Get IRS 990-T Form

At the heart of tax compliance for tax-exempt organizations lies the IRS 990-T form, a document that is as crucial as it is comprehensive. Primarily, it's designed for organizations to report and pay taxes on unrelated business income, which is income not directly related to their exempt purpose. This form embodies the principle that even organizations benefiting from tax-exempt status must contribute their fair share for income generated through activities outside their core missions. The complexities of the 990-T stem from the varied nature of income that can be considered unrelated business taxable income (UBTI), alongside the differences in exempt organizations themselves, including charities, pensions, and educational institutions. Moreover, the importance of accurately completing this form cannot be overstated, as errors or omissions can lead to audits, penalties, and even the jeopardization of tax-exempt status. The form not only serves as a financial statement of sorts but also stands as a reflection of the organization's adherence to tax laws, shining a light on its fiscal responsibility and transparency towards the IRS and the public.

IRS 990-T Example

Form |

|

Exempt Organization Business Income Tax Return |

|

OMB No. |

||||||

|

|

|

|

|

||||||

|

|

|

|

(and proxy tax under section 6033(e)) |

|

|

|

2020 |

||

|

|

|

For calendar year 2020 or other tax year beginning |

, 2020, and ending |

, 20 |

|

||||

|

|

|

|

▶ Go to www.irs.gov/Form990T for instructions and the latest information. |

|

|

|

|

||

Department of the Treasury |

|

|

|

|

Open to Public Inspection |

|||||

▶ Do not enter SSN numbers on this form as it may be made public if your organization is a 501(c)(3). |

for 501(c)(3) |

|||||||||

Internal Revenue Service |

||||||||||

Organizations Only |

||||||||||

|

|

|

|

|

|

|||||

A Check box if |

|

|

Name of organization ( Check box if name changed and see instructions.) |

|

D Employer identification number |

|||||

address changed. |

|

|

|

|

|

|

||||

|

|

|

|

|||||||

B Exempt under section |

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

E Group exemption number |

|||||||

501( |

) ( |

) |

or |

|

|

|

|

(see instructions) |

||

Type |

|

|

|

|

||||||

|

|

|

|

|

|

|||||

408(e) |

|

220(e) |

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

|

||

408A |

|

530(a) |

|

|

|

|

|

|

|

|

|

|

|

|

|

F |

|

Check box if |

|||

529(a) |

|

529A |

C Book value of all assets at end of year . . . . |

. . . . . . ▶ |

|

|

|

an amended return. |

||

|

|

|

|

|

|

|

|

|

|

|

G |

Check organization type ▶ |

501(c) corporation |

501(c) trust |

401(a) trust |

Other trust |

Applicable reinsurance entity |

|

H |

Check if filing only to ▶ |

Claim credit from Form 8941 |

Claim a refund shown on Form 2439 |

|

|||

I |

Check if a 501(c)(3) organization filing a consolidated return with a 501(c)(2) titleholding corporation . |

. . . |

. . . . ▶ |

||||

J |

Enter the number of attached Schedules A (Form |

. . . . . . . . . . . |

. . . |

▶ |

|||

KDuring the tax year, was the corporation a subsidiary in an affiliated group or a

Yes

Yes

No If “Yes,” enter the name and identifying number of the parent corporation ▶

No If “Yes,” enter the name and identifying number of the parent corporation ▶

L The books are in care of ▶

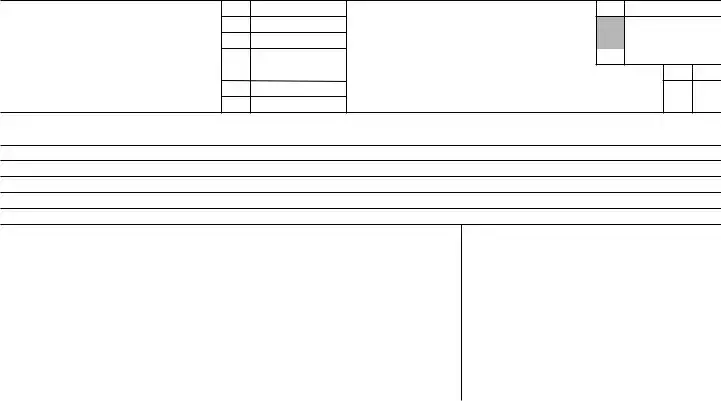

Part I Total Unrelated Business Taxable Income

1Total of unrelated business taxable income computed from all unrelated trades or businesses (see

|

instructions) |

2 |

Reserved |

3 |

Add lines 1 and 2 |

4 |

Charitable contributions (see instructions for limitation rules) |

5 |

Total unrelated business taxable income before net operating losses. Subtract line 4 from line 3 . . |

