Get IRS 941 Form

Staying on top of tax obligations represents a significant aspect of managing a business in the United States, and one cannot overlook the importance of the IRS 941 form in this realm. This form, central to payroll tax compliance, serves as a quarterly report that businesses must file to detail the taxes they have withheld from their employees' wages. It encompasses federal income tax, Social Security, and Medicare taxes, ensuring that employers are contributing to their employees' future security and healthcare. Not only does the IRS use it to verify the accuracy of the tax amounts withheld, but it also plays a pivotal role in maintaining the financial integrity of the Social Security and Medicare programs by guaranteeing timely and accurate funding. The process of completing this form requires meticulous attention to detail and an understanding of the current tax obligations, highlighting the form's complexity and the potential consequences of errors. The significance of the IRS 941 form in facilitating a smooth relationship between employers, employees, and the federal tax system underscores its role as a cornerstone of fair and efficient tax administration.

IRS 941 Example

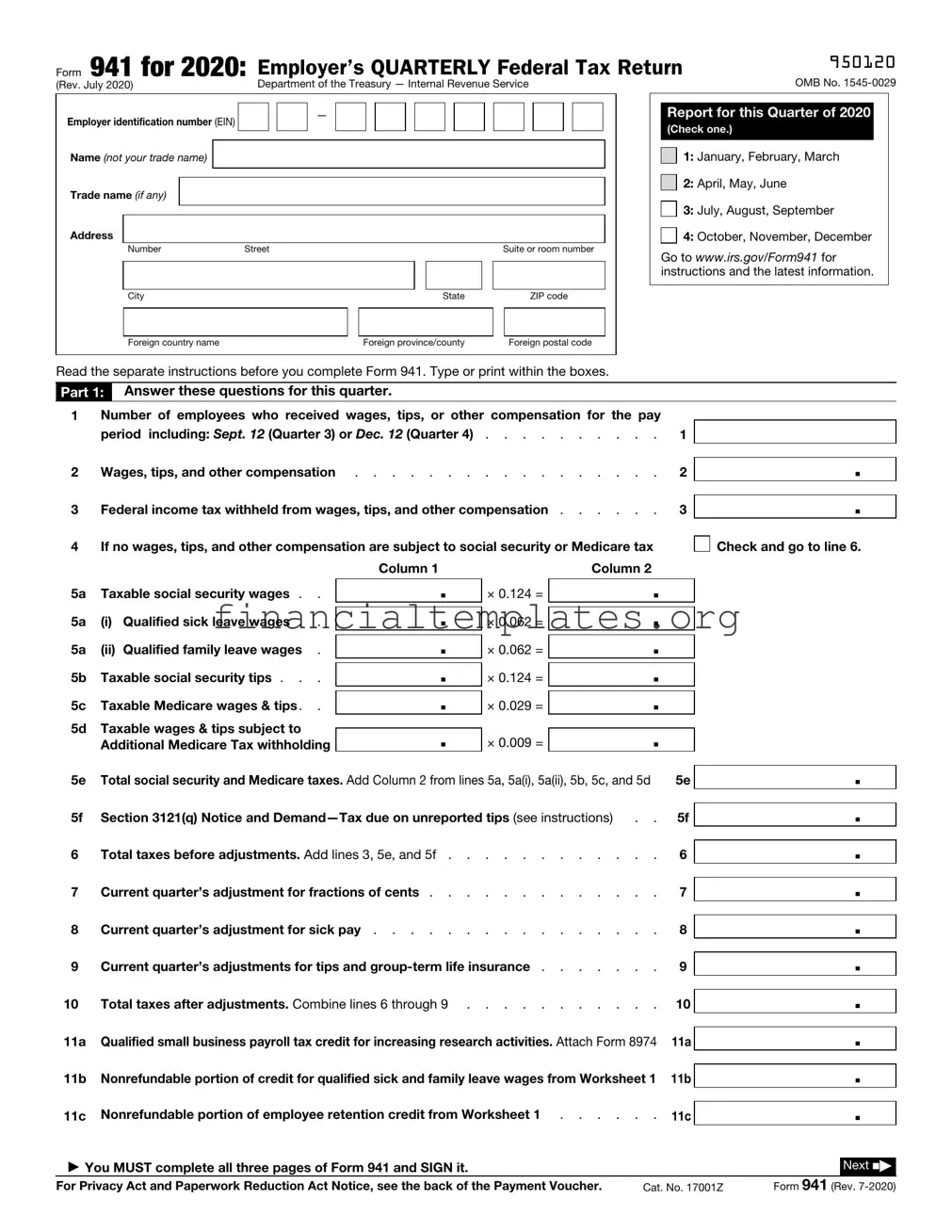

Form 941 for 2020: |

Employer’s QUARTERLY Federal Tax Return |

950120 |

|

|

|

(Rev. July 2020) |

Department of the Treasury — Internal Revenue Service |

OMB No. |

Employer identification number (EIN) |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Number |

Street |

|

|

|

|

|

Suite or room number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

|

ZIP code |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

Foreign country name |

|

|

Foreign province/county |

|

|

Foreign postal code |

||

Report for this Quarter of 2020

(Check one.)

