Get IRS Notice 1392 Form

When navigating the intricacies of United States taxation, international individuals working within its borders encounter a unique set of challenges and obligations. Essential to understanding and complying with these requirements is the IRS Notice 1392, a document that plays a pivotal role for nonresident aliens adjusting to the tax landscape in the U.S. This notice acts as a comprehensive guide, elucidating the specific rules and variations in tax withholding rates that are applicable to people from different countries, according to agreements and treaties between the U.S. and their home countries. It provides invaluable instructions for filling out W-4 forms, ensuring that employers withhold the appropriate amount of taxes from their paychecks. The significance of the IRS Notice 1392 cannot be overstated, as it not only aids in preventing under or over-withholding of taxes but also in navigating the complexities of tax laws that govern international workers in the United States. By familiarizing themselves with the contents of this notice, international employees and their employers can ensure compliance with U.S. tax obligations, thereby avoiding potential legal pitfalls and financial penalties.

IRS Notice 1392 Example

Notice 1392 |

Department of the Treasury |

Internal Revenue Service |

|

(Rev. January 2020) |

|

Supplemental Form

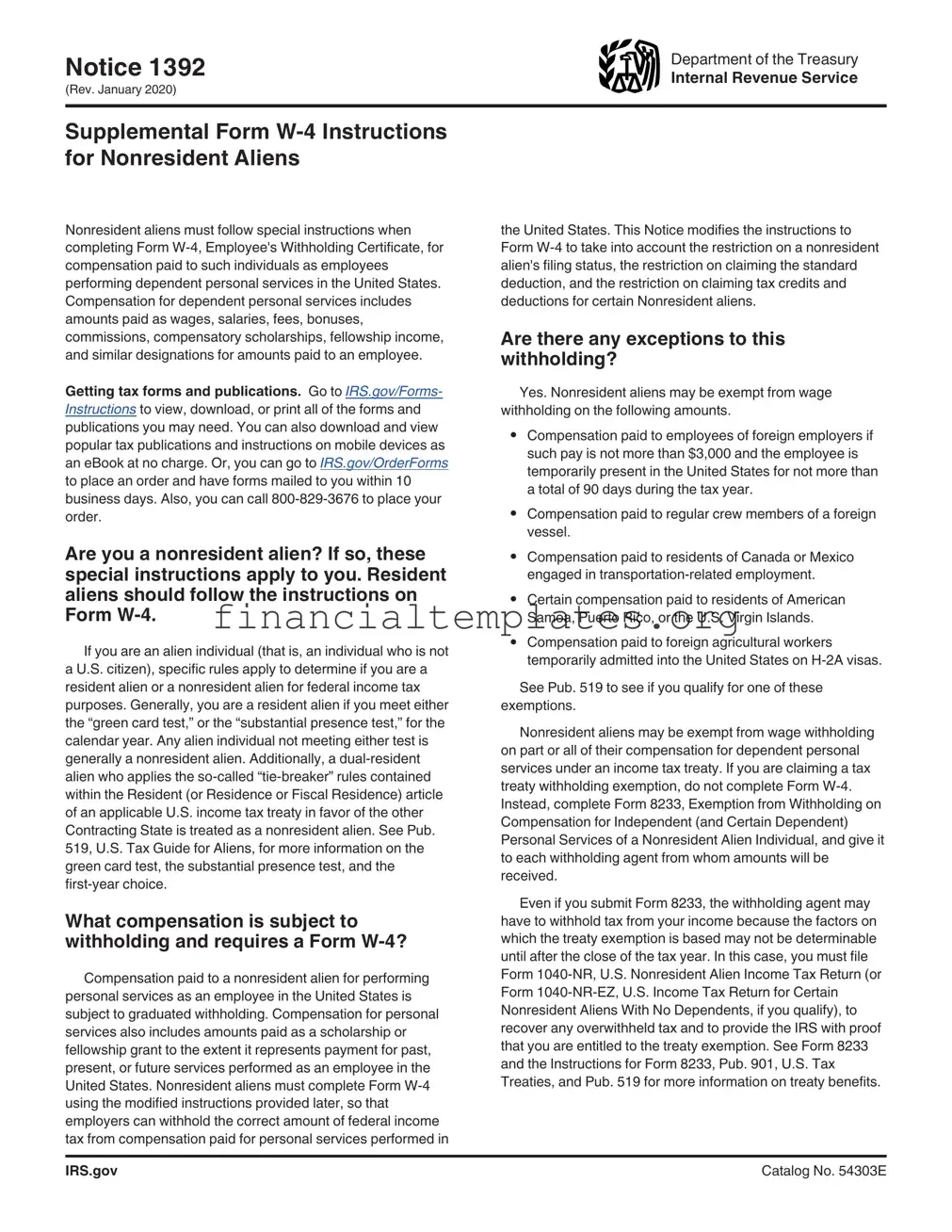

Nonresident aliens must follow special instructions when completing Form

Getting tax forms and publications. Go to IRS.gov/Forms- Instructions to view, download, or print all of the forms and publications you may need. You can also download and view popular tax publications and instructions on mobile devices as an eBook at no charge. Or, you can go to IRS.gov/OrderForms to place an order and have forms mailed to you within 10 business days. Also, you can call

Are you a nonresident alien? If so, these special instructions apply to you. Resident aliens should follow the instructions on Form

If you are an alien individual (that is, an individual who is not a U.S. citizen), specific rules apply to determine if you are a resident alien or a nonresident alien for federal income tax purposes. Generally, you are a resident alien if you meet either the “green card test,” or the “substantial presence test,” for the calendar year. Any alien individual not meeting either test is generally a nonresident alien. Additionally, a

What compensation is subject to withholding and requires a Form

Compensation paid to a nonresident alien for performing personal services as an employee in the United States is subject to graduated withholding. Compensation for personal services also includes amounts paid as a scholarship or fellowship grant to the extent it represents payment for past, present, or future services performed as an employee in the United States. Nonresident aliens must complete Form