6 |

Deduction for net operating loss. See instructions |

7Total of unrelated business taxable income before specific deduction and section 199A deduction.

|

Subtract line 6 from line 5 |

8 |

Specific deduction (generally $1,000, but see instructions for exceptions) |

9 |

Trusts. Section 199A deduction. See instructions |

10 |

Total deductions. Add lines 8 and 9 |

11Unrelated business taxable income. Subtract line 10 from line 7. If line 10 is greater than line 7, enter zero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part II Tax Computation

1

2

3

4

5

6

7

8

9

10

11

1 Organizations taxable as corporations. Multiply Part I, line 11 by 21% (0.21) . . . . . . . ▶ |

1 |

2Trusts taxable at trust rates. See instructions for tax computation. Income tax on the amount on

|

Part I, line 11 from: |

Tax rate schedule or |

Schedule D (Form 1041) |

. . |

. |

▶ |

2 |

3 |

Proxy tax. See instructions |

. . . . . . . . . . . . . . |

. . |

. |

▶ |

3 |

|

4 |

Other tax amounts. See instructions |

4 |

|||||

5 |

Alternative minimum tax (trusts only) |

5 |

|||||

6 |

Tax on noncompliant facility income. See instructions |

6 |

|||||

7 |

Total. Add lines 3 through 6 to line 1 or 2, whichever applies |

7 |

|||||

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 11291J |

|

|

|

Form |

||

Form |

|

|

|

|

|

|

|

|

|

Page 2 |

||

Part III |

Tax and Payments |

|

|

|

|

|

|

|

|

|

|

|

1a |

Foreign tax credit (corporations attach Form 1118; trusts attach Form 1116) |

|

1a |

|

|

|

|

|||||

b |

Other credits (see instructions) |

|

1b |

|

|

|

|

|||||

c |

General business credit. Attach Form 3800 (see instructions) |

|

1c |

|

|

|

|

|||||

d |

Credit for prior year minimum tax (attach Form 8801 or 8827) |

|

1d |

|

|

|

|

|||||

e |

Total credits. Add lines 1a through 1d |

. . . . . . . |

|

1e |

||||||||

2 |

Subtract line 1e from Part II, line 7 |

. . . . . . . |

|

2 |

|

|||||||

3 |

Other taxes. Check if from: |

Form 4255 |

Form 8611 |

Form 8697 |

Form 8866 |

|

|

|||||

|

|

|

Other (attach statement) |

. . . . . . . |

|

3 |

|

|||||

4 |

Total tax. Add lines 2 and 3 (see instructions). |

Check if includes tax previously deferred under |

|

|

||||||||

|

section 1294. Enter tax amount here . . . . |

. . . . . . . . . ▶ |

|

|

|

. |

4 |

|

||||

5 |

2020 net 965 tax liability paid from Form |

5 |

|

|||||||||

6a |

Payments: A 2019 overpayment credited to 2020 |

|

6a |

|

|

|

|

|||||

b |

2020 estimated tax payments. Check if section 643(g) election applies ▶ |

|

6b |

|

|

|

|

|||||

c |

Tax deposited with Form 8868 |

|

6c |

|

|

|

|

|||||

d |

Foreign organizations: Tax paid or withheld at source (see instructions) . |

|

6d |

|

|

|

|

|||||

e |

Backup withholding (see instructions) |

|

6e |

|

|

|

|

|||||

f |

Credit for small employer health insurance premiums (attach Form 8941) . |

6f |

|

|

|

|

||||||

gOther credits, adjustments, and payments:  Form 2439

Form 2439

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 4136 |

|

Other |

|

Total ▶ 6g |

|

|

|

|

||||

|

|

|

|

|||||||||||

7 |

Total payments. Add lines 6a through 6g |

7 |

||||||||||||

8 |

Estimated tax penalty (see instructions). Check if Form 2220 is attached |

. . |

▶ |

|

8 |

|||||||||

9 |

Tax due. If line 7 is smaller than the total of lines 4, 5, and 8, enter amount owed . . |

