Get Non Erisa Loan Application Form

The Non-ERISA Loan Application form serves as a crucial document for individuals looking to borrow against their VALIC Annuity Accounts. This form, specifically designed for all plan types within the framework of VALIC, a Houston, Texas-based Variable Annuity Life Insurance Company, streamlines the process of requesting a loan. Applicants are required to disclose personal and employment information, alongside specifying the desired loan terms that detail the minimum and maximum borrowable amounts—ranging from $1,000 to $50,000—based on the lesser of specific regulatory limits or 50% of their vested account value. Additionally, the application outlines the repayment terms, underscoring the incidence of a processing fee and possible variations based on the borrower's employment status with the sponsoring employer. Mailing instructions for the loan check, vesting determination for employer contribution sources, plan administrator approval, and comprehensive account verification processes are also included to ensure a holistic evaluation of the applicant's eligibility. The form further incorporates sections dedicated to securing and approving the loan request, emphasizing the termination of the IncomeLOCK option upon loan approval. By furnishing detailed instructions and requiring thorough disclosures, this application not only safeguards the interests of the borrower and the lender but also aligns with relevant legal and regulatory standards, ensuring a seamless transaction.

Non Erisa Loan Application Example

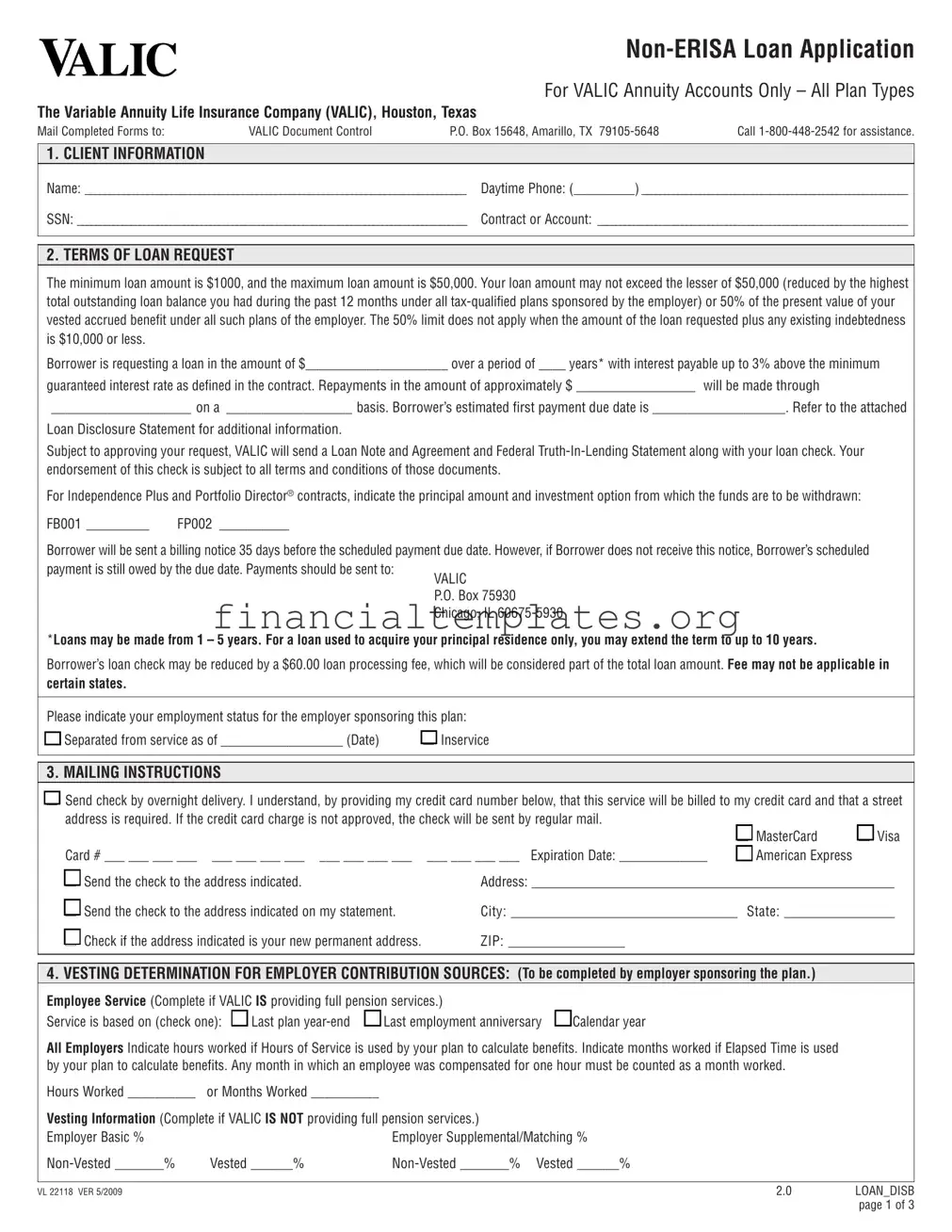

For VALIC Annuity Accounts Only – All Plan Types

The Variable Annuity Life Insurance Company (VALIC), Houston, Texas

Mail Completed Forms to: |

VALIC Document Control |

P.O. Box 15648, Amarillo, TX |

Call |

|

|

|

|

|

|

1. CLIENT INFORMATION |

|

|

|

|

Name: ________________________________________________________________________________ |

Daytime Phone: (_________) ____________________________________________________________ |

|||

SSN: ________________________________________________________________________________________ |

Contract or Account: ______________________________________________________________________ |

|||

|

|

|

|

|

2. TERMs OF LOAN REquEsT

The minimum loan amount is $1000, and the maximum loan amount is $50,000. Your loan amount may not exceed the lesser of $50,000 (reduced by the highest total outstanding loan balance you had during the past 12 months under all

Borrower is requesting a loan in the amount of $_____________________ over a period of ____ years* with interest payable up to 3% above the minimum

guaranteed interest rate as defined in the contract. Repayments in the amount of approximately $ _________________ will be made through

____________________ on a __________________ basis. Borrower’s estimated first payment due date is ___________________. Refer to the attached

Loan Disclosure Statement for additional information.

