Get Tax Benefits Application Form

Exploring the Tax Benefits Application form can feel like navigating through a maze of criteria and deadlines, yet it holds the key to potential savings for various homeowners. This form includes a range of exemptions, each with its unique set of eligibility requirements, be it for veterans, clergy members, or those owning properties in specific housing developments. Veterans need to focus on their service period and discharge status, alongside the primary residence requirement. On the other hand, clergy members must prove their status and, if applicable, their age or health conditions. It's not just about filling out the form; applicants must provide supporting documents like the DD214 for veterans, marriage certificates, or proof of clergy status. Deadlines are strict, with the application for the tax year 2018/19 requiring postmarking by March 15, 2018. Moreover, the application process touches on several aspects of homeownership from primary residence verification, information about additional properties, to the specifics of cooperative ownership and properties held in trust or life estates—each element ensuring that the right benefits go to the eligible applicants. All in all, navigating the Homeowner Tax Benefits Application is a careful process of understanding eligibility, gathering necessary documentation, and meeting deadlines to secure valuable exemptions.

Tax Benefits Application Example

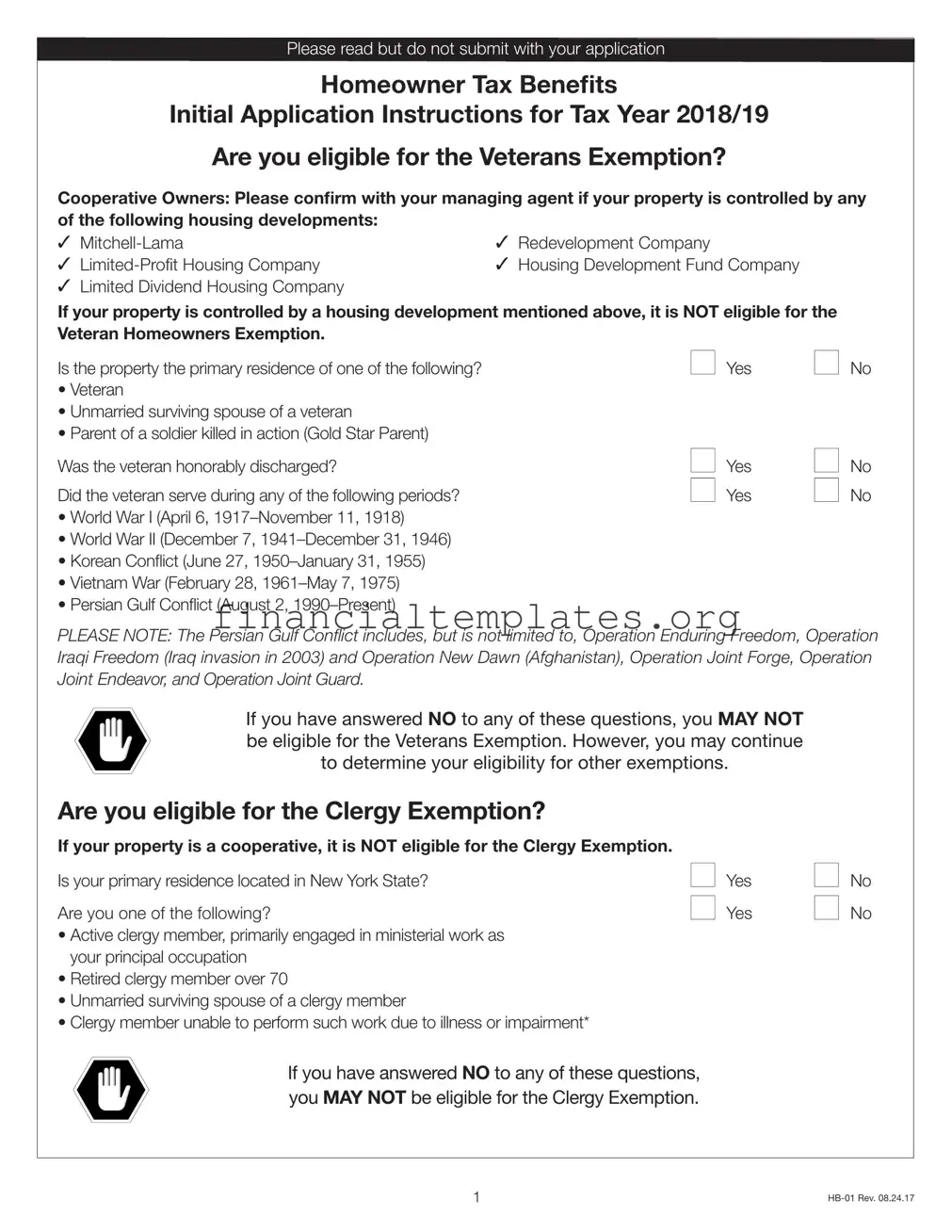

Please read but do not submit with your application

Homeowner Tax Benefits

Initial Application Instructions for Tax Year 2018/19

Are you eligible for the Veterans Exemption?