. . |

. |

. ▶ |

9 |

|||||||||

10 |

Overpayment. If line 7 is larger than the total of lines 4, 5, and 8, enter amount overpaid |

. |

. |

. ▶ |

10 |

|||||||||

11 |

Enter the amount of line 10 you want: Credited to 2021 estimated tax ▶ |

|

|

|

Refunded ▶ |

11 |

||||||||

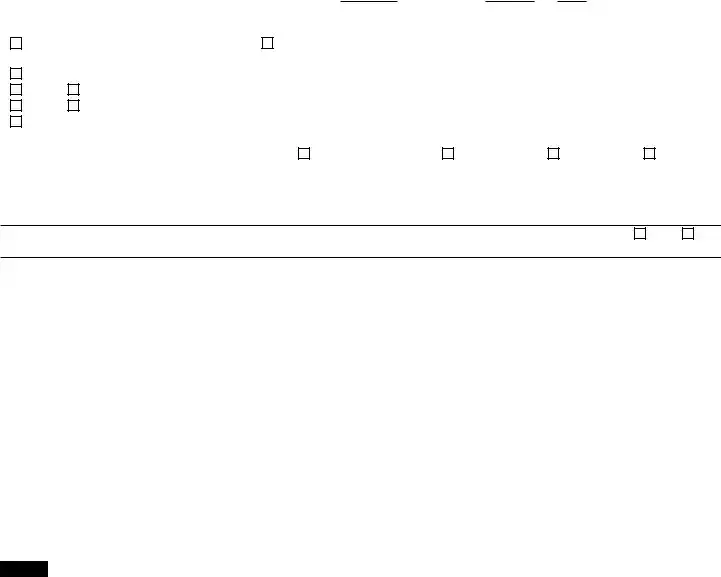

Part IV |

Statements Regarding Certain Activities and Other Information (see instructions) |

|

|

|||||||||||

1At any time during the 2020 calendar year, did the organization have an interest in or a signature or other authority over a financial account (bank, securities, or other) in a foreign country? If “Yes,” the organization may have to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts. If “Yes,” enter the name of the foreign country here ▶

2During the tax year, did the organization receive a distribution from, or was it the grantor of, or transferor to, a

foreign trust? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

If “Yes,” see instructions for other forms the organization may have to file. |

3 |

Enter the amount of |

4a |

Did the organization change its method of accounting? (see instructions) |

bIf 4a is “Yes,” has the organization described the change on Form 990,

Part V Supplemental Information

Yes No

Provide the explanation required by Part IV, line 4b. Also, provide any other additional information. See instructions.

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

▲ |

|

▲ |

|

|

May the IRS discuss this return |

||

|

|

|

with the preparer shown below |

||||

|

|

|

|

|

|

||

|

|

|

|

|

|

(see instructions)? |

Yes No |

|

Signature of officer |

Date |

|

Title |

|||

|

|

|

|

|

|||

Paid |

Print/Type preparer’s name |

Preparer’s signature |

Date |

Check |

if |

PTIN |

|

|

|

|

|||

|

|

|

|

|

||

Preparer |

|

|

|

|

||

|

|

|

|

|

|

|

Firm’s name ▶ |

|

|

Firm’s EIN ▶ |

|

|

|

Use Only |

|

|

|

|

|

|

Firm’s address ▶ |

|

|

Phone no. |

|

|

|

|

|

|

|

|

||

Form

Document Specifics

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS 990-T form is used by tax-exempt organizations to report their unrelated business income and calculate and pay income tax on that income. |

| Who Must File | Any tax-exempt organization that has $1,000 or more of gross income from an unrelated business must file Form 990-T. This includes charities, churches, and schools, among others. |

| Due Date | For organizations on a calendar year, the due date is the 15th day of the 5th month after the end of their tax year. For fiscal year filers, it is due the 15th day of the 5th month after their fiscal year ends. |

| Electronic Filing Requirement | As of the 2020 tax year, the IRS requires that Forms 990-T be filed electronically, except for certain exemptions specified by the agency. |

| Unrelated Business Income (UBI) | Unrelated Business Income refers to income from a trade or business, regularly carried on, that is not substantially related to the organization's exempt purpose or function. |

| Estimated Tax Payments | Organizations expecting to owe $500 or more in tax from unrelated business income must make estimated tax payments throughout the year. |

| State-Specific Forms | Some states require separate filings outside of the IRS 990-T for unrelated business income, and these requirements vary by state. Organizations should consult local laws. |

| Public Inspection | Generally, Form 990-T filings are open to public inspection, except for parts related to the trade secrets, patents, processes, or style of work. |