the United States. This Notice modifies the instructions to Form

Are there any exceptions to this withholding?

Yes. Nonresident aliens may be exempt from wage withholding on the following amounts.

•Compensation paid to employees of foreign employers if such pay is not more than $3,000 and the employee is temporarily present in the United States for not more than a total of 90 days during the tax year.

•Compensation paid to regular crew members of a foreign vessel.

•Compensation paid to residents of Canada or Mexico engaged in

•Certain compensation paid to residents of American Samoa, Puerto Rico, or the U.S. Virgin Islands.

•Compensation paid to foreign agricultural workers temporarily admitted into the United States on

See Pub. 519 to see if you qualify for one of these exemptions.

Nonresident aliens may be exempt from wage withholding on part or all of their compensation for dependent personal services under an income tax treaty. If you are claiming a tax treaty withholding exemption, do not complete Form

Even if you submit Form 8233, the withholding agent may have to withhold tax from your income because the factors on which the treaty exemption is based may not be determinable until after the close of the tax year. In this case, you must file Form

IRS.gov |

Catalog No. 54303E |

Am I required to file a U.S. tax return even if I am a nonresident alien?

Yes. Nonresident aliens who perform personal services in the United States are considered to be engaged in a trade or business in the United States and generally are required to file Form

Nonresident aliens who are bona fide residents of U.S. possessions should consult Pub. 570, for information on whether compensation is subject to wage withholding in the United States.

Will my withholding amounts be different from withholding for my U.S. coworkers?

Yes. Nonresident aliens cannot claim the standard deduction. The benefits of the standard deduction are included in the existing wage withholding tables published in Pub.

Because nonresident aliens may not claim the standard deduction, employers are instructed to withhold an additional amount from a nonresident alien's wages. For the specific amounts to be added to wages before application of the wage tables, see Pub.

Note. A special rule applies to nonresident alien students from India and business apprentices from India who are eligible for the benefits of Article 21(2) of the United

What are the special Form

Nonresident aliens should pay particular attention to the following lines when completing Form

Step 1(b): Personal Information. You are required to enter a social security number (SSN) on Step 1(b) of Form

You can visit any SSA office or call the SSA at

For more information, go to www.ssa.gov/ssnumber.