Cooperative Owners: Please confirm with your managing agent if your property is controlled by any of the following housing developments:

✓ |

✓ |

Redevelopment Company |

|

✓ |

✓ |

Housing Development Fund Company |

✓Limited Dividend Housing Company

If your property is controlled by a housing development mentioned above, it is NOT eligible for the

Veteran Homeowners Exemption. |

|

|

Is the property the primary residence of one of the following? |

n Yes |

n No |

• Veteran |

|

|

• Unmarried surviving spouse of a veteran |

|

|

• Parent of a soldier killed in action (Gold Star Parent) |

|

|

Was the veteran honorably discharged? |

n Yes |

n No |

Did the veteran serve during any of the following periods? |

n Yes |

n No |

• World War I (April 6, |

|

|

• World War II (December 7, |

|

|

• Korean Conflict (June 27, |

|

|

• Vietnam War (February 28, |

|

|

• Persian Gulf Conflict (August 2, |

|

|

PLEASE NOTE: The Persian Gulf Conflict includes, but is not limited to, Operation Enduring Freedom, Operation Iraqi Freedom (Iraq invasion in 2003) and Operation New Dawn (Afghanistan), Operation Joint Forge, Operation Joint Endeavor, and Operation Joint Guard.

If you have answered NO to any of these questions, you MAY NOT be eligible for the Veterans Exemption. However, you may continue to determine your eligibility for other exemptions.

Are you eligible for the Clergy Exemption?

If your property is a cooperative, it is NOT eligible for the Clergy Exemption.

Is your primary residence located in New York State?

Are you one of the following?

•Active clergy member, primarily engaged in ministerial work as your principal occupation

•Retired clergy member over 70

•Unmarried surviving spouse of a clergy member

•Clergy member unable to perform such work due to illness or impairment*

n n

Yes

Yes

n n

No

No

If you have answered NO to any of these questions, you MAY NOT be eligible for the Clergy Exemption.

1 |

Important Information

1. Deadline – March 15, 2018:

The Homeowner Tax Benefit Application and required documents must be postmarked by March 15, 2018, for benefits to begin on July 1st. If the deadline falls on a weekend or a holiday, the deadline will be the next business day.

2. Property information:

Provide the complete address and the borough, block and lot (BBL) number of the your property for which you are seeking tax benefits and the date you purchased the property. The borough, block and lot numbers for properties can be found on the Department of Finance website at nyc.gov/bbl, on your deed or property tax bill.

Properties owned by trust or life estate:

If the property has a life estate, only the individual retaining the life estate can apply. If the property is held in a trust, only the qualifying beneficiary/trustee can apply. (Veterans Exemption Only)

Properties owned by a business:

If your property is owned by a business, it is not eligible for Homeowner Tax Benefits.

3. Primary residence:

Your primary residence is your principal and permanent place of residence. You can have only one primary residence but may own more than one property. Please provide documents if you were absent from the property due to medical reasons or institutionalization.

Percentage Used As Primary Residency (Veterans Exemption Only):

If your property contains four or more residential units, indicate the percentage used as your primary residency. Example: if the property is a

4. Owner information:

Please complete the entire section for all owners and their spouses. If you are a foreign national, please provide your Individual Taxpayer Identification Number (ITIN).

5. Transfer of Veterans Exemption:

If you received a Veterans Exemption on a property and can show proof that your previous residence was granted the exemption, you may be able to transfer the exemption to a new property. Both residences must be located in New York State. The application must be received within 30 days of the purchase of the new property. To qualify for the following tax year the application must be postmarked on or before March 15th. If the property is granted the exemption it will be prorated.

6. Additional Property Information:

If you own an additional property outside of NYC and are no longer receiving benefits, you must submit a letter from the county/state local assessor’s office indicating there are no benefits on your other property. If you or your spouse own additional/multiple properties, please complete the “Additional Property Information” section on pages 3 and 4 of the application.

2 |

7. Submission of the Homeowner Tax Benefit application:

Send the original application and COPIES of the required documentation to:

NYC Department of Finance

P.O. Box 311

Maplewood, NJ

Application and all required documentation must be postmarked by March 15, 2018. Keep a copy of your application for your records. You will receive an acknowledgment letter from the Department of Finance when your application is received.

Required Documention (2018/19)

Proof of Veteran Status

•COPY of DD214 or its equivalent

•COPY of Separation papers

NOTE: The DD214 (or its equivalent) and/or separation papers are REQUIRED and must be submitted with the application.

AND COPIES of one of the following, if applicable:

•Marriage certificate, if a spouse is applying for the exemption based on the military service of the veteran and the veteran is not on the deed.

•Death certificate, if you are an unmarried surviving spouse or Gold Star parent.

•Veterans Administration award letter with service connected disability rating, if the veteran is disabled.

To obtain DD214 and separation papers, contact:

National Personnel Records Center 1 Archives Drive

St. Louis, Missouri 63138 www.archives.gov/veterans (866)

Proof of Clergy Status

• Verification letter from the house of worship employer on official letterhead.

AND COPIES of one of the following, if applicable:

•Death certificate, if you are an unmarried surviving spouse.