Guide to Writing IRS 990-T

Filling out the IRS 990-T form is an essential process for organizations seeking to report their unrelated business income. This form allows entities to calculate and report the tax owed on income that is not related to their exempt purposes. To ensure accuracy and compliance, follow these step-by-step instructions carefully. This concise guide aims to make the task more manageable, from gathering the necessary information to submitting the form.

- Begin by downloading the most current version of the IRS 990-T form directly from the IRS website. Verify that you have the correct tax year’s form.

- Complete the basic information section at the top of the form, including the legal name of the organization, address, Employer Identification Number (EIN), and the tax year for which you are filing.

- Read the instructions for each part of the form carefully. The IRS provides detailed guidelines that are essential for accurately completing the form.

- In Part I, calculate the gross income from all unrelated businesses. Each business activity must be reported separately.

- In Part II, deduct the allowed business deductions from your gross income to determine your unrelated business taxable income before net operating losses.

- Part III requires you to calculate and subtract any net operating loss deduction. This part is crucial for organizations that have experienced a loss in the previous tax years.

- If applicable, complete Part IV to calculate the tax owed on unrelated business taxable income. This section incorporates various credits and other taxes.

- Sign and date the form. An officer of the organization who is authorized to sign tax returns must sign the form. This ensures that the information provided is accurate and complete to the best of the signatory's knowledge.

- Review the entire form to ensure all necessary parts are completed and that all calculations are correct. Errors can delay processing or result in penalties.

- Submit the form to the IRS by the applicable deadline, which is typically the 15th day of the 5th month after the end of the organization’s tax year. The form can be filed electronically or mailed, depending on your preference and the specific requirements of the IRS for the year you are filing.

After the form is submitted, it's important to keep a copy for your records along with any documentation that supports the income, deductions, and credits claimed. This documentation is essential in case of an IRS audit. Always consult the IRS website or a tax professional if you have questions or require further assistance during the process.

Understanding IRS 990-T

-

What is the IRS 990-T form and who needs to file it?

The IRS 990-T form, known as the Exempt Organization Business Income Tax Return, is a document used by tax-exempt organizations, including charities, universities, and retirement plans, to report and pay income tax on unrelated business income. This form is required when a tax-exempt entity earns income from activities not substantially related to its tax-exempt purpose. If an organization generates more than $1,000 in gross income from a business unrelated to its exempt purposes, it must file a 990-T form in addition to any other required forms.

-

What qualifies as unrelated business income (UBI)?

Unrelated Business Income (UBI) is income from a trade or business, regularly carried on, that is not substantially related to the organization's exempt purpose or function, aside from the need for income. Examples of UBI include advertising sales in publications, rental income from debt-financed property, and merchandise sold that is unrelated to the organization’s exempt purposes. However, there are exceptions and modifications, including dividends, interest, certain types of rentals, and income from research, which are generally not considered UBI.

-

Are there any exceptions to filing the 990-T form?

Yes, several exceptions exist for filing the 990-T form. Organizations that typically do not need to file include those whose gross income from unrelated businesses is $1,000 or less, churches, and certain church-related organizations. Moreover, income from certain activities is not considered unrelated business income and, thus, does not require filing. These activities include volunteer labor, selling donated merchandise, and conducting bingo games, which meet specific legal definitions.

-

What are the deadlines for filing the 990-T form?

The 990-T form must be filed by tax-exempt organizations annually, by the 15th day of the 5th month after their accounting period ends. For organizations operating on a calendar year, the due date is May 15th of the following year. An organization can request an extension to file by submitting Form 8868, which grants an additional six months to file. It's important to adhere to these deadlines to avoid late filing penalties.