Note. You cannot enter an individual taxpayer identification number (ITIN) in Step 1(b) of Form

Step 1(c): Personal Information. Check the Single or Married filing separately box regardless of your actual marital status.

Step 2: Multiple Jobs or Spouse Works. Do not complete this section unless you have more than one job at the same time. Do not account for your spouse's job because nonresident aliens may not file jointly.

If you have more than one job, you may complete Step 2(b) or Step 2(c).

If you chose Step 2(b), complete the Step 2(b) Multiple Jobs Worksheet for only one job and write “nonresident alien” or “NRA” below Step 4(c) for only one job.

If you have only two jobs, you may choose Step 2(c), check the box on both Forms

Nonresident aliens should not use the Tax Withholding Estimator.

Multiple withholding agents. If you are completing Form

Step 3: Claim Dependents. Only certain nonresident aliens should use Step 3. Nonresident aliens from Canada, Mexico, South Korea, or India may be able to claim the child tax credit or the credit for other dependents. See Pub. 519 and Pub. 972 for more information.

Nonresident aliens are generally not entitled to education credits. See Pub. 519 for more information.

Add the total credits that you may claim and enter the total in Step 3.

Step 4. Optional

Step 4(a). If you want tax withheld for other income this year that won't have withholding and the income is taxable in the United States, enter the amount of other income here. Do not include any income from any jobs or

Step 4(b). Nonresident alien itemized deductions and adjustments to income may be limited. See Pub. 519 for more information. If you expect to claim itemized deductions and/or adjustments to income (such as the student loan interest deduction), add your itemized deductions and adjustments to income and enter the amount in Step 4(b).

Step 4(c). Write “nonresident alien” or “NRA” in the space below Step 4(c). If you would like to have an additional amount withheld, enter the amount in Step 4(c).

Exempt from withholding. Do not claim that you are exempt from withholding in the space below Step 4(c) of Form

IRS.gov |

Catalog No. 54303E |

Document Specifics

| Fact Number | Description |

|---|---|

| 1 | IRS Notice 1392 is a supplemental form to the W-4 form. |

| 2 | It provides instructions for nonresident aliens when completing the W-4 form for employment in the United States. |

| 3 | This notice helps ensure that the correct amount of federal income tax is withheld from their wages. |

| 4 | Specific adjustments stated in IRS Notice 1392 must be made by nonresident aliens, such as not claiming exemption from withholding and requesting an additional withholding amount. |

| 5 | The form also directs individuals to the IRS Publication 519 for more detailed information on tax issues relevant to nonresident aliens. |

| 6 | Failure to follow the instructions in Notice 1392 can result in incorrect withholding, potentially leading to an unexpected tax bill or penalty at year-end. |

| 7 | The IRS updates the Notice 1392 periodically, so it is important for employers and employees to ensure they are using the most current version. |

Guide to Writing IRS Notice 1392

Filling out the IRS Notice 1392 form is an important process for individuals who need to comply with specific tax requirements. This form is crucial for ensuring that the right information is provided to the Internal Revenue Service (IRS), making the tax filing process smoother and helping to avoid potential issues. The steps to complete the form are straightforward, but it's essential to pay close attention to detail to ensure all information is accurate and complete. Below are the steps to fill out the form properly.

Steps for Filling Out the IRS Notice 1392 Form

- Begin by carefully reading through the entire form to understand the type of information required. This initial review will help in gathering all the necessary details before starting to fill it out.

- Enter your personal information, including your full name, address, Social Security Number (SSN), and the tax year the form pertains to. Ensure that this information is accurate to prevent any processing delays.

- Follow the instructions for each section closely. The IRS Notice 1392 form may include various sections that require detailed financial information. Fill in each section according to the instructions provided, consulting the guidelines if you're unsure about what to enter.

- If the form requires financial figures, double-check these amounts to ensure they are correct. Accuracy in reporting financial details is crucial for avoiding errors in your tax calculations.

- Review the form for any additional requirements, such as documentation that needs to be attached. Make sure to include all required attachments to avoid delays in processing.

- Before submitting the form, go through it once more to check for any errors or omissions. Correct any mistakes you find to ensure the information is complete and accurate.