Subject to approving your request, VALIC will send a Loan Note and Agreement and Federal

For Independence Plus and Portfolio Director® contracts, indicate the principal amount and investment option from which the funds are to be withdrawn:

FB001 _________ |

FP002 __________ |

Borrower will be sent a billing notice 35 days before the scheduled payment due date. However, if Borrower does not receive this notice, Borrower’s scheduled payment is still owed by the due date. Payments should be sent to:

*Loans may be made from 1 – 5 years. For a loan used to acquire your principal residence only, you may extend the term to up to 10 years.

Borrower’s loan check may be reduced by a $60.00 loan processing fee, which will be considered part of the total loan amount. Fee may not be applicable in

certain states.

Please indicate your employment status for the employer sponsoring this plan:

|

Separated from service as of __________________ (Date) |

l |

Inservice |

l |

3. MAILINg INsTRuCTIONs |

|

|

|

|

|

|

l Send check by overnight delivery. I understand, by providing my credit card number below, that this service will be billed to my credit card and that a street |

||||||

address is required. If the credit card charge is not approved, the check will be sent by regular mail. |

l MasterCard |

l Visa |

||||

|

|

|

|

|

||

Card # ___ ___ ___ ___ |

___ ___ ___ ___ |

___ ___ ___ ___ |

___ ___ ___ ___ |

Expiration Date: _____________ |

l American Express |

|

l Send the check to the address indicated. |

|

Address: ____________________________________________________________ |

||||

l Send the check to the address indicated on my statement. |

City: _____________________________________ State: __________________ |

|||||

l Check if the address indicated is your new permanent address. |

ZIP: ___________________ |

|

|

|||

4. VEsTINg DETERMINATION FOR EMPLOYER CONTRIBuTION sOuRCEs: (To be completed by employer sponsoring the plan.)

Employee service (Complete if VALIC Is providing full pension services.) |

||

Service is based on (check one): |

l Last plan |

l Last employment anniversary |

l

Calendar year

All Employers Indicate hours worked if Hours of Service is used by your plan to calculate benefits. Indicate months worked if Elapsed Time is used by your plan to calculate benefits. Any month in which an employee was compensated for one hour must be counted as a month worked.

Hours Worked __________ |

or Months Worked __________ |

|

|

Vesting Information (Complete if VALIC Is NOT providing full pension services.) |

|

||

Employer Basic % |

|

Employer Supplemental/Matching % |

|

Vested ______% |

|

||

|

|

|

|

VL 22118 VER 5/2009 |

|

2.0 |

LOAN_DISB |

|

|

|

page 1 of 3 |

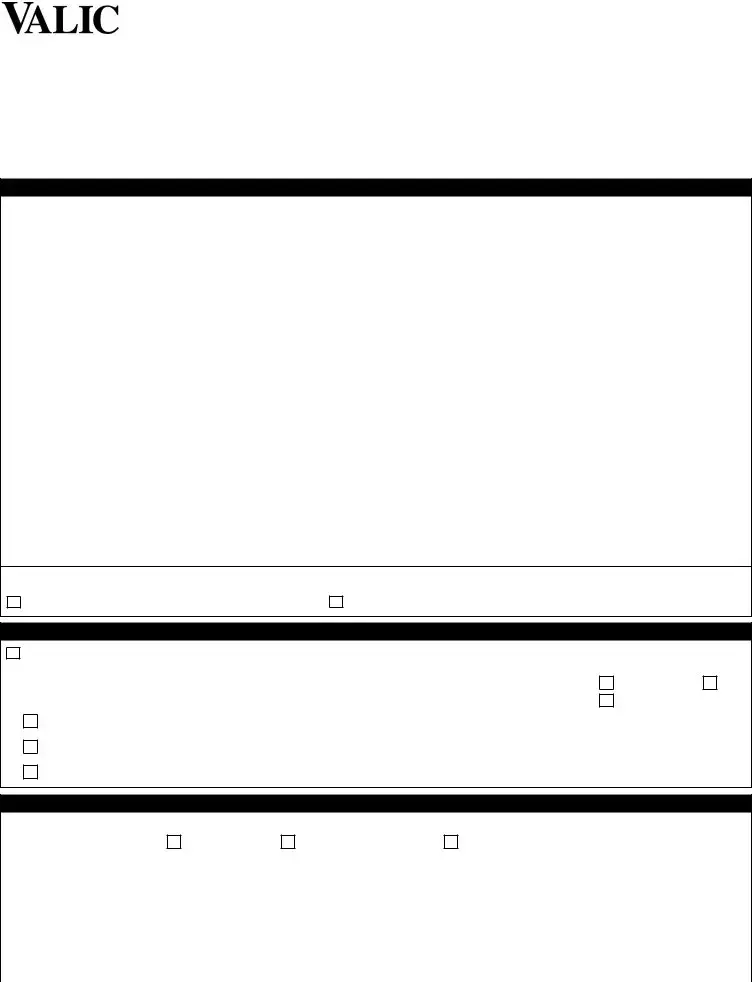

5. PLAN ADMINIsTRATOR APPROVAL

To be completed where required under your employer’s plan.