Common mistakes

Not understanding what constitutes unrelated business income (UBI). Many organizations mistakenly report income that is not considered UBI or overlook income that should be reported.

Failing to claim all permissible deductions. This includes direct and indirect expenses connected to generating unrelated business income, which can lower the taxable income.

Misinterpreting exceptions and modifications. Certain activities are not subject to unrelated business income tax (UBIT), and specific modifications can be applied to the gross income calculation.

Inaccurate calculation of estimated tax payments. If the organization expects to owe $500 or more in UBIT, estimated tax payments are required, and miscalculations can lead to underpayment penalties.

Omitting relevant schedules or attachments. The Form 990-T requires various schedules for different types of income, and failing to attach necessary information can lead to processing delays or questioning.

Incorrectly categorizing income. Income must be accurately classified according to the specific business activity to ensure correct tax treatment and rate application.

Overlooking state and local tax requirements. While Form 990-T is a federal form, many states have their own requirements for reporting unrelated business income, which can sometimes be overlooked.

Entering information on the wrong line or section. Due to the form's complexity, it's easy to place information in the incorrect section, which can affect the calculation of taxable income.

Averting these mistakes requires a diligent review process, a comprehensive understanding of tax laws regarding unrelated business income, and, when necessary, professional advice. Being meticulous and informed can help ensure that your organization complies with IRS requirements and avoids potential penalties.

Documents used along the form

When dealing with the IRS 990-T form, various other forms and documents commonly accompany it to ensure comprehensive compliance and reporting for tax-exempt organizations. These additional forms assist in detailing specific financial activities, tax deductions, credits, and income types that may affect the tax obligations of an organization. Understanding each document's purpose can significantly ease the preparation process, ensuring accuracy and completeness in filing.

- Schedule A (Form 990 or 990-EZ) - This form is essential for organizations to report their public charity status and public support. It helps in determining the classification of the organization and ensures the correct application of tax laws based on its public charity status.

- Schedule M (Form 990) - Used to report the types of non-cash contributions received by an organization over the tax year, Schedule M provides a detailed account of donations other than money, detailing their valuation and handling.

- Form 8822-B - This form is used to notify the IRS of a change in address or the identity of the responsible party. Keeping this information up to date is crucial for receiving timely communication from the IRS.

- Form 4562 - For organizations that need to report depreciation and amortization, Form 4562 details the expenses associated with the depreciation of assets and helps in calculating the allowable deductions over the assets' useful life.

- Form 2848 - Power of Attorney and Declaration of Representative, allows an individual, such as an accountant or attorney, to represent the organization in tax matters before the IRS, enabling them to make inquiries and receive information.

- Form 8868 - Organizations seeking an extension of time to file their IRS 990-T or other related forms can use Form 8868. This application is crucial for avoiding penalties for late submission.

- Form 1099 series - These forms report various types of income, including interest, dividends, and independent contractor payments. They are crucial for organizations to report income not related directly to charitable activities.

- Form 990 Schedule K (Form 990) - Specifically for organizations that hold tax-exempt bonds, this schedule provides details on the bonds issued, including the use of proceeds and compliance with tax regulations.

- Form 990-W - This worksheet helps organizations estimate the amount of tax they should withhold or pay for their unrelated business income, aiding in the planning of tax payments throughout the year.

- Form 1120-POL - For tax-exempt organizations that engage in political activities, this form is used to report political income and expenditures, crucial for maintaining transparency and compliance with tax laws regarding political involvement.

Understanding and utilizing these forms in conjunction with the IRS 990-T form is key to maintaining the tax-exempt status while ensuring full compliance with IRS regulations. Each document plays a vital role in the broader context of non-profit tax reporting and management. By staying informed and proactive in document preparation, organizations can navigate their financial and tax obligations more effectively, ultimately contributing to their mission's success and sustainability.

Similar forms

The IRS 990-PF form shares similarities with the 990-T, primarily because it's used by private foundations, including non-exempt charitable trusts treated as private foundations, to report their annual financial information. Similar to the 990-T, the 990-PF form has sections dedicated to reporting income, but it focuses more on charitable distributions and the assets held by the foundation. The reporting requirements aim to ensure transparency and compliance with IRS rules regarding charitable activities and financial management.

