Get Oklahoma Minimum Franchise Tax Form

In the realm of running a business in Oklahoma, one notable obligation is the filing of the Oklahoma Minimum Franchise Tax form, specifically Form 215, designed for delinquent filers. This form caters to corporations that find themselves behind on their franchise tax obligations, providing a structured method for recalculating and submitting overdue taxes. The form outlines eligibility criteria, emphasizing a tax liability range from the minimum $10 to a ceiling of $20,000, and includes a comprehensive worksheet to assist businesses in determining their precise tax obligation based on their assets and operations within Oklahoma. Additionally, it addresses the necessary steps for correcting any outdated or incorrect preprinted company information and guides the filer through completing the subsequent sections that capture the company's financial and corporate details. Of critical importance, the form specifies various fees and penalties applicable to delinquent filings, including late penalties and reinstatement fees, aimed at encouraging compliance. Furthermore, special notes and instructions ensure the accurate and timely submission of the form and accompanying documentation, such as schedule of officers and payment, to avoid further financial penalties. This setup underscores the tax authorities' efforts to streamline the process for businesses to rectify their franchise tax standing while emphasizing the importance of adhering to the state's regulatory and financial requirements.

Oklahoma Minimum Franchise Tax Example

OKLAHOMA TAX COMMISSION

OKLAHOMA MINIMUM/MAXIMUM FRANCHISE TAX RETURN

FORM 215

Delinquent Filers Only

This version of Form 215 is for delinquent filers only.

Not for use for current reports.

|

FRX |

0600103 |

|

|

|

|

|

OKLAHOMA MINIMUM/MAXIMUM |

|

|

|

|||

|

|

Form 215 |

|

|

|

|

Revised |

|

|

|

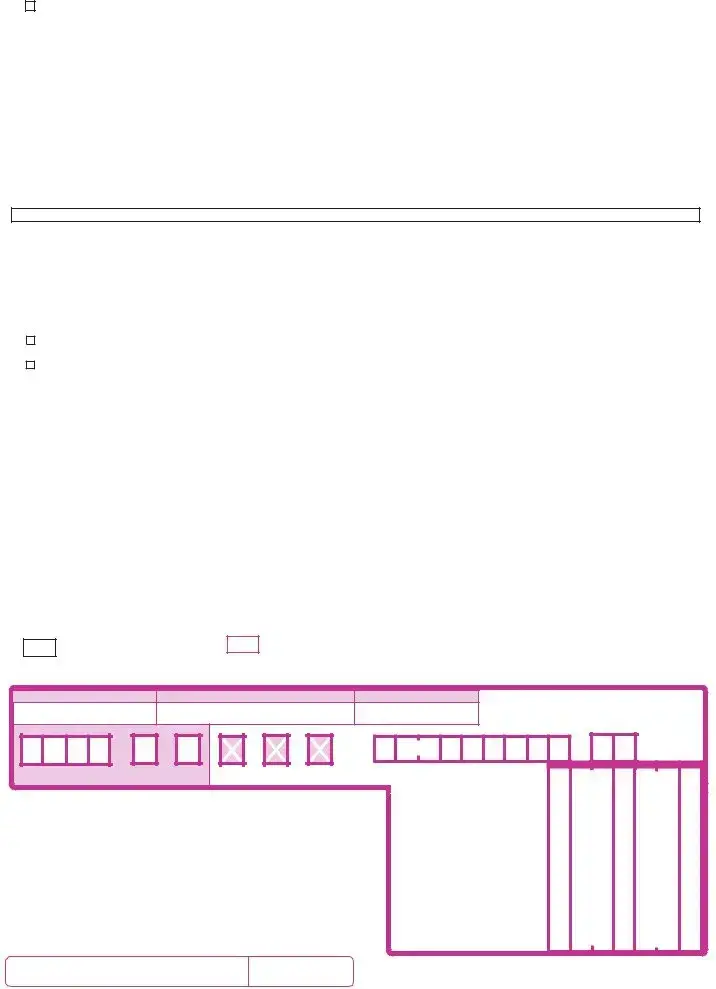

A. TAXPAYER FEIN |

B. REPORTING PERIOD |

C. DUE DATE |

|

|

|

|

|

|

|

|

|

|

|

FRANCHISE TAX RETURN

1.You qualify to file this return if your tax liability is the minimum of $10.00 or the maximum of $20,000. Use the worksheet to determine your tax liability. If you do not qualify to file this return, call the OTC at

(405)

2.If the preprinted name and address on this form is incorrect check Item E and make corrections on the back of the return.