•I approve this loan in accordance with current plan provisions and all applicable laws and regulations.

•I verify that the information provided on this form for purposes of this distribution is correct to the best of my knowledge.

__________________________________________________________________________

Plan Administrator or Authorized Representative Name (Print) |

|

__________________________________________________________________________ |

_____________________ |

Plan Administrator or Authrorized Representative Signature |

Date |

sPECIAL NOTICE FOR INCOMELOCK OPTION

special note to IncomeLOCK participants: If a loan is taken on an account with the IncomeLOCK option, the IncomeLOCK option will be terminated and all benefits will cease. Once terminated, the IncomeLOCK option can not be added back to the contract.

6. ACCOuNT VERIFICATION (skip this section if your plan has only one provider or you are not in a 403(b) Plan.) |

||

Plan type of my account: |

l 403(b) |

l 401(a) or 401(k) (If 401(a) or 401(k), skip to Section 7) |

This section is applicable only to a loan from a 403(b) plan: If you are requesting a loan from a 403(b) plan and Plan Administrator or

I have funds under this or any other plan sponsored by this Employer with other investment providers: lYes lNo (If no, skip to Section 7.) If you answered “Yes” to the question above, the Loan Supplement for Investment Providers (on page 3) will be required.

List all other investment providers and account number(s) under this Plan where contributions have been made at any time:

Investment Provider

Customer service Phone Number

Account Number

Use a separate sheet for additional accounts and/or loans.

7. sECuRITY AND APPROVAL FOR LOAN

•Borrower understands that Borrower will be pledging to VALIC as security for the loan the following amounts (1) the cash surrender value of the contract or account in an amount equal to the value of the loan; (2) the portion of the loan interest due with a quarterly loan payment; (3) any applicable surrender charge; and (4) all interest credited on (1), (2), and (3) held in reserve until the loan is repaid or foreclosed upon. Any applicable surrender charge is calculated as if I partially surrendered an amount equal to the loan balance as of the beginning of the loan term. The reserve is not subject to withdrawal, surrender, reallocation, transfer, assignment, or pledge to anyone other than VALIC.

•Borrower certifies that Borrower does not have any loans under this or any other plan sponsored by this employer (or under a plan sponsored by any other employer related to the employer sponsoring this plan) that would cause any amount of this loan to be in excess of the applicable loan limits described under Section 2 of the attached Loan Disclosure Statement.

•Borrower certifies that Borrower does not have any outstanding defaulted loans under this or any other plan sponsored by this employer (or under a plan sponsored by any other employer related to the employer sponsoring the plan).

•Borrower understands that this loan will terminate the IncomeLOCK option, if any, and benefits associated with the IncomeLOCK option.

•Once terminated, the IncomeLOCK option can not be added back to the contract.

•Borrower acknowledges that Borrower has read and understands the attached Loan Disclosure Statement.

•Borrower certifies that the information provided above is true and correct to the best of Borrower’s knowledge.

•Borrower authorizes VALIC to confirm the accuracy of information provided with listed providers and authorizes such providers to confirm the information herein, subject to the requirement that the information is used solely for purposes of satisfying the restrictions under the Plan. Borrower understands request will not be processed until confirmed.

_________________________________________________________________________ |

_____________________ |

Borrower’s Signature |

Date |

VL 22118 VER 5/2009 |

2.0 |

LOAN_DISB |

|

|

page 2 of 3 |

|

Loan supplement for Investment Providers |

|

(For use with decentralized |

The Variable Annuity Life Insurance Company (VALIC), Houston, Texas |

(skip this page if your plan has only one provider or |

you are not in a 403(b) Plan.) |

Borrower: Your request for a loan from your 403(b) account and answering “Yes” to the question in Section 6 also requires the submission of this supplemental form to your other investment providers to determine eligibility for a loan distribution from your employer’s plan. You should complete Box A (below) and provide a copy of this form to each of the other investment provider(s) for completion of Box B. Upon full execution of this form, the supplemental form can then be submitted along with the Loan Application form.

Remit this page to each of the investment providers listed in section 6 for completion of required information:

PARTICIPANT INFORMATION

Name: ______________________________________________________ |

Daytime Phone: (________) _____________________________________ |

SSN: _______________________________________________________ |

Contract or Account: ___________________________________________ |

Address: ____________________________________________________ |

City: _______________________ State: _________ ZIP: ___________ |

BOX A:

Name of Investment Provider:

Employer Name:

Plan Name:

Participant’s Name:

Participant’s Address:

Provide Account #:

Provide Account #:

•I certify that the information I have provided is true and correct to the best of my knowledge.

•Borrower authorizes VALIC to confirm the accuracy of information provided with listed providers and authorizes such providers to confirm the information herein, subject to the requirement that the information is used solely for the purposes of satisfying the restrictions under the Plan. Borrower understands request will not be processed until confirmed.