•Physician letter documenting illness or impairment, if the clergy member is unable to perform work for his/her denomination due to illness or impairment.

•Proof of age, if the clergy member is retired and over 70 years of age.

NOTE: Additional documentation may be needed in the following cases:

•If the property is a cooperative, please provide a COPY of the stock certificate.

•If the property is held in a trust, please submit a COPY of the trust agreement. (FOR VETERANS ONLY)

•If the property was willed to an owner, please submit a COPY of last will and testament, probate or court order.

3 |

Homeowner Tax Benefits

INITIAL APPLICATION FOR TAX YEAR 2018/19

This application and ALL REQUIRED DOCUMENTS must be

submitted and postmarked by March 15, 2018.

Please be sure that ALL HOMEOWNERS sign the Certification section of this application on page 4.

Mail completed application to:

New York City Department of Finance, P.O. Box 311, Maplewood, NJ

This application is for the following homeowner property tax benefit programs:

Which exemption(s) are you applying for? (Check all that apply)

n Veterans |

n Clergy |

If you need help or have any questions about this application,visit

nyc.gov/contactpropexemptions, or call 311.

If you do not send in ALL REQUIRED DOCUMENTS by this deadline,

there will be a delay in the processing of your application.

PLEASE PRINT

1. PROPERTY INFORMATION

BOROUGH |

|

BLOCK |

|

|

LOT |

|

|

|

# OF COOPERATIVE SHARES |

|

|

|

|

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

|

|

|

|

|

APT. |

|

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

|

STATE |

|

|

|

ZIP |

|

|

|

|

|

|

|

|

|

|||

TYPE OF PROPERTY |

n Condominium unit |

n |

|

|

|

|||||

|

n Cooperative |

n |

4+ family dwelling |

DWELLINGS WITH 4 OR MORE UNITS, ENTER |

|

|||||

|

|

|

|

|

|

% OF SPACE USED FOR PRIMARY RESIDENCE: ____________ % |

||||

|

|

|

|

|

|

|

||||

DATE YOU PURCHASED THE |

|

|

COOPERATIVE/CONDO MANAGEMENT INFORMATION |

|

||||||

PROPERTY (mm/dd/yyyy) |

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY NAME |

|

|

|

|

TELEPHONE |

( |

) |

– |

|

|

|

|

|

|

|

NUMBER |

|||

|

|

|

|

|

|

|

|

|||

IS THIS PROPERTY USED EXCLUSIVELY FOR RESIDENTIAL PURPOSES? |

|

|

|

n Yes |

n No |

|||||

IF NO: PROVIDE % USED FOR |

|

|

|

|||||||

IS THERE A LIFE ESTATE ON THIS PROPERTY? |

|

|

|

|

|

|

n Yes |

n No |

||

|

|

|

|

|

|

|

|

|

||

IS THERE A TRUST ON THIS PROPERTY? (FOR VETERANS ONLY) |

|

|

|

|

|

n Yes |

n No |

|||

|

|

|

|

|

|

|

|

|

||

WAS THE PROPERTY WILLED TO YOU? |

|

|

|

|

|

|

n Yes |

n No |

||

|

|

|

|

|

|

|

|

|

||

1 |

Homeowner Tax Benefits INITIAL APPLICATION — 2018/19

For Proof of Veteran Status

•COPY of DD214 or its equivalent

•COPY of Separation papers

NOTE: The DD214 (or its equivalent) and/or separation papers is REQUIRED and must be submitted with the application.

AND COPIES of one of the following, if applicable:

•Marriage certificate, if a spouse is applying for the exemption based on the military service of the veteran and the veteran is not on the deed.

•Death certificate, if you are an unmarried surviving spouse or Gold Star parent.

Veterans Administration award letter with service connected disability rating, if the veteran is disabled

•For a life estate, provide owner info for life estate holder and spouse.

•For a trust, provide owner information for qualifying beneficiary/trustee and submit copy of entire Trust Agreement

•If the property is a cooperative, please provide a copy of the stock certificate

•If the property was willed to an owner, please submit a copy of last will and testament, probate or court order.

•For owner receiving medical care in a health care facility, submit documentation from health care facility.

For proof of clergy status: • Verification letter from the house of worship employer on official letterhead. AND COPIES of one of the following, if applicable:

•Death certificate, if you are an

•Physician letter documenting illness or impairment, if the clergy member is unable to perform work for his/her denomination due to illness or impairment.

•Proof of age, if the clergy member is retired and over 70 years of age.

•If the property was willed to an owner, please submit a COPY of last will and testament, probate or court order.