3.Follow the instructions on the back of this form for the completion of lines 1 through 6 on the detachable report below.

4.Return the detachable return below and schedule of officers with your payment in the enclosed return envelope before the due date to avoid assessment of interest and penalty.

TAX WORKSHEET

The basis for computing your tax is the balance sheet as shown by your books |

(A) Everywhere |

(B) Oklahoma Only |

||

of account at the close of your most recent income tax accounting year. |

||||

|

|

|||

|

|

(Do not use if all property is in OK) |

|

|

1. |

Enter total company assets |

________________________________ |

_______________________________ |

|

2. |

Enter business done |

________________________________ |

_______________________________ |

|

3. |

Total assets and business done (Line 1 plus Line 2) |

________________________________ |

_______________________________ |

|

4. |

Percentage of capital employed in Oklahoma. Select the option |

________________________________ |

|

|

|

you will use to determine the apportionment of Oklahoma Assets |

|

|

|

|

Option 1: Percent of Oklahoma Assets and business done to total assets and |

|

|

|

|

business done. (Line 3B divided by line 3A) Round to 4 decimal points. |

|

|

|

|

Option 2: Percent of Oklahoma Assets to total net assets |

|

|

|

|

(Line 1B divided by line 1A) Round to 4 decimal points. |

|

|

|

5. |

Enter total current company liabilities; i.e. accounts payable, short term debt, etc. |

_________________________________ |

________________________________ |

|

6. |

Calculate the capital employed in Oklahoma |

_________________________________ |

|

|

|

|

|

||

|

OR |

|

|

|

|

|

_________________________________ |

||

7. |

Calculate your franchise tax. The tax rate is $1.25 per $1,000.00, or portion thereof, |

_________________________________ |

_________________________________ |

|

|

of capital employed in Oklahoma. Use Line 6A if company employs capital in states |

|

|

|

|

other than Oklahoma. Use 6B if all company capital is in Oklahoma. |

|

|

|

If your capital on Line 6(A) or 6(B) above is less than $8,000, enter $10 in the box for line 1 below. If your capital on Line 6(A) or 6(B) above is more than $16,000,000 enter $20,000 in the box for Line 1 below. If your capital is between $8,000 and $16,000,000 you cannot use this form. Please call (405)

|

Special Note: To insure that your report will be properly |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

0 |

X |

|

||||

|

processed, please print all figures within boxes as shown. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

• Write only |

|

|||||||||||

• Do not fold, staple or paper clip |

PLEASE DETACH HERE AND RETURN REPORT BELOW |

|

in white areas |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FRX

0600103 I.

000

OKLAHOMA MINIMUM/MAXIMUM FRANCHISE TAX RETURN |

|

|

|

|

A. Taxpayer FEIN |

B. Reporting Period |

C. Due Date |

|

|

|

|

G. TAXPAYER FEIN |

H. TAX PERIOD |

|

M M D D |

|

|

Y Y |

|

|

|

|

CENTS |

|

|

P.T. D. FOREIGN E. CHANGE |

F. ESTIMATED |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

CORP. |

RETURN |

1. Tax |

= |

|

|

|

0 |

0 |

|

||

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

(Minimum $10 or Maximum $20,000) |

+ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Registered Agent Fee |

|

|

|

0 |

0 |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

(see instructions) |

+ |

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

4. |

Penalty |

+ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

5. |

Reinstatement Fee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

0 |

|

||

Address |

|

|

|

|

|

+ |

|

|

|

|

|||||

|

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

6. Total Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

State |

|

ZIP |

|

|

= |

|

|

|

|

|

|

|||

|

|

|

|

(Min. $10) |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I declare that the information contained in this document and any attachments is true and correct to the best of my knowledge and belief.