________________________________________________________________________ |

_____________________ |

Participant’s Signature |

Date |

Investment Providers: Client has authorized VALIC to collect the following information. Complete the following table for each 403(b) account where contributions have been made at any time. Do not include accounts only containing transferred amounts transferred prior to 09/25/2007.

Return to Client upon completion. |

|

|

BOX B: |

Account #1 |

Account #2 |

|

|

|

Account Number(s): |

|

|

|

|

|

Account Balance(s): |

|

|

|

|

|

Account Balance(s) On 12/31/1988: |

|

|

|

|

|

Total Amount of Outstanding |

|

|

Loan Balance: |

|

|

|

|

|

Highest Total Outstanding Loan |

|

|

Balance Over Past 12 months: |

|

|

|

|

|

Describe status of Loan: |

|

|

Active, Defaulted, or Fully Repaid |

|

|

|

|

|

________________________________________________________________________ |

____________________________________________ |

|

Signature of Investment Provider |

|

Date |

________________________________________________________________________ |

____________________________________________ |

|

Printed name of Investment Provider |

|

Title of Investment Provider |

VL 22118 VER 5/2009 |

2.0 |

LOAN_DISB |

|

|

page 3 of 3 |

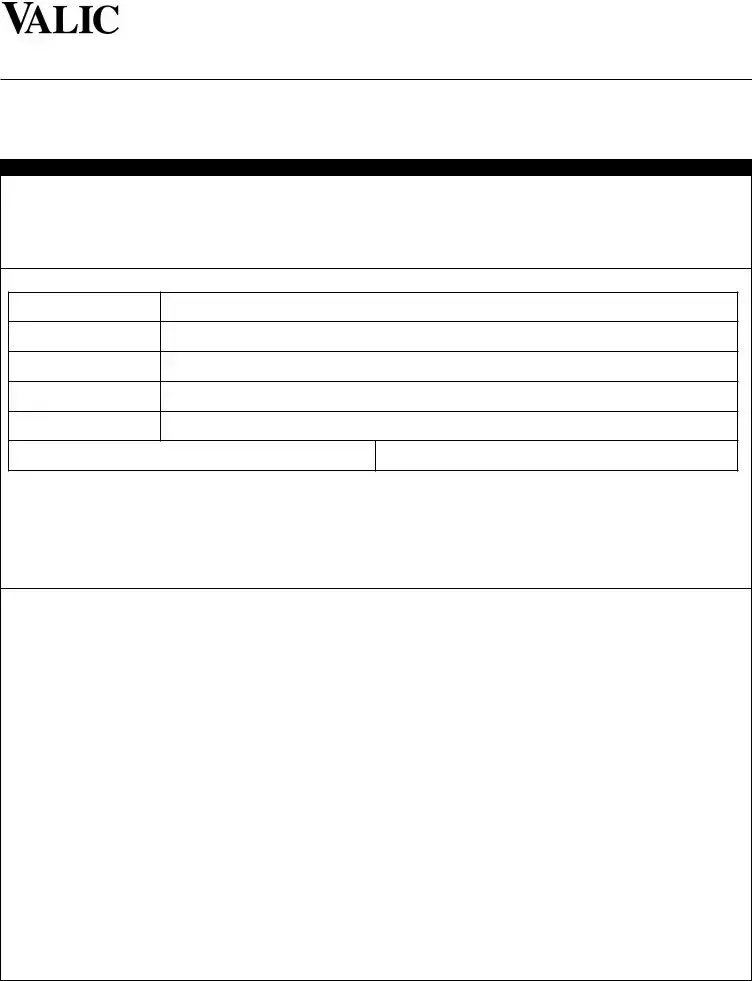

Loan Disclosure statement

THIs LOAN DIsCLOsuRE sTATEMENT gOVERNs YOuR LOAN APPLICATION AND ANY REsuLTINg LOAN.

Additional loans will not be allowed to participants with outstanding defaulted loans under this or any other plan sponsored by this employer (or under a plan sponsored by any other employer related to the employer sponsoring this plan) until these defaulted loans have been repaid with outside funds or can be fully foreclosed.

Payments of principal and interest should be made by check payable to THE VARIABLE ANNUITY LIFE INSURANCE COMPANY.

The remittance address will be indicated on the payment coupon. However, payments are due regardless of receipt of payment coupon. For additional information contact our Client Care Center at

1. APPLICABILITY

Loans as described herein are available only from VALIC annuity contracts and accounts issued to

The IncomeLOCK option is not available if there is an outstanding loan on the contract. Prior to adding the IncomeLOCK option to the contract, any outstanding loan must first be paid off. If a loan is taken after the IncomeLOCK option is in effect, the IncomeLOCK option and associated benefits will cease. Once terminated, the IncomeLOCK option can not be added back to the contract.

2. AMOuNT OF LOAN

VALIC processes loans for loan qualification purposes solely on the basis of employer

VALIC assumes no responsibility for the processing of loans other than in accordance with the limits described below as applied to VALIC annuity contracts and accounts issued to such employer

a.The availability and amount of a loan are subject to any applicable restrictions in the plan.

b.Both fixed and variable VALIC accounts are considered for purposes of qualifying a loan, but only the vested portion of a fixed

c.The maximum amount you may borrow may not exceed the lesser of $50,000 [reduced by the highest total outstanding loan balance you had during the past 12 months under all

d.Loans are not made to participants who have begun receiving annuity payments under the contract or account.

e.VALIC may from time to time establish minimum loan amounts. Refer to your VALIC contract for the current minimum.

f.If a participant annuitizes, surrenders the contract or account, or dies before the loan is repaid, the annuity value or death benefit payable under the contract will be reduced by the outstanding loan amount, delinquent quarterly interest payments, prorated portion of quarterly loan interest and any applicable surrender charge.