The IRS 1041 form is another document related to the 990-T, used by estates and trusts to report income. Like the 990-T, which is used by tax-exempt organizations to report unrelated business income, the 1041 form accounts for income that might be subject to taxation. Both forms serve to declare income that falls outside the typical tax-exempt status, though 1041 focuses on the taxation of trusts and estates specifically.

The Schedule K-1 (Form 1065) is closely related to the 990-T in that it is used to report income from pass-through entities, such as partnerships and S corporations, to the IRS. While the 990-T reports unrelated business income for tax-exempt organizations, the Schedule K-1 details each partner's share of the business’s income, deductions, and credits. Both forms play crucial roles in ensuring that income is reported accurately for tax purposes.

The IRS Form 1120 is the U.S. Corporation Income Tax Return, sharing a common goal with the 990-T of reporting income, losses, and dividends to the IRS. Though the 1120 form is used by taxable corporations and the 990-T by tax-exempt organizations reporting unrelated business income, both are critical for compliance with U.S. tax laws and ensure proper taxation based on reported income.

The IRS Form 8868 is an application for an extension of time to file an exempt organization return, including the 990-T. Organizations use this form when they need additional time to prepare their 990-T or other exempt organization returns. The similarity lies in the administrative aspect of managing tax reporting deadlines, ensuring organizations have adequate time to report their financial activities accurately.

The IRS Form 5500 is used by employer-sponsored benefit plans to report their financial condition, investments, and operations. While differing in specifics, both the 5500 and the 990-T require detailed financial reporting to the IRS. The 990-T focuses on unrelated business income for tax-exempt entities, whereas the 5500 concerns the transparency and accountability of pension and welfare benefit plans.

The IRS Form 990 is the standard form used by tax-exempt organizations to provide the public with financial information about their operations, somewhat similar to the 990-T, which also pertains to tax-exempt organizations but focuses specifically on reporting unrelated business income. Both forms ensure that these organizations maintain their tax-exempt status through transparent disclosure of their financial activities.

Lastly, the Schedule E (Form 1040) is used by taxpayers to report income or loss from rental property, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Like the 990-T, it deals with declaring specific types of income to the IRS, ensuring individuals and entities alike report income sources that may not be subject to standard income tax processes. The emphasis is on transparency and accuracy in reporting income that could impact taxation and compliance.

Dos and Don'ts

Filling out the IRS 990-T form, which is used by tax-exempt organizations to report unrelated business income, involves careful attention to detail and adherence to tax laws. Below are essential tips to guide you through the process, ensuring accuracy and compliance.

Things You Should Do

- Ensure accurate reporting by thoroughly reviewing the organization's financial records before filling out the form. This step is crucial for providing correct information about income, deductions, and taxable amounts.

- Utilize the IRS instructions for Form 990-T to guide you in filling out the form accurately. These instructions are designed to help taxpayers understand the requirements and how to correctly complete the form.

- Report all sources of unrelated business income. It is important to disclose all the income generated from activities not directly related to the organization’s tax-exempt purpose.

- Take advantage of relevant deductions and credits to lower the taxable income. Organizations are allowed to deduct expenses associated with generating unrelated business income, which can reduce the overall tax liability.

- Consider electronic filing for faster processing and confirmation of receipt. The IRS encourages electronic filing as it is more efficient and secure.

- Seek professional advice if you are unsure about any aspect of the form. Tax professionals can provide valuable guidance and help avoid common mistakes.

Things You Shouldn't Do

- Do not overlook the importance of deadlines. Filing the IRS 990-T form after the due date can result in penalties and interest charges.

- Avoid guesswork. Make sure that all the information you provide on the form is based on accurate financial records and calculations.

- Do not leave required fields blank. If a particular section does not apply, it is better to write “N/A” (not applicable) than to leave it empty, to show that you did not overlook the question.

- Refrain from mixing unrelated business income with exempt-function income. Keeping these incomes separate is crucial for correct reporting and tax calculation.

- Do not ignore IRS notices or letters about your Form 990-T filing. If the IRS contacts you for more information or clarification, respond promptly to avoid further issues.

- Avoid the temptation to underreport income to reduce tax liability. Such practices can lead to audits, penalties, and legal issues.