Sign Here

Date

INSTRUCTIONS FOR COMPLETING THE MINIMUM/MAXIMUM FRANCHISE TAX RETURN

GENERAL INSTRUCTIONS

Please write only in the white areas. This return

SPECIFIC LINE INSTRUCTIONS • CONTINUED

WHEN TO FILE

must be legible and suitable for microfilming Please |

Line 4 • Penalty |

The tax is due on July 1 The report and tax will be |

|||||||||||

form your entries as shown in the character |

It this return is postmarked after the due date, the |

delinquent if not paid on or before August 31, and |

|||||||||||

formation guide with a #2 pencil or black ink pen. |

tax is subject to a penalty of 10%. Multiply the |

is delinquent on September 1 of each year, or if |

|||||||||||

|

|

|

|

amount on Line 1 by 0.10 to determine the |

you elected to change your filing period to be the |

||||||||

|

SPECIFIC ITEM INSTRUCTIONS |

|

|

penalty. Enter the amount of penalty due. |

same as your corporate income tax, the report and |

||||||||

|

|

|

|

|

|

|

tax, will be delinquent if not paid by the fifteenth |

||||||

• Item D |

Line 5 • Reinstatement Fee |

(15) day of the third month following the close of |

|||||||||||

Place an 'X' in the box if you are a foreign |

the corporate income tax year. Penalty and |

||||||||||||

If the corporation has been suspended, it must be |

|||||||||||||

corporation, not incorporated in Oklahoma. |

interest is charged after the delinquency date. A |

||||||||||||

reinstated. Enter $15 00 on Line 5. |

|||||||||||||

|

|

|

|

||||||||||

|

|

|

|

corporation may be suspended if the tax is not |

|||||||||

• Item E |

|

|

|

||||||||||

|

|

|

paid and/or officer information is not provided. A |

||||||||||

Place an `X" in the box if any preprinted information is |

Line 6 • Total Due |

||||||||||||

reinstatement fee of $15.00 is required to return |

|||||||||||||

incorrect. Make corrections in the space provided |

Add the amounts of lines 1 through 5 and enter |

||||||||||||

the corporation to good standing after it has been |

|||||||||||||

below. |

|||||||||||||

the total on line 6. |

|||||||||||||

|

|

|

|

suspended. |

|||||||||

|

|

|

|

|

|

|

|||||||

• Item F |

Schedule A • Officer Information |

|

|

|

|

|

|

||||||

Place an X` in the box if you have not completed a |

If you file an extension to file your corporate |

||||||||||||

year end balance sheet You must file an estimated |

Enter the reporting period indicated in Item B. |

||||||||||||

income tax return, a copy of your request for |

|||||||||||||

return. |

If any preprinted officer information (Schedule A) |

||||||||||||

an extension must accompany your estimated |

|||||||||||||

|

|

|

|

||||||||||

|

|

|

|

is incorrect, please make the necessary changes |

|||||||||

• Item G |

franchise tax return. |

||||||||||||

on Schedule A and mail with your tax return and |

|||||||||||||

If your FEIN is not preprinted, please enter your |

|

|

|

|

|

|

|||||||

FEIN. |

payment. Be sure to update the corporate |

|

|

|

PAYMENT INFORMATION |

|

|||||||

• Item H |

officers' name, address and social security |

|

|

|

|

|

|

||||||

number. Failure to provide this information could |

To assist us in processing your return accurately |

||||||||||||

Enter the tax year for which you are filing a return. |

|||||||||||||

result in the corporation being suspended. |

|||||||||||||

and assure proper credit to your account, please |

|||||||||||||

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

send a separate check with each report submitted. |

||||||

|

SPECIFIC LINE INSTRUCTIONS |

|

|

WHO MUST FILE |

|

Please put your FEIN on your check. |

|||||||

|

|

|

|

|

|

||||||||

Line 1 • Tax |

|

|

|

||||||||||

Every corporation doing business in the state of |

|

|

|

|

|

|

|||||||

|

WHO TO CONTACT FOR ASSISTANCE |

|

|||||||||||

Enter the amount computed from your |

|

|

|||||||||||

Oklahoma must file an annual franchise tax return |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