3.TERMs OF LOAN

a.Amortized equal loan payments of principal and interest are due on the last day of each quarter of the loan year.

b.Quarterly payments are required. Quarterly payment obligations may not be satisfied more than one quarter in advance.

c.Payments received by VALIC will be applied in this order: First, to any outstanding payments due

Second, to the current quarterly payment due Third, to the next quarterly payment Fourth, to the principal balance

d.The loan balance may be repaid in full at any time. Please contact the Client Care Center at

4.sECuRITY FOR LOAN

a.VALIC will place in a security reserve an amount equal to the sum of the loan amount, the contract surrender charge as if the loan amount had been surrendered at the start of the loan term, if applicable, and all interest credited to the foregoing amounts.

b.I pledge the foregoing amount in the security reserve to VALIC as security for this loan. This amount is not subject to withdrawal, surrender, reallocation, transfer, assignment or pledge to anyone other than VALIC.

c.The portion of the reserve equal to the loan balance and interest thereon will accumulate minimum guaranteed interest at the applicable contract rate. The portion of the reserve equal to the amount necessary to satisfy the surrender charge, if applicable, and interest thereon, will earn interest at the applicable minimum guaranteed interest rate or such higher rate declared by VALIC’s Board of Directors but no less than the minimum guaranteed rate under the contract.

d.As loan balance repayments are made,

e.VALIC will foreclose on the security reserve for the foreclosure amount upon default or when any withdrawal or plan restrictions no longer apply. If the loan is foreclosed upon, any amount in the security reserve in excess of the foreclosure amount will be credited to the contract or account.

5.LOAN DEFAuLT

a.If Borrower fails to make any scheduled payment, the loan is considered past due. If the past due payment amount remains unpaid for 90 days or such other time period as defined under the terms of the plan or loan provisions (not to extend longer than permitted under applicable regulations or rulings of the Internal Revenue Service or the Department of Labor), the loan will be

in default and the outstanding loan amount, together with any accrued interest, will be immediately due and payable.

b.The defaulted loan amount will be reported on IRS Form

c.If there are any withdrawal or plan restrictions, then, upon default, VALIC may be unable to immediately foreclose upon the security

VL 22118 VER 5/2009

Loan Disclosure statement

reserve and discharge your loan. VALIC may only foreclose upon the security reserve upon the occurrence of a distributable event under your plan, such as your attainment of age 59½, death, disability

or separation from service. Until such time, VALIC must continue to carry your loan and credit interest to you as described above. At the same time, you will continue to accrue interest equal to the minimum guaranteed interest rate under your current contract until the loan is repaid or foreclosed upon.

d.You may repay the defaulted loan amount plus interest due to VALIC prior to foreclosure. This repayment must be in full. Contact the Client Care Center

6.gENERAL LOAN INFORMATION

a.Can I make payments through payroll deductions?

Some employers do have agreements with VALIC to offer their employees the option of payroll deductions for loan repayments. If available to you, it’s a simple process of signing a VALIC agreement indicating how much and how often you want deductions made. We will then coordinate with your employer to begin deductions. Check with your employer to see if they offer this benefit.

b.How often can I send in a loan payment?

Payments are due every 90 days from the effective date of your loan. However, you can send payments as often as you like as long as the amount due each quarter is paid by the scheduled due date. Remember to include your loan account number(s) on your check to ensure proper crediting.

Note: Only one quarterly payment may be paid in advance. When making more than one payment in a quarter, any excess after two payments will be credited to the principal of the loan.

c.Will I receive confirmation of my loan payment?

Yes. Payments will be reflected on your account statement. The statement will reflect the amount of principal paid on your loan and the amount of guaranteed interest credited to your account, both of which are returned to your regular account from your loan security reserve amount.

Can I pay my loan back prior to the final due date without penalties?

Yes. You can contact our Client Care Center for a payoff quote and repay the loan at any time without any prepayment penalties.

Please send completed forms to:

VALIC Document Control

P.O. Box 15648

Amarillo, TX

Call

VL 22118 VER 5/2009

Document Specifics

| Fact Name | Detail |

|---|---|

| Form Use | Non-ERISA Loan Application for VALIC Annuity Accounts Only – All Plan Types. |

| Contact Information | For assistance, contact VALIC at 1-800-448-2542. |

| Loan Amount Limits | Minimum loan amount is $1,000 and the maximum is $50,000, subject to certain conditions. |

| Loan Repayment Terms | Loans may be made from 1 – 5 years, or up to 10 years for loans used to acquire a principal residence. |

| Interest Rate | Interest payable up to 3% above the minimum guaranteed interest rate as defined in the contract. |

| Processing Fee | A $60.00 loan processing fee may apply, reducible from the loan check amount. |

| Payment Procedure | Borrowers will be sent a billing notice 35 days before the payment due date. |

| Applicable Law | Plans not subject to the Employee Retirement Income Security Act of 1974 (ERISA). |

Guide to Writing Non Erisa Loan Application

Once you've decided to apply for a Non-ERISA Loan from VALIC, understanding the process and knowing what to expect next is crucial. Submitting a well-prepared application ensures a smoother process. Following your application's submission, VALIC will review the information provided to approve your loan request. If approved, you will receive a Loan Note and Agreement along with a Federal Truth-In-Lending Statement and your loan check. It is important to thoroughly review these documents, as your endorsement of the loan check indicates acceptance of their terms. Here are the steps you need to follow to complete the application form correctly:

- Begin with the CLIENT INFORMATION section. Fill in your full name, contact number during the day, Social Security Number (SSN), and your contract or account number.