If you are a clery member engaged in secular employment, indicate the time devoted to: |

|

____________secular employment |

_______________________ religious duties |

Owner 1

NAME (FIRST, LAST)

DATE OF BIRTH (mm/dd/yyyy) |

|

|

SOCIAL SECURITY / ITIN NUMBER |

|

|||

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

|

|

APT. |

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

|

|

|

|

|

|

|

TELEPHONE |

( |

) |

– |

CELL PHONE |

( |

) |

– |

NUMBER |

NUMBER |

||||||

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

IS THIS THE PRIMARY RESIDENCE OF OWNER 1? |

||

|

|

|

|

|

|

n Yes |

n No |

|

|

|

|

|

|

|

|

If there are more than two owners, please complete the Additional Owners section on corresponding page

2

Homeowner Tax Benefits INITIAL APPLICATION — 2018/19

Owner 2:

NAME (FIRST, LAST)

DATE OF BIRTH (mm/dd/yyyy) |

|

|

SOCIAL SECURITY / ITIN NUMBER |

|

|

|||

|

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

|

|

APT. |

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

|

|

|

|

|

|

|

|

|

TELEPHONE |

( |

) |

– |

CELL PHONE |

( |

) |

– |

|

NUMBER |

NUMBER |

|

||||||

|

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

IS THIS THE PRIMARY RESIDENCE OF OWNER 2? |

|

||

|

|

|

|

|

|

n Yes |

n No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ARE OWNERS 1 AND 2 |

n Yes |

n No |

|

|

|

|

|

|

MARRIED TO EACH OTHER? |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

The Federal Privacy Act of 1974, as amended, requires agencies requesting Social Security Numbers to inform individuals from whom they seek this information as to whether compliance with the request is voluntary or mandatory, why the request is being made and how the information will be used. The disclosure of Social Security Numbers for applicants and

3. ADDITIONAL PROPERTIES OWNED (IF ANY)

Complete the following for each additional property.

If the property is in NYC, please provide the Borough/Block/Lot Number.

Additional property 1:

BOROUGH |

BLOCK |

LOT |

|

OR |

|||

|

|

|

|

|

|

|

|

|

|

|

|

OWNER(S) NAME

PARCEL ID

STREET ADDRESS |

|

|

|

|

APT |

|

|

|

|

|

|

|

|

CITY |

|

|

STATE |

|

ZIP |

|

|

|

|

|

|

|

|

EXEMPTIONS RECEIVED |

|

|

|

|

|

|

n Basic STAR/Enhanced STAR |

n Senior |

n Disabled n Veterans |

n Other: |

|||

|

|

|

|

|

|

|

Was the property recently sold? |

|

|

|

nYes |

nNo |

|

If yes, provide sale date (mm/dd/yyyy) _______________________________ |

||||||

CLERGY ONLY:

If this property receives a Clergy Exemption,

indicate the amount of clergy exemption received _______________________________$

3 |

Homeowner Tax Benefits INITIAL APPLICATION — 2018/19

3. ADDITIONAL PROPERTIES OWNED (IF ANY) (CONTINUED)

Additional property 2:

BOROUGH |

BLOCK |

LOT |

|

|

|

OWNER(S) NAME

OR

PARCEL ID

|

STREET ADDRESS |

|

|

|

|

|

APT |

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

STATE |

|

ZIP |

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS RECEIVED |

|

|

|

|

|

|

|

|

n Basic STAR/Enhanced STAR |

n Senior |

n Disabled n Veterans n Other: |

|||||

|

|

|

|

|

|

|

|

|

|

Was the property recently sold? |

|

|

|

|

|

nNo |

|

|

If yes, provide sale date (mm/dd/yyyy) _______________________________ nYes |

|||||||

|

|

|

|

|

|

|

|

|

|

CLERGY ONLY: |

|

|

|

|

|

|

|

|

If this property receives a Clergy Exemption, |

|

|

|

|

|

||

|

indicate the amount of clergy exemption received _______________________________$ |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

4. CERTIFICATION |

|

|

|

|

|

|

|

|

Please read carefully and sign the certification below. Your application is not complete if you do not sign. |

|||||||

|

I certify that all statements made on this application are true and correct to the best of my knowledge and that I have |

|||||||

|

made no willful false statements of material fact. I understand that this information is subject to audit and should the |

|||||||

|

Department of Finance determine that I made false statements, I may lose my future exemptions and be responsible |

|||||||

|

for all applicable taxes due, accrued interest, and the maximum penalty allowable by law. |

|||||||

|

All owners must sign and date this application, regardless of where they reside. |

|||||||

|

|

|

|

|

|

|

|

|

|

PRINT NAME OF OWNER 1 |

|

SIGNATURE OF OWNER 1 |

|

DATE OF APPLICATION |

|||

|

|

|

|

|

|

|

|

|

|

PRINT NAME OF OWNER 2 |

|

SIGNATURE OF OWNER 2 |

|

DATE OF APPLICATION |

|||

|

|

|

|

|

|

|

|

|

|

PRINT NAME OF OWNER 3 |

|

SIGNATURE OF OWNER 3 |

|

DATE OF APPLICATION |

|||

|

|

|

|

|

|

|

|

|

|

PRINT NAME OF OWNER 4 |

|

SIGNATURE OF OWNER 4 |

|

DATE OF APPLICATION |

|||

|

|

|

|

|

|

|

|

|

If due to a disability you need an accommodation in order to apply for and receive a service, or to participate in a program offered by the Department of Finance, please contact the Disability Service Facilitator at nyc.gov/contactdofeeo or by calling 311.