- Sign and date the form in the designated area. Your signature is required to validate the information and confirm that you are providing truthful and accurate data.

- Finally, submit the form to the IRS using the submission instructions provided. Depending on the form, it may need to be mailed to a specific address or submitted online.

Following these steps carefully will help ensure that your IRS Notice 1392 form is filled out correctly and submitted properly. It's important to take your time and pay attention to detail, as providing accurate and complete information is essential for the IRS to process your form efficiently. If you have any questions or require assistance, consider seeking help from a tax professional or the IRS directly.

Understanding IRS Notice 1392

-

What is IRS Notice 1392?

IRS Notice 1392 is a document issued by the Internal Revenue Service (IRS) to provide guidance for nonresident aliens in completing their Form W-4, which is used to determine the amount of federal income tax to withhold from wages. This notice is tailored specifically for nonresident aliens to help ensure that the correct amount of tax is withheld from their earnings in the United States.

-

Who needs to follow IRS Notice 1392?

This notice is specifically designed for nonresident aliens working in the United States. If you are a foreign national and do not possess a green card or have not passed the Substantial Presence Test, and you are receiving wages subject to U.S. income tax withholding, then the guidelines in Notice 1392 are applicable to you.

-

How does IRS Notice 1392 affect the way Form W-4 is completed?

Notice 1392 modifies the standard instructions for completing Form W-4 for nonresident aliens in several ways. It may require nonresident aliens to make specific adjustments when filling out their W-4, such as not claiming exemption from withholding, requesting additional withholding, and specifying a nonstandard deduction amount or an additional specific dollar amount to be withheld. These adjustments are designed to help ensure that the amount of tax withheld accurately reflects their tax liability.

-

Are there specific lines on Form W-4 that are affected by Notice 1392?

Yes, certain lines on Form W-4 are directly impacted by the guidelines in IRS Notice 1392. Nonresident aliens may be instructed to fill out the form in a way that differs from the standard instructions, particularly regarding allowances, additional income, deductions, and extra withholding amounts. It is important for nonresident aliens to review Notice 1392 carefully to understand which parts of Form W-4 these instructions apply to.

-

What happens if a nonresident alien does not follow the guidelines in Notice 1392?

If a nonresident alien does not follow the guidelines provided in IRS Notice 1392, there could be several consequences. The most immediate is that their employer may withhold either too much or too little federal income tax from their wages. Overwithholding can lead to a larger refund than expected at tax time, but underwithholding can result in owing taxes when filing a return, along with potential penalties and interest for insufficient payments throughout the year.

-

Can a nonresident alien claim exemption from withholding on their Form W-4?

Under the instructions provided in IRS Notice 1392, nonresident aliens generally cannot claim exemption from withholding. Instead, they are required to meet specific conditions outlined in the form instructions, which are designed to ensure the appropriate amount of taxes are withheld. Making inaccurate claims on Form W-4 can lead to incorrect withholding amounts and potential tax liabilities.

-

Does IRS Notice 1392 apply to all types of income?

IRS Notice 1392 specifically addresses the withholding of federal income tax on wages earned by nonresident aliens in the United States. It does not apply to other types of income, such as interest, dividends, or rental income, which may be subject to different tax rules and withholding requirements. Nonresident aliens should seek guidance on other income types as needed to ensure compliance with all applicable tax laws.

-

Where can nonresident aliens find IRS Notice 1392?

Nonresident aliens can find IRS Notice 1392 on the official IRS website (www.irs.gov). It is available for download in PDF format. Additionally, employers who are aware of their employees' nonresident alien status may provide a copy of the notice or direct employees to where they can find the document. Tax professionals and preparers are also valuable resources for obtaining and understanding the requirements outlined in Notice 1392.

-

What should a nonresident alien do if they have incorrectly completed Form W-4 without following Notice 1392?

If a nonresident alien realizes that they have incorrectly completed their Form W-4 by not adhering to the guidelines in IRS Notice 1392, they should immediately fill out a new Form W-4 in accordance with the correct instructions and submit it to their employer. Correcting the form promptly can help avoid issues with under or over withholding as early as possible. For specific situations or complications, consulting with a tax professional is advisable to ensure compliance and address any potential tax liabilities.