- In the TERMs OF LOAN REQUEST section, specify the amount you are requesting, the loan period in years, the interest rate, your repayment amounts, the mode and frequency of repayments, and the estimated first payment due date.

- If applicable, for INDEPENDENCE PLUS and Portfolio Director® contracts, indicate the desired principal amount and the specific investment option to withdraw funds from, using the codes provided (FB001 for Independence Plus, FP002 for Portfolio Director).

- Select your employment status in relation to the employer sponsoring the plan—either separated from service as of a specific date, or inservice.

- For MAILING INSTRUCTIONS, choose the preferred method to receive your check and provide relevant details like your address or credit card information for overnight delivery.

- Complete the VESTING DETERMINATION FOR EMPLOYER CONTRIBUTION SOURCES section, which may require assistance from your employer to provide accurate service information or vesting percentages.

- Should your plan require it, obtain the PLAN ADMINISTRATOR APPROVAL, including a signature and date from the plan administrator or authorized representative.

- If you have an IncomeLOCK option, note that taking out this loan will terminate that option, with all benefits ceasing, and acknowledge this in the provided space.

- Skip the ACCOUNT VERIFICATION section if it does not apply to you. If it does, ensure to accurately detail other investment providers if you’re part of a decentralized 403(b) plan.

- In the SECURITY AND APPROVAL FOR LOAN section, read and understand the security you're providing for the loan, the certification against outstanding loans, and the impact on the IncomeLOCK option if applicable. Confirm the accuracy of the information provided here and throughout the form.

- Sign and date at the bottom of the form to authorize the loan process to begin, confirming that all information is correct and that you consent to VALIC verifying this information as necessary.

- If required for a 403(b) plan, complete the Loan Supplement for Investment Providers form, detailing investment provider information and participant information, and obtain the required signatures.

After completing these steps, review the entire form to ensure accuracy and completeness. Then, send the completed form to the address specified for VALIC Document Control. Remember that assistance is available if you have questions or need help with the form by calling VALIC at 1-800-448-2542. Taking care with your application can help avoid delays in the processing of your loan request.

Understanding Non Erisa Loan Application

What is a Non-ERISA Loan Application?

A Non-ERISA Loan Application is a form used by individuals who have annuity accounts under non-ERISA (Employee Retirement Income Security Act of 1974) plans with VALIC (The Variable Annuity Life Insurance Company) to request a loan. It involves submitting personal and loan request details, adhering to terms, and obtaining approval from plan administrators where required.

Who can apply for a Non-ERISA Loan?

Individuals who have VALIC Annuity Accounts and are part of a plan that is not governed by ERISA are eligible to apply. This includes plans like 403(b) and non-ERISA 457(b) plans.

How much can I borrow with a Non-ERISA Loan?

The minimum loan amount is $1,000 and the maximum is $50,000, subject to the lesser of $50,000 (minus the highest outstanding loan balance from the past 12 months under all employer-sponsored plans) or 50% of your vested benefit under such plans. A $10,000 exception to the 50% rule applies under certain conditions.

What are the terms for repaying the loan?

Loans can have repayment terms ranging from 1 to 5 years, with an extension up to 10 years allowed for loans used to acquire a principal residence. Repayments are made with interest up to 3% above the contract's minimum guaranteed interest rate, on a regular basis, as detailed in the loan request.

Is there a fee for processing a Non-ERISA Loan?

Yes, there may be a $60.00 loan processing fee, which is considered part of the total loan amount. This fee could vary or not be applicable in certain states.

What happens if I do not receive a billing notice?

Borrowers are sent a billing notice 35 days before the payment due date, but if a notice is not received, the scheduled payment is still due by the original date. Payments must be sent to the address provided, with or without a billing notice.

Can I repay my loan early?

Yes, the loan can be repaid in full at any time before the end of the loan term without any prepayment penalties. Contact VALIC for a payoff quote to include all principal and interest due.

What security is required for a Non-ERISA Loan?

The borrower pledges as security to VALIC amounts including the cash surrender value of the contract or account equal to the loan value, loan interest due with a quarterly payment, any applicable surrender charge, and all interest credited on these amounts held in reserve.

What happens if I default on my Non-ERISA Loan?

If a borrower fails to make a scheduled payment and it remains unpaid for 90 days, the loan is considered defaulted. The outstanding loan amount and accrued interest become immediately due. Defaulting on the loan may lead to foreclosure on the security reserve, and the defaulted loan amount will be treated as a taxable distribution, possibly incurring an early withdrawal penalty if under age 59½.

Common mistakes

Filling out a Non-ERISA Loan Application form requires careful attention to detail to ensure accuracy and compliance with the guidelines. Here are 10 common mistakes people often make when completing this form:

- Incorrect Client Information: Providing inaccurate details such as name, social security number (SSN), or contract/account numbers. Every piece of information needs to be double-checked for accuracy.

- Misunderstanding Loan Terms: Failing to request the correct loan amount within the allowed minimum of $1,000 and maximum of $50,000, or not understanding the limitations based on 50% of their vested accrued benefits.