4 |

Homeowner Tax Benefits INITIAL APPLICATION — 2018/19

6. ADDITIONAL OWNER(S) (CONTINUED FROM SECTION 2) |

|

|

|

||||

Owner 3: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME (FIRST, LAST) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

DATE OF BIRTH (mm/dd/yyyy) |

|

|

SOCIAL SECURITY / ITIN NUMBER |

|

|||

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

|

|

APT. |

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

|

|

|

|

|

|

|

TELEPHONE |

( |

) |

– |

CELL PHONE |

( |

) |

– |

NUMBER |

NUMBER |

||||||

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

IS THIS THE PRIMARY RESIDENCE OF OWNER 3? |

||

|

|

|

|

|

|

n Yes |

n No |

|

|

|

|

|

|

||

RELATIONSHIP TO OWNERS 1 AND 2 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Owner 4: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME (FIRST, LAST) |

|

|

|

|

|

|

|

|

|

|

|

|

|||

DATE OF BIRTH (mm/dd/yyyy) |

|

|

SOCIAL SECURITY / ITIN NUMBER |

|

|||

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

|

|

APT. |

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

|

|

|

|

|

|

|

TELEPHONE |

( |

) |

– |

CELL PHONE |

( |

) |

– |

NUMBER |

NUMBER |

||||||

|

|

|

|

|

|

||

EMAIL ADDRESS |

|

|

|

|

IS THIS THE PRIMARY RESIDENCE OF OWNER 4? |

||

|

|

|

|

|

|

n Yes |

n No |

|

|

|

|

|

|

||

RELATIONSHIP TO OWNERS 1 AND 2 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Did you... |

|

|

|

|

|

|

|

nCheck over the application to make sure all questions have been answered?

nInclude copies of all required documentation?

nSign and date the application?

nKeep a copy of the completed application for your records?

If you have any questions, please contact us at us at nyc.gov/contactpropexemptions, or call 311. Application and all required documentation must be postmarked by March 15, 2018. BY MAIL:

New York City Department of Finance

P.O. Box 311

Maplewood, NJ

When your application is received, the Department of Finance will send you an acknowledgment as a receipt.

5 |

Document Specifics

| Fact Name | Description | Governing Law(s) |

|---|---|---|

| Eligibility Criteria for Veterans Exemption | Must be a veteran, unbetrothed surviving spouse of a veteran, or parent of a deceased soldier. The veteran should have been honorably discharged and served during specified conflict periods. | New York State Property Tax Laws |

| Non-Eligibility for Certain Property Types | Properties controlled by Mitchell-Lama, Redevelopment Company, Limited-Profit Housing Company, Housing Development Fund Company, or Limited Dividend Housing Company are not eligible for the Veteran Homeowners Exemption. | New York State Property Tax Laws |

| Eligibility for Clergy Exemption | Applies to active clergy members, retired clergy members over 70, unmarried surviving spouses of a clergy, or clergy unable to work due to illness or impairment. Co-op properties are excluded. | New York State Property Tax Laws |

| Application Deadline | All applications and required documents must be postmarked by March 15, 2018, for benefits to start on July 1st. | New York State Property Tax Laws |

| Primary Residence Requirement | Your primary residence is your main living place. You can only have one, but may own multiple properties. Supporting documents required for absences due to medical reasons. | New York State Property Tax Laws |

| Owner Information | All owners and their spouses must complete the section. Foreign nationals should provide their ITIN. | Federal and New York State Tax Laws |

| Transfer of Veterans Exemption | If previously received, you can transfer the exemption to a new property within New York State, subject to conditions. | New York State Property Tax Laws |

| Additional Property Requirements | For owners of additional properties outside NYC not receiving benefits, a letter from the local assessor’s office is needed. | New York State Property Tax Laws |

| Proof of Status Requirements | Veterans and clergy need to provide specific documents (e.g., DD214 for veterans, verification from church for clergy) to prove eligibility. | Applicable Federal and New York State Laws |

Guide to Writing Tax Benefits Application

Filling out the Tax Benefits Application form is a crucial step for homeowners looking to claim their rightful exemptions. This guide provides a straightforward approach to ensure the application is completed accurately and submitted on time. It is essential to gather all pertinent information and related documents before starting the process to avoid any unnecessary delays. The following steps are designed to make this process as smooth as possible.

- Begin by reviewing the eligibility criteria for the Veterans Exemption and the Clergy Exemption to determine if you qualify for either program.

- Mark the appropriate response to each eligibility question based on your circumstances.

- For Property Information, provide the complete address of the property, including the borough, block, and lot (BBL) number. If your property is a co-op, include the number of cooperative shares owned.

- Enter the type of property (e.g., Condominium unit, 1–3 family dwelling, Cooperative, 4+ family dwelling).

- Indicate the percentage of space used for primary residence if the dwelling has four or more units.

- Provide the date you purchased the property or co-op shares.

- Complete all required sections for owner information. If applicable, include your Individual Taxpayer Identification Number (ITIN).

- If you're applying for the Veterans Exemption and your property has a life estate or is held in a trust, ensure only the eligible individual is applying.

