances about Form 2848 can demystify the process of granting power of attorney for tax purposes, allowing taxpayers to make informed decisions about their representation before the IRS. When used correctly, this form can be an invaluable resource in managing and resolving tax affairs with greater ease and confidence.

Key takeaways

Filling out and using the Tax Power of Attorney (POA) Form 2848 correctly is crucial for individuals who want to grant someone else the authority to handle their tax matters with the Internal Revenue Service (IRS). Here are five key takeaways to ensure proper completion and use of this form:

Identify the representative clearly: Form 2848 requires you to provide detailed information about the representative you are appointing. This includes their name, address, and phone number, as well as their Preparer Tax Identification Number (PTIN) or other acceptable identification numbers. Make sure all the information is accurate to avoid any confusion or processing delays.

Specify the tax matters: The form allows you to define the specific tax forms, years, or periods you are giving the representative authority over. Be as precise as possible. If the document is too vague, the IRS may not accept it. For example, instead of saying "all tax years," specify the exact years you want the representative to handle, such as "2020, 2021, and 2022."

Understand the authority you're granting: By signing Form 2848, you're allowing the representative to receive your confidential tax information and to act on your behalf in matters before the IRS. However, there are limits to their authority. For instance, your representative cannot endorse or negotiate checks issued by the Treasury Department on your behalf unless specifically authorized in the document.

Both parties must sign the form: For Form 2848 to be valid, both you (the taxpayer) and your appointed representative must sign and date the form. Incomplete forms lacking either signature will not be processed by the IRS, leading to delays or rejection of your POA request.

Submit the form to the right IRS office: Once completed, you must send Form 2848 to the appropriate IRS office. The correct office depends on your state of residence and the specific tax matter involved. The IRS provides a list of where to file, which can be found on their website or in the instructions accompanying Form 2848. Sending the form to the wrong office can result in processing delays.

Proper completion and understanding of Form 2848 can smooth the process of handling tax matters through a representative, ensuring that your tax affairs are managed effectively and in accordance with your wishes.

Popular PDF Documents

What Businesses Need to File Form 720 - It's important for new businesses to determine if their operations require filing the IRS 720 form to start on the right foot with tax obligations.

Lgl-001 - Completing the Tax Power of Attorney form is a proactive step in safeguarding one's financial health and ensuring compliance with tax laws.