Common mistakes

When it comes to handling IRS Notice 1392 forms, people often make mistakes that can be easily avoided. Understanding these common errors can help ensure that the process goes smoothly and without delay. Here are six frequent mistakes to watch out for:

- Not double-checking the Social Security Number (SSN): It's crucial to ensure that the SSN provided on the form matches the number issued by the Social Security Administration. A simple typo can lead to processing delays or errors in your tax records.

- Ignoring Supplemental Documents: Some people forget to attach required supplemental documents that verify their eligibility for the tax situation being reported. This oversight can lead to incomplete submissions, requiring additional follow-up.

- Omitting Dates: Dates are essential for the IRS to understand the timing of certain events or eligibility periods. Missing dates can make it difficult for the IRS to process the form accurately.

- Using Incorrect Forms: Occasionally, individuals may use outdated forms or the wrong version of the IRS Notice 1392, which can cause confusion and delays in the processing of their information.

- Illegible Handwriting: While it might seem old-fashioned, filling out the form by hand requires clear and legible handwriting to prevent misunderstandings or errors in data entry.

- Forgetting to Sign and Date: An unsigned or undated form is considered incomplete by the IRS. This oversight can halt the entire process until the form is properly signed and dated.

Avoiding these mistakes can lead to a smoother and more efficient process when dealing with IRS Notice 1392 forms. Always review your forms carefully before submission to minimize potential issues.

Documents used along the form

When dealing with tax-related matters, particularly those involving international aspects, it's essential to ensure that all necessary documents are prepared and filed correctly. For individuals navigating through their tax obligations, the IRS Notice 1392 is often just one piece of a larger puzzle. This notice is especially pertinent for nonresident aliens, helping them figure out their proper tax withholding rates. Alongside this notice, several other forms and documents frequently play critical roles in ensuring tax compliance and maximizing potential benefits.

- Form W-4: Employees use this form to tell employers how much tax to withhold from their paycheck. It's crucial for determining the correct amount of federal income tax to be withheld from your earnings.

- Form 1040-NR: This is the U.S. Nonresident Alien Income Tax Return. It's used by nonresident aliens to report their U.S. sourced income and figure out their tax liability.

- Form 8233: This form is for nonresident aliens to claim a tax treaty exemption from income tax withholding on compensation for independent and certain dependent personal services performed in the U.S.

- Form W-8BEN: Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding, is used by foreign individuals to report their nonresident status and claim any applicable benefits under a tax treaty.

- Form 1099: Various forms 1099 report income from self-employment earnings, dividends, interest, government payments, and more. They are essential for nonresident aliens to adequately report all types of income beyond wages.

- Form 8833: Treaty-Based Return Position Disclosure under Section 6114 or 7701(b). This form is used by taxpayers to disclose positions taken on a tax return that are based on a tax treaty, affecting resident or nonresident status and income treatment.

- Social Security Agreement Documents: These documents prove the arrangement between the U.S. and other countries to eliminate dual social security taxation for workers. They are crucial for nonresident aliens working in the U.S. under such agreements.

From ensuring appropriate tax withholding to maximizing treaty benefits, these documents collectively ensure compliance and facilitate the accurate reporting of income and taxes for nonresidents. Accurate completion and filing of these forms directly impact one's tax obligations and potential refunds. Therefore, grasping the significance and details of each document is a solid step toward managing tax liabilities effectively.

Similar forms

The IRS Notice 1392, which provides guidelines for nonresident aliens to follow when preparing their U.S. income tax returns, shares similarities with a number of other important documents. One such document is the Form 1040NR, U.S. Nonresident Alien Income Tax Return. The Form 1040NR is a detailed form that nonresident aliens use for filing their income tax. Similar to IRS Notice 1392, it outlines the tax responsibilities for nonresident aliens and provides a systematic approach to income reporting and tax calculation.