- Incorrect Loan Period: Selecting a loan repayment period that doesn’t align with the maximum allowed terms, e.g., more than 5 years for general loans or more than 10 years for loans to acquire a principal residence.

- Overlooking Interest Rates: Not comprehending how the interest rate is determined or failing to calculate the approximate repayment amount correctly.

- Employment Status Errors: Incorrectly indicating employment status with the sponsoring employer, which can affect loan eligibility and terms.

- Payment Information: Skipping over the repayment details, such as the start date of the first payment or the frequency of the repayments, can lead to misunderstandings about the loan repayment schedule.

- Failing to Specify Delivery Instructions: Not clearly specifying how the check should be delivered or forgetting to provide a complete and accurate address may delay the receipt of the loan proceeds.

- Vesting Determination Oversights: Not completing the vesting section accurately or failing to provide the necessary information if VALIC is not providing full pension services, can result in the loan application being delayed or denied.

- Plan Administrator Approval: Not obtaining the required plan administrator’s approval or failing to provide the plan administrator’s signature where required under the employer’s plan.

- Inaccurate Account Verification: For borrowers with multiple investment providers, not accurately listing all other investment providers and account numbers can lead to incomplete consideration of all assets, affecting loan eligibility.

To avoid these common mistakes, it’s crucial to read all sections carefully, understand the loan terms and requirements, and verify all provided information before submission. Seeking assistance if any part of the form is unclear can also help ensure the application is completed correctly.

Documents used along the form

Applying for a Non-ERISA Loan is just the beginning when it comes to the variety of forms and documents individuals might need to properly request and manage a loan. Understanding what these documents are and their purposes can significantly streamline the application process and ensure compliance with all requirements. Here's a concise overview of other forms and documents often needed alongside the Non-ERISA Loan Application form.

- Loan Disclosure Statement: This document outlines the terms, conditions, and the financial aspects of the loan, ensuring transparency between the borrower and the lender. It includes information about the loan amount, repayment schedule, interest rates, and any fees associated with the loan.

- Loan Note and Agreement: An official agreement between the borrower and the lender that details the loan's terms and conditions, repayment obligations, and security interests if applicable. It acts as a legally binding contract that outlines both parties' responsibilities and rights.

- Federal Truth-In-Lending Statement: This statement provides a clear breakdown of the loan’s terms, including the annual percentage rate (APR), finance charges, amount financed, and the total payments required. It helps borrowers understand the cost of borrowing.

- Loan Repayment Schedule: A detailed schedule that outlines the timing and amount of each repayment installment over the life of the loan. It helps borrowers understand when payments are due and how much they need to pay.

- Billing Notice: A document sent to the borrower ahead of each payment due date, summarizing the amount due and the due date. Even if the notice is not received, the borrower is still responsible for making the payment on time.

- Employment Verification Form: Used to verify the borrower's employment status with the employer sponsoring the plan. This may affect loan eligibility and terms, especially concerning loans intended for principal residence acquisition.

- Plan Administrator Approval Form: A form that must be completed and signed by the plan administrator, confirming that the loan request complies with current plan provisions and applicable laws and regulations.

- Loan Supplement for Investment Providers: For 403(b) plans that involve multiple investment providers, this form helps coordinate information about the borrower’s accounts across different providers to assess loan eligibility and terms.

Each of these documents plays a crucial role in the process of obtaining and managing a Non-ERISA Loan. The requirements may vary based on the employer, the plan, and state laws, making it important to consult with a financial advisor or the plan administrator for guidance tailored to individual circumstances. With a comprehensive understanding of these forms and documents, borrowers can navigate the loan process more effectively and ensure they meet all necessary requirements.

Similar forms

A Non-ERISA Loan Application, such as the one presented for VALIC Annuity Accounts, shares similarities with Personal Loan Application forms used by banks or other financial institutions. Both types of applications collect personal information about the borrower, such as name, Social Security Number, and employment status, to assess the borrower's ability to repay the loan. They also detail the terms of the loan request, including loan amount, repayment period, and interest rate, offering a clear understanding of the commitment from the borrower.

Another document with considerable resemblance is the Mortgage Application form. This form is used when an individual is applying for a loan to purchase real estate. Like the Non-ERISA Loan Application, a Mortgage Application requests detailed financial information, employment history, and a declaration of assets and liabilities. Both applications similarly assess the borrower's financial health and capability to fulfill the loan obligations, underlining their vested interest in ensuring the borrower doesn't default on the loan.

The Business Loan Application form also bears similarity to the Non-ERISA Loan Application. This type of application is specifically designed for businesses seeking financial support and, like its counterpart, requires detailed information about the business's financial status, ownership details, and the purpose of the loan. Both documents necessitate a thorough vetting process to evaluate the risk involved in lending and to establish terms that are feasible for both the lender and the borrower.

Credit Card Application forms are similar as well, in that they request personal financial information from the applicant to evaluate creditworthiness, just like the Non-ERISA Loan Application. Both forms play a pivotal role in determining the terms of the credit or loan offered, based on the applicant's risk profile. Additionally, both types of applications might lead to the issuance of an agreement outlining the credit or loan terms, signifying a binding contract between the two parties.

Finally, the Home Equity Line of Credit (HELOC) Application is quite akin to the Non-ERISA Loan Application. Both forms assess the value of the borrower's assets (in the case of a HELOC, the home's equity) to determine the maximum amount that can be borrowed. Information about the borrower's financial situation, including existing debts and income, are crucial in both applications for securing the loan and setting terms that ensure the borrower's ability to comply with repayment schedules.