||||||||

worksheet. The amount must be either the |

|

|

|

|

|

|

|||||||

and pay the franchise tax by July 1 of each year. |

For franchise tax assistance, call the Oklahoma |

||||||||||||

minimum $10.00 or maximum $20,000.00 tax. |

|||||||||||||

The report and tax will be delinquent if not paid |

|||||||||||||

Tax Commission at (405) |

|||||||||||||

|

|

|

|

||||||||||

|

|

|

|

on or before August 31, or if you elected to |

|||||||||

Line 2 • Registered Agent Fee |

|

|

|

|

|

|

|||||||

change your filing period to be the same as your |

Mandatory inclusion of Social Security and/or |

||||||||||||

If you are incorporated in a state other than |

|||||||||||||

corporate income tax, the report and tax will be |

|||||||||||||

Federal Employer's Identification numbers is |

|||||||||||||

Oklahoma, the Secretary of State of Oklahoma |

|||||||||||||

delinquent if not paid by the fifteenth (15) day of |

|||||||||||||

required on forms filed with the Oklahoma Tax |

|||||||||||||

charges an annual registered agent fee of $100.00. |

|||||||||||||

the third month following the close of the |

|||||||||||||

Commission pursuant to Title 68 of the Oklahoma |

|||||||||||||

If this applies to your corporation, enter $100.00 on |

|||||||||||||

corporate income tax year. The report and tax are |

|||||||||||||

Statutes and regulations thereunder, for |

|||||||||||||

line 2. |

|||||||||||||

due annually until the corporation ceases under |

|||||||||||||

identification purposes, and are deemed to be part |

|||||||||||||

|

|

|

|

||||||||||

|

|

|

|

the provisions of the Oklahoma General |

|||||||||

Line 3 • Interest |

of the confidential files and records of the |

||||||||||||

Corporation Act. If you wish to make an election |

|||||||||||||

Oklahoma Tax Commission. |

|||||||||||||

If this return is postmarked after the due date, the |

|||||||||||||

to change your filing frequency for your next |

|||||||||||||

|

|

|

|

|

|

||||||||

tax is subject to 1.25% interest per month from the |

|

|

|

|

|

|

|||||||

reporting period, please complete OTC Form |

|

|

|

|

|

|

|||||||

|

|

|

MAILING INSTRUCTIONS |

|

|

||||||||

due date until it is paid. Multiply the amount on Line |

|

|

|

|

|

||||||||

200F: Request to Change Franchise Tax Filing |

|

|

|

|

|

||||||||

|

|

|

|

|

|

||||||||

I by .0125 for each month the report is late. Enter |

|

|

|

|

|

|

|||||||

Period. You may file this return if your tax |

|

|

|

|

|

|

|||||||

the amount of interest due. |

Please mail your completed return, officer |

||||||||||||

liability is the minimum of $10.00 or the |

|||||||||||||

|

|

|

|

information and payment to |

|||||||||

|

|

|

|

maximum of $20,000.00. If you do not quality to |

|||||||||

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

file this form call the OTC at (405) |

|

|

Oklahoma Tax Commission |

||||||

|

|

|

|

the correct form. |

|

|

|||||||

|

|

|

|

|

|

Franchise Tax |

|||||||

|

|

|

|

|

|

|

|

|

|||||

The Oklahoma Tax Commission is not required to give actual notice of changes in any state tax law. |

|

|

P.O. Box 26930 |

||||||||||

|

|

|

|

|

|

|

|

|

Oklahoma City, OK |

||||

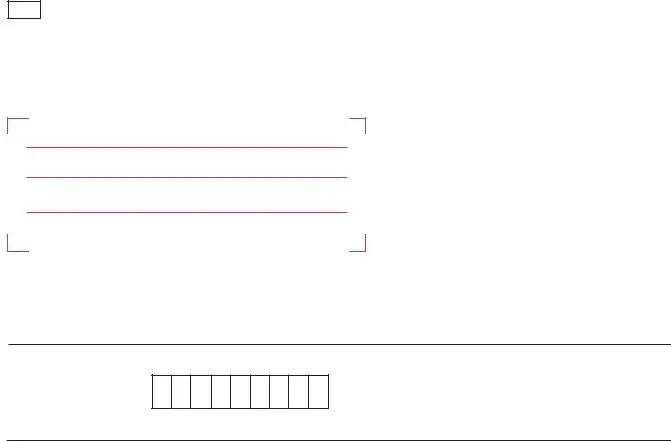

CHANGES IN

If you checked Box E.,indicate the changes only below.