1: January, February, March

1: January, February, March

2: April, May, June

2: April, May, June

3: July, August, September

4: October, November, December

Go to www.irs.gov/Form941 for instructions and the latest information.

Read the separate instructions before you complete Form 941. Type or print within the boxes.

Part 1: Answer these questions for this quarter.

1Number of employees who received wages, tips, or other compensation for the pay period including: Sept. 12 (Quarter 3) or Dec. 12 (Quarter 4) . . . . . . . . . . 1

2 |

Wages, tips, and other compensation |

. |

2 |

|||||

3 |

Federal income tax withheld from wages, tips, and other compensation |

. |

3 |

|||||

4 |

If no wages, tips, and other compensation are subject to social security or Medicare tax |

|

||||||

|

|

Column 1 |

|

Column 2 |

|

|||

5a |

Taxable social security wages . . |

|

. |

× 0.124 = |

. |

|

||

|

|

|

|

|

|

|

. |

|

5a |

(i) |

Qualified sick leave wages . . |

|

. |

× 0.062 = |

|

|

|

|

|

|

|

|

|

|

. |

|

5a |

(ii) |

Qualified family leave wages . |

|

. |

× 0.062 = |

|

|

|

|

|

|

|

|

|

. |

|

|

5b |

Taxable social security tips . . . |

|

. |

× 0.124 = |

|

|

||

|

|

|

|

|

|

. |

|

|

5c |

Taxable Medicare wages & tips. . |

|

. |

× 0.029 = |

|

|

||

5d |

Taxable wages & tips subject to |

|

|

|

|

|

|

|

|

. |

× 0.009 = |

|

. |

|

|||

|

Additional Medicare Tax withholding |

|

|

|

||||

5e |

Total social security and Medicare taxes. Add Column 2 from lines 5a, 5a(i), 5a(ii), 5b, 5c, and 5d |

|

5e |

|||||

5f |

Section 3121(q) Notice and |

. |

5f |

|||||

6 |

Total taxes before adjustments. Add lines 3, 5e, and 5f |

. |

6 |

|||||

7 |

Current quarter’s adjustment for fractions of cents |

. |

7 |

|||||

8 |

Current quarter’s adjustment for sick pay |

. |

8 |

|||||

9 |

Current quarter’s adjustments for tips and |

. |

9 |

|||||

10 |

Total taxes after adjustments. Combine lines 6 through 9 |

. |

10 |

|||||

11a |

Qualified small business payroll tax credit for increasing research activities. Attach Form 8974 |

11a |

||||||

11b |

Nonrefundable portion of credit for qualified sick and family leave wages from Worksheet 1 |

11b |

||||||

11c |

Nonrefundable portion of employee retention credit from Worksheet 1 |

. |

11c |

|||||

▶You MUST complete all three pages of Form 941 and SIGN it.

.

.

Check and go to line 6.

Check and go to line 6.

.

.

.

.

.

.

.

.

.

.

Next ■▶

For Privacy Act and Paperwork Reduction Act Notice, see the back of the Payment Voucher. |

Cat. No. 17001Z |

Form 941 (Rev. |

950220

Name (not your trade name) |

Employer identification number (EIN) |

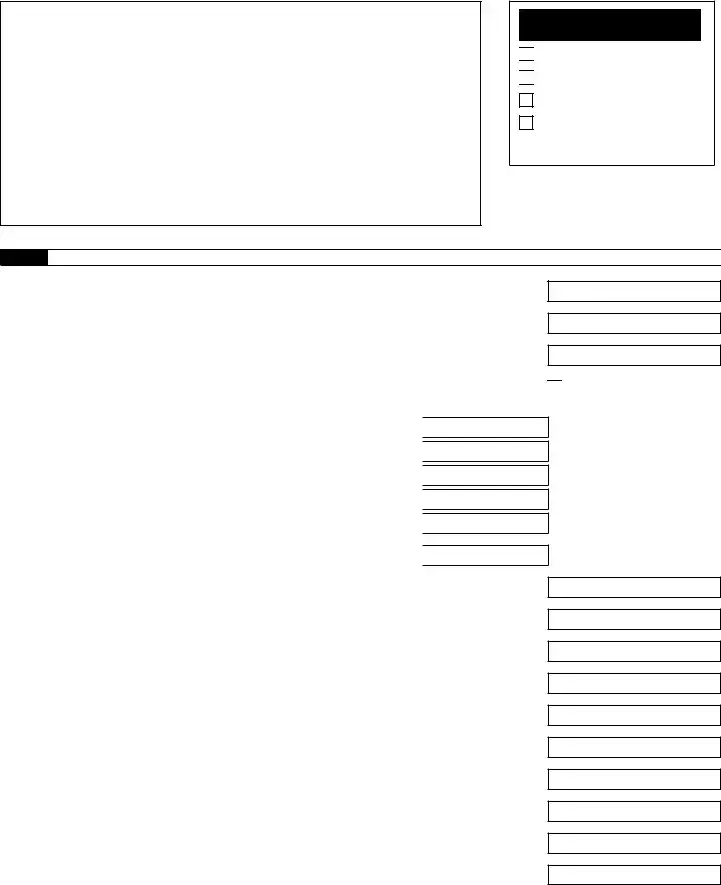

Part 1: Answer these questions for this quarter. (continued)