Dos and Don'ts

Filling out a Non-ERISA Loan Application requires careful attention to detail and an understanding of the terms and conditions involved. Below are key dos and don'ts to consider during the process:

- Do carefully read the entire application form, including the Loan Disclosure Statement, before beginning to fill it out. This ensures you understand the terms and any obligations.

- Do verify the minimum and maximum loan amounts to ensure the amount you request is within the specified limits of $1,000 to $50,000, considering your vested benefits and any outstanding loans.

- Do provide accurate and complete information in every section required, including personal information, employment status, and desired loan terms.

- Do indicate your preferred method of receiving the loan check, whether by regular or overnight mail, and ensure the address provided is correct.

- Do ensure that the vesting information for employer contribution sources is properly filled out by your plan administrator if necessary.

- Don't forget to sign and date the application. An unsigned application can delay processing or result in a denial of the loan request.

- Don't underestimate the importance of providing your employment status accurately, as it may affect your eligibility or loan terms.

- Don't ignore the impact of a loan on your IncomeLOCK option, if applicable. Taking a loan will terminate this option along with its benefits.

By following these guidelines, you can help ensure your Non-ERISA Loan Application is complete and processed efficiently, avoiding common pitfalls and misunderstandings that can lead to delays or unexpected financial implications.

Misconceptions

There are several common misconceptions regarding the Non-ERISA Loan Application form, which can lead to confusion among individuals considering a loan. Understanding these misconceptions is crucial for making informed decisions. Below are seven misconceptions explained:

- Misconception 1: The Non-ERISA Loan Application is available for any type of loan. In reality, this application is specifically designed for loans against VALIC annuity accounts and is not applicable to other loan types.

- Misconception 2: There is no minimum loan amount requirement. Contrary to this belief, the application stipulates that the minimum loan amount is $1,000, ensuring that the loan process is utilized for substantial financial needs.

- Misconception 3: Borrowers can request a loan of any amount, regardless of their account balance. However, the form clearly states that the loan amount cannot exceed the lesser of $50,000 or 50% of the present value of the borrower’s vested accrued benefit, with certain conditions allowing for a minimum loan request.

- Misconception 4: The loan repayment period is flexible and can be extended indefinitely. The truth is that loans must be repaid within 1 to 5 years, with an exception for loans used to acquire a principal residence, which may be extended to up to 10 years.

- Misconception 5: Borrowers will not receive a bill if they do not receive a billing notice. The document makes it clear that borrowers are still responsible for making scheduled payments by the due date, regardless of whether they receive a billing notice.

- Misconception 6: It’s acceptable to have defaulted loans under other plans when applying. Applicants must certify they do not have outstanding defaulted loans under any plan sponsored by their employer or a related employer, ensuring financial responsibility.

- Misconception 7: The IncomeLOCK option remains active when a loan is taken. If a loan is taken on an account with the IncomeLOCK option, this option and its benefits will terminate, underscoring the impact a loan can have on specific account features.

Understanding the specific terms and conditions outlined in the Non-ERISA Loan Application form is essential for applicants to ensure that their expectations align with the realities of the loan process. This knowledge promotes responsible borrowing and financial planning.

Key takeaways

When completing the Non-ERISA Loan Application for VALIC Annuity Accounts, it is critical to understand specific requirements and conditions that affect the loan terms, eligibility, and repayment options. Below are key takeaways that applicants should bear in mind:

- The minimum loan amount one can request is $1,000, while the maximum amount is limited to $50,000. However, the actual loan amount may not exceed the lesser of $50,000 - accounting for the highest total outstanding loan balance during the past twelve months - or 50% of the present value of your vested benefits under the plans of the employer.

- A unique term of the loan application process is the provision for borrowers to request a loan over a period ranging from one to five years. For loans used to acquire a principal residence, the term can be extended up to 10 years. This flexibility allows for borrowing with repayment terms that can be adjusted based on the borrower’s need and capability.

- The borrower’s loan is subject to a processing fee of $60.00, which is included in the total loan amount. This fee, however, may be waived in certain states due to state-specific regulations.

- Loan repayments are arranged to be made on a predefined basis, with the first payment's due date estimated at the loan setup stage. This structured repayment ensures consistency and predictability for both the borrower and the lender.

- Borrowers are pledged to provide VALIC with the security for the loan, which includes the cash surrender value of the contract or account equal to the value of the loan, plus the portion of the loan interest due with a quarterly loan payment, any applicable surrender charge, and all interest credited on these amounts held in reserve until the loan is repaid or foreclosed upon.

- If a borrower takes a loan against an account with the IncomeLOCK option, this option will be terminated, and all benefits associated with it will cease. Importantly, once terminated, the IncomeLOCK option cannot be reinstated to the contract.

Understanding these key points ensures that borrowers are fully informed about the terms of their Non-ERISA Loan Application with VALIC, helping to manage expectations and obligations throughout the term of the loan.

Popular PDF Documents

Tax Affidavit Form - The collected data aids in property valuation and the equitable assessment of property taxes statewide.

IRS W-2 - An end-of-year tax form that reports an employee's annual wages and the taxes withheld.

Trs Qpp Loan Application - In Part B, applicants are asked to state the desired loan amount, which could be a specific dollar amount or the maximum allowable.