Name _______________________________________________________

Address _____________________________________________________

City ________________________________________________________

State ________________________________________________________

ZIP Code ____________________________________________________

FRX

0600102 000

Name

Address

City |

State |

ZIP |

FEDERAL EMPLOYER’S

IDENTIFICATION NUMBER

SCHEDULE A

CORPORATE OFFICERS FOR THE REPORTING PERIOD OF ______________ ARE AS FOLLOWS:

|

(Date) |

|

|

President |

Social Security Number |

|

|

Home Address (street and number, city, state, ZIP code) |

Home Phone (area code and number) |

|

|

Vice President |

Social Security Number |

|

|

Home Address (street and number, city, state, ZIP code) |

Home Phone (area code and number) |

|

|

Secretary |

Social Security Number |

|

|

Home Address (street and number, city, state, ZIP code) |

Home Phone (area code and number) |

|

|

Treasurer |

Social Security Number |

|

|

Home Address (street and number, city, state, ZIP code) |

Home Phone (area code and number) |

Note: If additional space is needed, please attach a schedule in the same format.

Mandatory inclusion of social security and/or federal identification numbers are required on forms filed with the Oklahoma Tax Commission pursuant to Title 68 of the Oklahoma Statutes and rules thereunder, for identification purposes, and are deemed part of the confidential files and records of the Oklahoma Tax Commission.

Document Specifics

| Fact Name | Description |

|---|---|

| Form Title | Oklahoma Minimum/Maximum Franchise Tax Return Form 215 |

| Purpose | Used by delinquent filers to report and calculate franchise tax liability |

| Tax Liability Range | Minimum of $10.00 to a maximum of $20,000.00 |

| Governing Law | Title 68 of the Oklahoma Statutes |

| Due Date | July 1st Annually, Delinquent post-August 31 or the 15th day of the third month following the close of the corporate income tax year |

| Filing Requirement | Mandatory for all corporations doing business in Oklahoma |

| Penalty and Interest | Penalties for late filings and interest is charged at 1.25% per month after due date |

| Contact Information | Oklahoma Tax Commission, call (405) 521-3160 for assistance |

| Address Changes | Indicate by checking Box E and providing current information |

Guide to Writing Oklahoma Minimum Franchise Tax

Filling out the Oklahoma Minimum Franchise Tax form involves precision and a clear understanding of your business's financial status. This tax form, applicable to delinquent filers, dictates a specific range for the franchise tax: a minimum of $10 and a maximum of $20,000. Completing this form accurately ensures your business remains compliant with Oklahoma's tax regulations.

- Review your business's eligibility: Ensure your tax liability falls within the $10 minimum and $20,000 maximum range.

- If the preprinted information is incorrect, mark Item E and provide the correct details on the back of the return.

- Begin with the Tax Worksheet on the front page to calculate your franchise tax based on your company’s assets and business activity in Oklahoma.

- For "A. TAXPAYER FEIN," input your Federal Employer Identification Number.

- Under "B. REPORTING PERIOD" and "C. DUE DATE," specify the corresponding dates.

- Complete the tax worksheet, including total assets, business done everywhere and in Oklahoma, to determine the percentage of capital employed in the state and calculate your franchise tax liability.

- Enter your calculated tax on Line 1 of the detachable return sheet, ensuring it matches either the minimum or maximum thresholds provided.

- Fill out Line 2 if the Registered Agent Fee applies to your business, typically a $100 fee for out-of-state corporations.

- Calculate and input any interest or penalties owed in Lines 3 and 4, respectively, if your filing is late.

- If applicable, include the Reinstatement Fee on Line 5, necessary for corporations suspended and seeking reinstatement.

- Sum the totals of Lines 1 through 5 on Line 6 for your Total Due.

- Sign and date the form where indicated to certify the accuracy of the information provided.

- For foreign corporations, ensure to mark Item D and fill out the Schedule A with the current officer information.

- If there have been changes to preprinted information, correct this on the lower section of the form specified for changes.

- Mail the completed form, along with payment and any necessary corrections or additional schedules, to the Oklahoma Tax Commission by the due date to avoid further penalties and interest.

It’s vital to remember that compliance with Oklahoma's tax laws, through accurate and timely filing, plays a crucial role in maintaining your business's good standing. If unclear about any step, it’s beneficial to seek clarification or assistance to ensure accurate filing.

Understanding Oklahoma Minimum Franchise Tax

Who needs to file the Oklahoma Minimum Franchise Tax Form (Form 215)?

Any corporation operating within Oklahoma must file an annual franchise tax return and pay the associated tax. This requirement holds until the corporation formally dissolves under the Oklahoma General Corporation Act's provisions. Specifically, if your corporation's franchise tax liability falls within the minimum of $10.00 or the maximum of $20,000.00, you are required to file this return. If your liability does not fit within these parameters, you need to contact the Oklahoma Tax Commission (OTC) for the appropriate form.