- For additional property information, disclose if you or your spouse own any other property outside NYC and provide evidence that no benefits are being received on that property.

- Prepare and include all required documentation, such as a copy of the DD214 or its equivalent for the Veterans Exemption and verification letter from the house of worship employer for the Clergy Exemption. Also, include other applicable documents like marriage certificates, death certificates, or proof of age.

- Ensure all homeowners sign the Certification section of the application.

- Mail the completed application along with COPIES of all required documentation to the New York City Department of Finance, P.O. Box 311, Maplewood, NJ 07040-0311. The application must be postmarked by March 15, 2018.

- Keep a copy of your application and all documentation for your records.

After submitting your application, you will receive an acknowledgment letter from the Department of Finance. This letter signifies that your application has been received and is being processed. It is crucial to provide all necessary information and documentation to avoid delays. If you need help or have questions during the application process, you can reach out for assistance through the contact information provided on the application form. Proper completion and timely submission of your application are key to taking advantage of tax benefits that you may be eligible for.

Understanding Tax Benefits Application

Who is eligible for the Veterans Exemption on homeowner tax benefits?

To be eligible for the Veterans Exemption, the property must be the primary residence of either a veteran, an unmarried surviving spouse of a veteran, or a parent of a soldier killed in action (Gold Star Parent). Additionally, the veteran must have been honorably discharged and served during specified conflict periods such as World War I, World War II, the Korean Conflict, the Vietnam War, or the Persian Gulf Conflict. Properties controlled by certain housing developments like Mitchell-Lama or owned by businesses are not eligible.

What documents are needed to prove veteran status for the exemption application?

Required documentation includes a copy of the veteran's DD214 or equivalent, separation papers, and depending on the applicant's relation to the veteran, possibly a marriage certificate, death certificate, or Veterans Administration award letter with a service connected disability rating. It's essential to submit these documents along with the application to ensure eligibility.

Can the Veterans Exemption be transferred to another property?

Yes, the Veterans Exemption can be transferred to a new property provided the previous residence was granted the exemption, both residences are located in New York State, and the application is received within 30 days of purchasing the new property. To qualify for the tax year, the application must be postmarked by March 15th. If approved, the exemption will be prorated.

What is the application submission deadline for homeowner tax benefits?

The application and all required documents must be postmarked by March 15, 2018, for benefits to commence on July 1st. If March 15 falls on a weekend or holiday, the deadline extends to the next business day.

How do I know if I am eligible for the Clergy Exemption?

To be eligible for the Clergy Exemption, your primary residence must be in New York State, and you must be an active clergy member primarily engaged in ministerial work, a retired clergy member over 70, an unmarried surviving spouse of a clergy member, or a clergy member unable to perform work due to illness or impairment. Cooperative properties are not eligible for this exemption.

What documentation is required for the Clergy Exemption?

Applicants for the Clergy Exemption must provide a verification letter from the house of worship employer on official letterhead, alongside other applicable documents such as a death certificate for an unmarried surviving spouse or a physician's letter documenting illness or impairment. Proof of age is required for retired clergy members over 70.

Where do I send my Homeowner Tax Benefit Application?

The original application, along with copies of all required documentation, should be sent to the NYC Department of Finance at P.O. Box 311, Maplewood, NJ 07040-0311. It's crucial to keep a copy of your application for your records.

What types of properties are eligible for these homeowner tax benefits?

Eligible properties include condominium units, 1–3 family dwellings, cooperatives, and 4+ family dwellings with a specified percentage used for primary residence. Properties such as cooperative units under specific housing developments and those owned by businesses are not eligible for the Veterans Exemption.

How do I obtain the DD214 form or equivalent for the application?

The DD214 form or its equivalent can be obtained from the National Personnel Records Center in St. Louis, Missouri, either by contacting them directly or visiting their website. This form is a crucial piece of documentation for verifying veteran status and is required for the application.

Can I apply for both the Veterans and Clergy Exemptions?

If you meet the eligibility criteria for both exemptions, you may apply for both the Veterans and Clergy Exemptions. Make sure to check all applicable boxes on the application form and provide the necessary documentation for each exemption. Eligibility will be determined based on the provided information and documentation.

Common mistakes

When filling out the Tax Benefits Application form, individuals often make mistakes that can impact their eligibility or delay the processing of their application. Here are five common errors:

Not checking the eligibility criteria carefully: It's essential to read through the eligibility requirements for each tax benefit program. For instance, properties controlled by certain housing developments are not eligible for the Veteran Homeowners Exemption.

Incomplete property information: Applicants must provide complete and accurate property information, including the borough, block, and lot numbers. This information is crucial for the Department of Finance to process the application.

Failing to provide required documentation: Each exemption program has specific documentation requirements, such as proof of veteran status or proof of clergy status. Missing or incomplete documents can result in application delays.

Not indicating the primary residence correctly: The form requires applicants to confirm if the property is their primary residence. Incorrect information can make a significant difference in eligibility, especially for veterans applying for exemptions that are applicable only to their primary residence.