Form W-4, Employee's Withholding Certificate, is another document akin to IRS Notice 1392. Although primarily used by employees to inform employers about the amount of tax to withhold from their paycheck, Form W-4 shares the concept of tax duty awareness with IRS Notice 1392. Both documents serve the purpose of guiding individuals in managing their tax withholding to align with their tax liability accurately.

The Form 8233, Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual, also has characteristics in common with the IRS Notice 1392. This form enables nonresident aliens to claim exemption from withholding on income associated with personal services. Like the IRS Notice 1392, it aids nonresident aliens in navigating the complexities of U.S. tax law, specifically regarding income exemption criteria.

Similarly, the Form 1042-S, Foreign Person's U.S. Source Income Subject to Withholding, parallels the IRS Notice 1392 in its focus on nonresident aliens and their tax obligations. This form reports income paid to foreign persons, including nonresident aliens, that is subject to income tax withholding. It complements the IRS Notice 1392 by offering a detailed account of taxable income and withheld taxes, thereby aiding in tax compliance and reporting.

Publication 519, U.S. Tax Guide for Aliens, is another comprehensive guide akin to IRS Notice 1392. It offers extensive information on the U.S. tax treatment of nonresident and resident aliens. By covering filing status, available deductions, and credits, it serves a similar educational purpose as the IRS Notice 1392, helping nonresident aliens understand and fulfill their U.S. tax obligations.

The Form 8840, Closer Connection Exception Statement for Aliens, also shares similarities with the IRS Notice 1392. This form allows nonresident aliens to assert a closer connection to a foreign country than to the United States to avoid being treated as U.S. residents for tax purposes. Like IRS Notice 1392, Form 8840 is designed to assist nonresident aliens in navigating specific tax filing positions and exemptions.

Lastly, the Form 8843, Statement for Exempt Individuals and Individuals with a Medical Condition, is related to the IRS Notice 1392 as well. Form 8843 is filed by nonresident aliens who are claiming an exemption from the substantial presence test. Through this lens, both documents are geared towards helping nonresident aliens understand exemptions and compliance requirements within the realm of U.S. tax law.

Dos and Don'ts

Filling out IRS forms can sometimes feel daunting, given their importance in the tax filing process. The IRS Notice 1392, specifically, carries its own set of guidelines. Here are some dos and don'ts that can help guide you through the process efficiently and correctly.

Do:Read through the entire form before beginning to fill it out, to ensure you understand all requirements.

Use black or blue ink if you are filling out the form by hand, as these colors are standard for official documents.

Gather all necessary documentation related to your tax situation before you start, such as your Social Security card, tax statements, and records of wages.

Double-check your Social Security number for accuracy to avoid processing delays or issues with your tax records.

Follow the instructions for each section carefully to ensure that all information is filled out correctly.

Contact a tax advisor or the IRS directly if you have any questions or uncertainties about how to complete any part of the form.

Sign and date the form if required, as an unsigned form may be considered invalid.

Keep a copy of the completed form for your records, as you may need to refer to it in the future or in case of an audit.

Submit the form before the due date to avoid penalties for late filing.

Use secure methods when sending your form, whether mailing or submitting electronically, to protect your sensitive information.

Rush through the form without understanding each section; mistakes could lead to processing delays or audits.

Use correction fluid or tape on the form; if you make a mistake, it's better to start with a new form to ensure clarity and cleanliness.

Ignore IRS instructions or specific guidelines; doing so can result in errors in filing.

Guesstimate values or information; ensure all data you provide is accurate and verifiable.

Skip sections that apply to you; incomplete forms may be returned for correction, delaying your filing.

Assume you are ineligible for certain deductions or credits without thoroughly checking the criteria.

Forget to check for updates or changes in tax laws that could affect how you complete the form.

Furnish incorrect contact information, which could cause delays in receiving any necessary correspondence from the IRS.

Fail to review the completed form for potential errors or omissions before submitting.

Overlook the importance of seeking assistance if you're unsure about any aspect of your tax situation; professional guidance can be invaluable.

Tackling the IRS Notice 1392 form with these dos and don'ts in mind can help ensure a smoother tax filing process. Remember, careful preparation and attention to detail can significantly impact the accuracy and timeliness of your submission.