When is the Oklahoma Minimum Franchise Tax due?

The franchise tax is due by July 1 each year. If the tax and the report are not submitted by August 31, they become delinquent. For corporations that align their filing period with their corporate income tax schedule, the due date is the fifteenth day of the third month following the close of their corporate income tax year. Failure to pay on time results in penalties and interest charges starting from September 1.

What are the penalties and interest for late filing?

If the franchise tax return is submitted after the due date, a 10% penalty is applied to the tax amount due. Additionally, interest accrues at a rate of 1.25% per month from the due date until the tax is fully paid. These charges are applied to encourage timely filing and payment.

How is the franchise tax calculated?

The tax calculation is based on the company's total assets and business within Oklahoma as compared to its total overall earnings and assets. You have the option to calculate the proportion of capital employed in Oklahoma either by the percentage of Oklahoma assets and business to total assets and business, or by the percentage of Oklahoma assets to total net assets. The actual tax rate is $1.25 per $1,000 or portion thereof of capital employed in Oklahoma. The minimum tax is $10 for capital less than $8,000, and the maximum tax is $20,000 for capital over $16,000,000.

What information is required for filing?

When filing Form 215, you need to provide the corporation's Federal Employer Identification Number (FEIN), the reporting period, and details on company officers (if applicable). Furthermore, if there have been any changes to preprinted information, such as the corporation’s name or address, these changes must be indicated on the form. All figures should be printed within the boxes provided to ensure the report is processed correctly.

What if my corporation's information has changed?

If there are changes to the corporation's preprinted information, such as address or name changes, you must mark an ‘X’ in the appropriate box on the form and provide the corrected information. It is crucial to keep all information up to date to ensure that the Oklahoma Tax Commission's records are accurate and that your corporation remains in good standing.

Where do I send my completed Oklahoma Minimum Franchise Tax Form?

The completed Form 215, along with any payment due, should be sent to the Oklahoma Tax Commission at P.O. Box 26930, Oklahoma City, OK 73126-0930. To ensure accurate processing and credit to your account, include a separate check for each report and write your FEIN on your check.

Common mistakes

Filling out tax forms can often be confusing, and the Oklahoma Minimum Franchise Tax Form 215 is no exception. Here are seven common mistakes to avoid to ensure the process goes as smoothly as possible:

Forgetting to check if you qualify: This form is intended for those whose tax liability falls at the minimum $10.00 or the maximum $20,000.00. Before diving into the paperwork, confirm if your business falls within these parameters.

Incorrect name and address: Although it sounds simple, not updating the preprinted name and address can lead to your form being processed incorrectly. Ensure any changes in Item E are indicated on the back of the return.

Miscalculating the tax due: The tax calculation involves several steps, starting with determining your company's capital employed in Oklahoma. Using incorrect asset figures or the wrong apportionment option can distort your tax due.

Not including the registered agent fee: If you are incorporated outside of Oklahoma, you must include a $100.00 registered agent fee with your tax. This is a common oversight for out-of-state businesses.

Forgetting about penalties and interest: Late filings incur a penalty plus 1.25% interest per month overdue. Ensuring your return is postmarked by the due date can save you unnecessary costs.

Incorrectly updating officer information: Schedule A should accurately reflect the officers for the reporting period. Failing to update or correct this information can result in the suspension of your corporation.

Neglecting to attach a request for filing period change if needed: If you're looking to align your franchise tax filing period with your corporate income tax period, you must complete and attach OTC Form 200F.

By paying close attention to these points and carefully reviewing the instructions provided on the form, you can avoid common pitfalls and ensure your Oklahoma Minimum Franchise Tax return is filed correctly and on time.

Documents used along the form

When filing the Oklahoma Minimum Franchise Tax Form, businesses often need to prepare and submit additional forms and documents. These ensure compliance with state regulations and provide the Oklahoma Tax Commission (OTC) with necessary details for accurate tax assessment and collection.

- Annual Franchise Tax Report: This comprehensive report details the corporation's activities, financial status, and assets within Oklahoma. It serves as the primary document for calculating the franchise tax owed, based on the company's capital employed in the state.