Waiting until the last minute to submit: The application and all required documentation must be postmarked by the specified deadline. Late submissions may not be accepted, delaying the benefits or making the applicant ineligible for that tax year.

Avoiding these mistakes can help ensure that the application process goes smoothly and that applicants receive the tax benefits for which they are eligible.

Documents used along the form

Filling out the Tax Benefits Application form for the tax year 2018/19 requires attention to detail and making sure to include all necessary paperwork. Apart from this application, several other forms and documents are often required to ensure that one's application is complete and processed without delay. Understanding these additional requirements can help applicants prepare their submissions thoroughly.

- Proof of Veteran Status: This includes copies of the DD214 or its equivalent and separation papers. These documents are crucial for verifying military service and are a standard requirement for veterans seeking tax advantages.

- Marriage Certificate: If applying for exemptions based on a spouse’s military service, a copy of the marriage certificate is necessary to establish the relationship between the applicant and the veteran.

- Death Certificate: For unmarried surviving spouses or Gold Star parents applying for benefits, providing a death certificate is required to prove their eligibility based on their deceased spouse's or child’s service.

- Veterans Administration Award Letter: Veterans with a service-connected disability must submit a copy of their VA award letter showing their disability rating to qualify for certain tax exemptions.

- Proof of Clergy Status: A verification letter from the house of worship on official letterhead is needed for clergy members to prove their status and primary occupation for clergy tax exemptions.

- Physician Letter Documenting Illness or Impairment: Clergy members unable to perform their duties due to illness or impairment must provide a letter from their physician detailing their condition.

- Proof of Age: Retired clergy members over the age of 70 applying for exemptions should include documentation, such as a birth certificate, to verify their age.

- Trust Agreement Copy: For properties held in a trust, applicants must submit a copy of the entire trust agreement to show the qualifying beneficiary/trustee who is applying for the tax benefit.

- Documentation from Health Care Facility: Owners receiving medical care in a health facility need to provide documentation from the facility if the absence from their primary residence is due to medical reasons.

Compiling these documents in preparation for submitting the Tax Benefits Application can be a daunting task, but it is essential for securing the tax benefits one may be eligible for. Always ensure that documents are clear, legible, and relevant to the application to facilitate smooth processing by the Department of Finance. Being organized and thorough in gathering and submitting these documents can lead to successful approval of tax benefits.

Similar forms

The Tax Benefits Application form closely resembles the Homestead Exemption application used in various states. Both forms are designed for homeowners looking to reduce their property taxes by proving their property as a primary residence. The Homestead Exemption, like the Veterans Exemption and Clergy Exemption on the Tax Benefits Application, requires homeowners to provide specific documentation, such as proof of residence and ownership details. Both applications also have strict deadlines for submission to qualify for tax reduction benefits in a particular tax year.

Another document similar to the Tax Benefits Application form is the Property Tax Deferral application. This form is intended for homeowners who wish to postpone payment of property taxes due to financial hardship or age. Like the Tax Benefits Application, it involves submitting proof of eligibility, which may include age verification, income level documentation, and evidence of the property as the homeowner's primary residence. Both forms require detailed property information and owner identification to process the application.

The application for a Mortgage Credit Certificate (MCC) also shares similarities with the Tax Benefits Application form. The MCC program provides qualifying homeowners a tax credit for a portion of their mortgage interest, aiming to make homeownership more affordable. Applicants must provide detailed personal and property information, similar to what's required for tax benefits applications, including property purchase details and proof of eligibility, such as income documentation.

Similar to the Tax Benefits Application form, the application for Income-Based Property Tax Relief programs for seniors or low-income families requires applicants to prove their eligibility through detailed personal, property, and financial information. These programs often ask for documentation of income, property ownership, and residency status to ensure applicants meet specific thresholds for tax relief or exemptions aimed at easing the tax burden on vulnerable populations.

Lastly, the application process for Energy Efficient Property Tax Credits shares similarities with the Tax Benefits Application form in that homeowners must provide property details and evidence of qualifying energy-efficient improvements. Both application processes aim to offer financial benefits to homeowners, though for different reasons: one for general tax relief and the other for incentivizing energy efficiency improvements. Required documentation may include proof of installation and associated costs, alongside standard property and homeowner identification details.

Dos and Don'ts

When you're filling out the Tax Benefits Application form, there are key dos and don'ts to ensure your application is complete and accurate. Following these guidelines can help streamline the process and increase the likelihood of receiving your benefits without unnecessary delays.

- Do read all the instructions carefully before you start filling out the form. This helps avoid mistakes that could delay your application.

- Do verify your eligibility for the specific tax benefit you are applying for, such as the Veterans Exemption or Clergy Exemption.

- Do gather all required documentation before you begin the application. This includes proof of veteran status, like DD214 or separation papers, and for clergy members, verification letters from their house of worship.

- Do ensure all homeowner information is accurate, including names, social security numbers, and contact details. Double-check for correctness.

- Do provide complete property information, including borough, block, and lot (BBL) numbers, which can be found on the Department of Finance website or your deed/property tax bill.