Misconceptions

The IRS Form 990-T is a document that many find confusing, leading to a variety of misconceptions about its purpose, who needs to file it, and the information it requires. Here's a list of common misunderstandings:

Only nonprofit organizations need to file the 990-T. While it's true that tax-exempt organizations use this form to report their unrelated business income, other entities, such as trusts, can also be required to file if they have gross income of $1,000 or more from a trade or business unrelated to their exempt function.

Filing a 990-T means an organization is engaging in inappropriate activities for a tax-exempt entity. This is not accurate. Tax-exempt organizations are allowed to engage in some amount of unrelated business; however, they must report and possibly pay tax on the income from these activities. Filing Form 990-T is a compliance requirement, not an admission of wrongdoing.

Organizations only report taxable income on the 990-T. In reality, organizations must report their gross income from unrelated businesses before deductions. This includes all income, not just the income that exceeds expenses and is considered taxable.

All income from activities not related to an organization's exempt purpose is automatically unrelated business income (UBI). Certain types of income, such as dividends, interest, and certain rents and royalties, are generally excluded from UBI, even if they come from activities unrelated to the organization's exempt purpose.

You can file the 990-T anytime during the year. Like individual and corporate tax returns, the 990-T has a specific filing deadline. It's typically due on the 15th day of the 5th month after the end of the organization's fiscal year. Extensions can be requested, but there is a set timeline for filing.

If an organization has unrelated business losses, there's no need to file the 990-T. Even if an organization expects its unrelated business activities to result in a loss, it still must file Form 990-T to report the loss. These losses might carry over to future years and offset future unrelated business income.

Organizations can wait to file 990-T until they pay their taxes. The filing deadline for Form 990-T generally precedes the date by which any payment due must be made. Therefore, waiting until taxes are paid to file could result in late filing penalties.

The 990-T is a public document. Unlike the Form 990 or 990-EZ, which are widely available to the public to provide transparency about the operations of nonprofit organizations, the 990-T, although submitted to the IRS by tax-exempt entities, is not publically disclosed in the same manner due to the sensitive business income details it contains.

Key takeaways

The IRS 990-T form is an essential document for certain tax-exempt organizations, trusts, and estates, detailing taxable income from unrelated business activities. Understanding the nuances of this form can ensure compliance and optimize tax responsibilities. Below are key takeaways for successfully filling out and using the IRS 990-T form:

- Educate Yourself on What Constitutes Unrelated Business Income (UBI): It's critical to understand which incomes are considered unrelated business income. Generally, UBI is income from a trade or business, regularly carried on, that is not substantially related to the organization's exempt purpose, other than through the generation of funds.

- Determine if Your Organization is Required to File: Not all tax-exempt entities are required to file the 990-T. Filing is necessary if the organization grosses $1,000 or more from an unrelated business activity during the tax year.

- Identify Available Deductions: Organizations can claim deductions for expenses, depreciation, and similar items directly connected to the unrelated business income. This may significantly reduce the taxable amount.

- Accurately Report Each Unrelated Business Activity Separately: The IRS requires the separate reporting of each unrelated business activity. This distinction helps ensure the correct application of the tax code to each activity.

- Be Aware of Filing Deadlines: Deadlines for filing the 990-T form vary depending on the organization's tax year. Generally, the form must be filed by the 15th day of the 5th month after the end of the organization's fiscal year. Extensions are available, but they must be filed on time.

- Consider State Filing Requirements: In addition to federal filing, some states may require tax-exempt organizations to file forms related to unrelated business taxable income. It's essential to verify and comply with any state-specific requirements.

Approaching the IRS 990-T with a comprehensive understanding of these aspects ensures that organizations fulfill their tax obligations without overlooking potential benefits associated with the law's provisions. For additional guidance, consulting with a tax professional knowledgeable about nonprofit tax issues is advisable.

Popular PDF Documents

Irs Power of Attorney - Form M-2848 can be critical during audits, enabling the appointed representative to interact with the IRS, request documents, and respond to inquiries on the taxpayer’s behalf.

Can I Stop Paying Sss After 10 Years - This document doubles as the official receipt when it is validated, serving as proof of payment.

Ohio Declaration of Tax Representative - This form is used when you want to appoint a representative to deal with the tax department on your behalf.