- Form OTC-200F, Request to Change Franchise Tax Filing Period: Companies looking to align their franchise tax reporting period with their fiscal year can use this form to request a change. It helps synchronize tax obligations with corporate accounting practices, providing convenience and consistency.

- Registered Agent Fee Schedule: If a corporation is incorporated outside of Oklahoma but operates within the state, it must annually validate its registered agent's information using this schedule. The document accompanies the franchise tax form to fulfill the state's requirement for an in-state point of contact.

- Schedule A - Corporate Officer Information: Listing the company's current officers, including their contact information and social security numbers, this schedule is crucial for maintaining up-to-date records with the OTC, assisting in legal and official correspondence.

- Balance Sheet and Income Statement: Although not a form, providing the most recent balance sheet and income statement supports the tax worksheet's figures, ensuring the franchise tax calculation's accuracy based on the company's financial condition at the close of the latest income tax accounting year.

Together, these documents complement the Oklahoma Minimum Franchise Tax Form, providing a full picture of the business's activities and financial status in Oklahoma. Proper completion and submission of all relevant forms ensure compliance with state tax laws, helping businesses avoid penalties and maintain good standing.

Similar forms

The Oklahoma Minimum Franchise Tax Form is quite similar to the Internal Revenue Service (IRS) Form 1120, which is the U.S. Corporation Income Tax Return. Both forms require corporations to report their financial activities over the fiscal year, including assets, liabilities, and calculation of owed taxes based on operational metrics. The Oklahoma form focuses on the franchise tax, which is based on the capital employed within the state, while the IRS form calculates income tax owed to the federal government. Each form requires detailed financial statements and schedules of officers, emphasizing the importance of accurate financial reporting.

Another document that bears resemblance is the Annual Report filed with the Secretary of State in many jurisdictions. These reports often collect similar information about company assets, officer details, and the company's operations within the state over the reporting period. Like the Oklahoma Minimum Franchise Tax Form, these annual reports are crucial for maintaining good standing in the state of incorporation, affecting the company’s legal and operational status within that state.

Form 2553, Election by a Small Business Corporation, submitted to the IRS, shares commonalities as well. This form is used by corporations opting to be taxed as S corporations, affecting their tax obligations. Like the Oklahoma form, it deals with tax status and requires detailed information about the company’s officers. Both forms play a pivotal role in determining a company’s tax liabilities and how they are viewed by regulatory bodies, albeit in different tax contexts.

The Statement of Information or Initial/Annual Report forms that corporations must file with their state's division of corporations closely mirror the Oklahoma form in terms of content and purpose. These documents gather data about the company’s officers, registered agent, and principal business activities. They’re essential for ensuring that the public and the state have access to current information about the business, similar to the accountability and transparency objectives served by the Oklahoma Minimum Franchise Tax Form.

Similarly, the Business Privilege Tax Return, required in some states, has a comparable function to the Oklahoma form. This tax is assessed on the privilege of doing business within the state and is calculated based on business capital or net worth. The parallels include a focus on the financial aspects of a business's operation within a specific jurisdiction and the requirement for detailed financial disclosures.

The Unemployment Insurance Tax Filings that businesses must submit to their state's unemployment insurance agency also share similarities. Though focused on unemployment insurance contributions rather than franchise tax, both types of forms calculate obligations based on the company's payroll and employee data. They ensure businesses contribute appropriately to state-managed funds, impacting both the company and its employees.

Payment Vouchers, such as those used to make estimated tax payments or accompany tax filings, are reminiscent of the detachable payment slip found on the Oklahoma form. These vouchers facilitate the accurate processing of payments and ensure they are credited to the correct account, just as the detachable report section in the Oklahoma form specifies the franchise tax owed and provides a means for its submission.

Lastly, the Articles of Incorporation, filed when establishing a corporation in any state, set the foundation that documents like the Oklahoma Minimum Franchise Tax Form build upon. These initial filings detail the company’s structure, purpose, and initial officers, establishing the entity’s legal identity. Both are critical in defining a company's obligations, rights, and presence within a state’s legal and economic framework.

Dos and Don'ts

When preparing the Oklahoma Minimum Franchise Tax form, it is important to follow certain guidelines to ensure that the process is smooth and error-free. Here are some key dos and don'ts to keep in mind:

- Do carefully review the preprinted name and address for accuracy. If any information is incorrect, mark Item E on the form and provide the correct details on the back of the return.