- Do note the application deadline — March 15, 2018, for tax benefits to begin on July 1. If the deadline falls on a weekend or holiday, it will be extended to the next business day.

- Don't submit the application without the required documents. Incomplete applications can result in delays or denial of the exemption.

- Don't send original documents unless specifically requested. Always keep copies for your records.

- Don't forget to sign the certification section of the application. Unsigned applications are incomplete.

- Don't overlook the importance of checking with your managing agent (if applicable) to confirm details about your cooperative's control by certain housing developments, which may affect eligibility.

Misconceptions

Understanding the particulars of Tax Benefits Application forms can sometimes be confusing. Here are six common misconceptions explained to help clarify the process:

- Tax benefits are only for individuals, not businesses: This is a common misunderstanding. While certain exemptions, specifically the Homeowner Tax Benefits, are not available to properties owned by businesses, there are numerous tax incentives and benefits designed to support businesses. It's crucial to differentiate between what is available for individual homeowners and what is available for businesses.

- Cooperative apartments are always eligible for tax exemptions: This is not true. If a cooperative property is controlled by specific housing developments such as Mitchell-Lama, Redevelopment Company, or others mentioned in the form, it is ineligible for the Veteran Homeowners Exemption. Cooperative owners must confirm with their managing agent about the property's eligibility.

- Any veteran or their family members are eligible for the Veterans Exemption: Eligibility for this exemption is subject to specific conditions. The veteran must have been honorably discharged and served during recognized periods of war or conflict. Moreover, the property must be the primary residence of the veteran, their unmarried surviving spouse, or the parent of a soldier killed in action.

- All clergy members automatically qualify for the Clergy Exemption: Clergy members also have specific eligibility criteria for tax exemptions. They must be active and primarily engaged in ministerial work, retired clergy members over the age of 70, or unable to perform their duties due to illness or impairment. Additionally, the primary residence must be in New York State and the property cannot be a cooperative for the Clergy Exemption to apply.

- The submission deadline is flexible: The Deadline of March 15, 2018, for the Homeowner Tax Benefit Application and required documents to be postmarked was firm. Missing this deadline could delay or disqualify applicants from receiving benefits starting July 1. It's a common mistake to assume leniency or extensions on such deadlines without official notice.

- Eligibility is determined based solely on application questions: While the application form’s questions are crucial for initial screening, eligibility for tax benefits often requires thorough documentation and sometimes additional verification. For instance, proof of veteran status via DD214 or separation papers and other applicable documents such as marriage certificates or death certificates for spouses or Gold Star parents are required for the Veterans Exemption. Similarly, clergy status must be verified through official documents and letters.

Understanding these misconceptions helps in correctly applying for tax benefits and maximizes the chances of receiving any exemptions for which an individual or family may be eligible.

Key takeaways

Filing for homeowner tax benefits can be a complex process, involving numerous factors and eligibility criteria. Here are six key takeaways from the Tax Benefits Application form for the 2018/19 tax year that can help homeowners navigate through this process with more clarity:

- Check your eligibility upfront: Before investing your time in filling out the application, it's essential to verify your eligibility. For instance, veterans seeking the Veterans Exemption must confirm that their property is not controlled by specific housing developments and that they meet criteria including honorable discharge and service during designated conflict periods. Similarly, applicants for the Clergy Exemption must ensure their primary residence is in New York State and meet other specific criteria.

- Be mindful of the deadline: The application and all required documentation must be postmarked by March 15, 2018. Missing this deadline can delay or disqualify your application for tax benefits. If the deadline falls on a weekend or holiday, it will be extended to the next business day.

- Property details matter: Furnishing accurate and complete property information is vital. This includes the property's full address, borough, block and lot (BBL) number, and the date of purchase. For properties within cooperative housing, further details may be required.

- Document ownership properly: All sections of the owner information must be filled out comprehensively. For properties owned by businesses, in trust, or with a life estate, there are specific requirements that must be met to qualify for tax benefits.

- Consider all relevant tax benefits: If transferring a Veterans Exemption from one property to another, ensure the application is received within the designated timeframe to qualify for benefits in the following tax year. For properties with multiple units, specifying the percentage used as the primary residence is crucial.

- Submit required documentation: In addition to the application, copies of necessary documents such as proof of veteran or clergy status, DD214 or separation papers, marriage certificates for spouses applying based on the military service of a veteran, or death certificates for unmarried surviving spouses or Gold Star parents must be included. The process also requires documentation for properties held in a trust or life estate, among other details.

Adhering to these key pointers can streamline the application process and increase the chances of obtaining valuable tax benefits. Always keep a copy of your application and supporting documents for your records, and consult with a tax professional or legal advisor if you have questions or need guidance through the process.

Popular PDF Documents

IRS 8867 - Through the information collected on the IRS 8867, tax authorities can more easily detect discrepancies and irregularities in tax credit claims.

Non Resident Alien Tax Withholding - The notice is an educational tool, enhancing the financial literacy of non-citizens about U.S. tax requirements.

How to Fill Out W4 Married Filing Jointly No Dependents - The W-4 form's purpose is to help employees manage their tax liability and align their withholding with their tax obligation.