Misconceptions

The IRS Notice 1392, a document pertaining to the tax status of nonresident aliens and the rules for withholding, is often misunderstood. Misconceptions can lead to errors in tax filing and withholding practices. Below are five common misconceptions about the IRS Notice 1392, each clarified to enhance understanding and compliance.

- Misconception 1: Notice 1392 is only relevant for employers.

This is incorrect. While Notice 1392 is indeed a critical document for employers, as it guides them on how to correctly withhold taxes for nonresident alien employees, its relevance extends to the employees themselves. Nonresident aliens benefit from understanding the rules and their rights regarding tax withholding in the United States.

- Misconception 2: It applies to all nonresident aliens regardless of visa type.

In fact, the guidelines outlined in Notice 1392 are not universally applicable to all nonresident aliens. The tax treatment and withholding requirements can vary significantly based on the visa type and other factors such as a tax treaty between the United States and the individual's home country.

- Misconception 3: Completing a W-4 form according to Notice 1392 guarantees correct withholding.

This belief overlooks the importance of regular updates and reviews. Although following Notice 1392 instructions when completing a Form W-4 can help achieve correct initial withholding, changes in circumstances, such as adjustments in income, tax status, or applicable tax treaty benefits, necessitate updates to the W-4 form.

- Misconception 4: Notice 1392 is only applicable at the federal level.

While it's true that Notice 1392 primarily provides guidance for federal tax withholding, understanding its provisions can also benefit individuals and employers in navigating state tax obligations. Some states model their tax legislation on federal rules, and being aware of federal guidelines can provide insights into state-level requirements.

- Misconception 5: Every section of Notice 1392 must be understood in detail by employees.

While it's advantageous for nonresident alien employees to have a general understanding of the rules that affect their tax withholding, it's not necessary for them to grasp every detail of Notice 1392. Employers, especially those with experience or resources related to tax compliance, play a key role in interpreting and applying these rules correctly. Employees, however, should be informed enough to identify potential issues and communicate them to their employers.

Key takeaways

The IRS Notice 1392 is an important document for certain nonresident aliens in understanding and complying with U.S. tax withholding requirements. Here are key takeaways for individuals who need to fill out and use this form:

Understand Your Tax Status: Before using IRS Notice 1392, ensure you accurately determine your tax status as a nonresident alien. This status impacts your tax obligations and withholding rates.

Specific Instructions for Nonresident Aliens: Notice 1392 provides specialized instructions for nonresident aliens to help them properly complete their W-4 forms, ensuring the correct amount of tax is withheld from their pay.

Follow Form W-4 Guidelines: While completing Form W-4, refer to the specific lines and instructions mentioned in Notice 1392. This may vary from the general instructions provided to other taxpayers.

Withholding Allowances Restrictions: Nonresident aliens may face certain restrictions on claiming withholding allowances. IRS Notice 1392 outlines these limitations clearly.

Standard Deduction Generally Not Available: In most cases, nonresident aliens cannot claim the standard deduction. Notice 1392 highlights exceptions and provides guidance on how to navigate this during tax withholding.

Additional Withholding: Notice 1392 may instruct nonresident aliens to request additional withholding to cover their U.S. tax liability fully. This helps avoid owing taxes when filing their annual return.

State and Local Taxes: While focusing on federal tax obligations, nonresident aliens should not overlook state and local tax requirements. Notice 1392 does not cover these, so separate research and compliance are necessary.

Filing Status Considerations: IRS Notice 1392 guides nonresident aliens on choosing the correct filing status for IRS Form W-4, which affects their tax withholding rate.

Consult With a Tax Professional: If uncertainties or complex situations arise, consulting with a tax professional knowledgeable about nonresident alien tax issues is advisable. They can provide personalized advice based on your specific circumstances.

By carefully adhering to the guidelines in IRS Notice 1392, nonresident aliens can ensure they are compliant with U.S. tax laws, potentially preventing over- or under-withholding of taxes from their income.

Popular PDF Documents

IRS 5498 - It also assists in strategic tax planning, especially for individuals looking to minimize their tax liabilities.

Form 500 Instructions - Step-by-step instructions on how to apply for various business taxes and licenses in Georgia.