- Do use the tax worksheet included with the form to accurately calculate your tax liability, ensuring that you qualify to use this form based on your tax amount being either the minimum $10.00 or the maximum $20,000.00.

- Do print all figures within the boxes provided to ensure that your report is properly processed. Use a #2 pencil or black ink pen, as required by the instructions.

- Do detach the return portion of the form and return it with your payment and schedule of officers in the enclosed return envelope before the due date to avoid any assessment of interest and penalty.

- Don't ignore the need to update preprinted information if it is incorrect. Failing to provide current and accurate information can lead to processing delays and may impact the status of your filing.

- Don't staple, fold, or use paper clips on your return form, as this can interfere with the processing of your document.

- Don't neglect the specific line instructions provided on the back of the form for completing lines 1 through 6. These instructions are designed to help you accurately complete your form.

- Don't forget to sign and date your return. An unsigned form may be considered incomplete and could delay processing or result in penalties.

Following these guidelines can help ensure that your Oklahoma Minimum Franchise Tax form is correctly filled out and submitted on time, thereby avoiding unnecessary penalties and delays.

Misconceptions

There are several misconceptions about the Oklahoma Minimum Franchise Tax form that need to be addressed to ensure that businesses can file accurately and with confidence. Understanding these common misunderstandings can help prevent mistakes and avoid potential penalties for incorrect filings.

- One form fits all businesses: This specific Form 215 is only for delinquent filers, not for current reporting. Companies with different tax circumstances may need a different form.

- Any company asset level can use this form: The form is specifically for those whose tax liability falls at the minimum of $10.00 or the maximum of $20,000. Companies outside of these thresholds must seek an alternative form.

- Correction of name and address is optional: If the preprinted information is incorrect, it’s crucial to check box E and make corrections. Accurate details are vital for proper processing.

- Capital employed calculation is straightforward: The worksheet requires detailed calculations, including total assets, business done, and a choice between two methods for determining the Oklahoma capital employed percentage. It's important to follow closely to avoid errors.

- The franchise tax rate is uniform: The tax calculation is based on the capital employed in Oklahoma, with a rate of $1.25 per $1,000, and exemptions apply if capital is below $8,000 or over $16,000,000.

- Filing the form is all that’s required: Besides filing Form 215, corporations must also return the schedule of officers and any applicable fees to remain in good standing.

- Delinquent status begins immediately after the due date: The tax and report are considered delinquent if not paid by August 31 or, for those aligning with their corporate income tax period, by the 15th day of the third month after their tax year ends.

- The form automatically updates the Oklahoma Tax Commission (OTC) on corporate changes: Filers need to actively check box E for changes in pre-printed information or complete necessary sections for updates, such as changes in corporate officers.

Understanding these key points about the Oklahoma Minimum Franchise Tax Form 215 can help businesses ensure that they are compliant with state tax requirements, thus avoiding potential penalties and interest for late or incorrect filings. If there's uncertainty, contacting the OTC for guidance is recommended.

Key takeaways

Filling out and using the Oklahoma Minimum Franchise Tax Form 215 requires attention to detail and adherence to specific instructions provided by the Oklahoma Tax Commission (OTC). Here are key takeaways that businesses should keep in mind:

- Eligibility for using Form 215 is determined by whether a business's tax liability falls within the minimum $10.00 or the maximum $20,000.00 range. Companies exceeding or falling below these thresholds must contact the OTC for the appropriate form.

- Corrections to preprinted information such as the name and address on the form should be indicated in Box E and detailed on the back of the return. This ensures that the OTC has the most current information.

- The calculation of the franchise tax relies on a worksheet which requires businesses to report their total assets and business done both within Oklahoma and everywhere. This information helps in determining the percentage of capital employed in Oklahoma, which in turn, affects the tax rate applied.

- It's mandatory to submit the completed form, along with the schedule of officers and the appropriate payment, before the specified due date to avoid incurring penalties and interest. The form itself provides detailed instructions on timelines and penalties for late submissions.

Adhering to the guidelines set forth by the Oklahoma Tax Commission and ensuring accurate and timely filing can help businesses avoid unnecessary penalties and maintain compliance with state tax laws.

Popular PDF Documents

How to Issue 1099 - Important caution notes for filers, particularly highlighting electronic filing mandates for financial institutions.

Form 709 - The form requires detailed information about the donor, the recipient, and the nature of the gift, ensuring complete transparency.