11d |

Total nonrefundable credits. Add lines 11a, 11b, and 11c |

11d |

12 |

Total taxes after adjustments and nonrefundable credits. Subtract line 11d from line 10 . |

12 |

13a |

Total deposits for this quarter, including overpayment applied from a prior quarter and |

13a |

|

overpayments applied from Form |

|

13b |

Deferred amount of social security tax |

13b |

13c |

Refundable portion of credit for qualified sick and family leave wages from Worksheet 1 |

13c |

13d |

Refundable portion of employee retention credit from Worksheet 1 |

13d |

13e |

Total deposits, deferrals, and refundable credits. Add lines 13a, 13b, 13c, and 13d . . . |

13e |

13f |

Total advances received from filing Form(s) 7200 for the quarter |

13f |

13g |

Total deposits, deferrals, and refundable credits less advances. Subtract line 13f from line 13e . |

13g |

14Balance due. If line 12 is more than line 13g, enter the difference and see instructions . . . 14

|

|

|

|

|

15 |

Overpayment. If line 13g is more than line 12, enter the difference |

|

. |

Check one: |

.

.

.

.

.

.

.

.

.

.

Apply to next return. |

|

Send a refund. |

Part 2: Tell us about your deposit schedule and tax liability for this quarter.

If you’re unsure about whether you’re a monthly schedule depositor or a semiweekly schedule depositor, see section 11 of Pub. 15.

16 Check one:

Line 12 on this return is less than $2,500 or line 12 on the return for the prior quarter was less than $2,500, and you didn’t incur a $100,000

You were a monthly schedule depositor for the entire quarter. Enter your tax liability for each month and total

liability for the quarter, then go to Part 3.

|

|

|

|

Tax liability: Month 1 |

|

. |

|

|

|

|

|

Month 2 |

|

. |

|

|

|

|

|

Month 3 |

|

. |

|

|

|

|

|

Total liability for quarter |

|

. |

Total must equal line 12. |

You were a semiweekly schedule depositor for any part of this quarter. Complete Schedule B (Form 941),

Report of Tax Liability for Semiweekly Schedule Depositors, and attach it to Form 941. Go to Part 3.

▶ You MUST complete all three pages of Form 941 and SIGN it. |

|

Next |

■ |

▶ |

|

|

|

||

Page 2 |

Form 941 (Rev. |

|||

952920

Name (not your trade name)

Employer identification number (EIN)

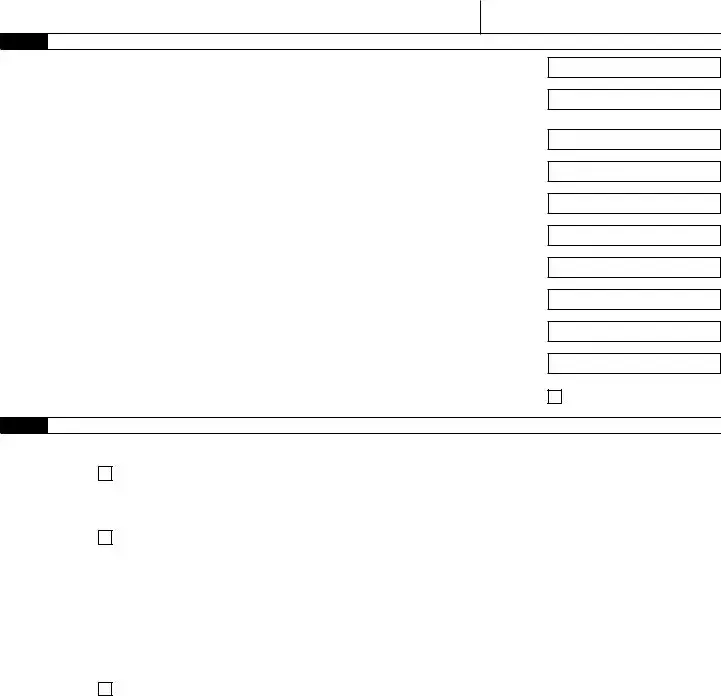

Part 3: Tell us about your business. If a question does NOT apply to your business, leave it blank.

17 If your business has closed or you stopped paying wages . . . . . . . . . . . . . . .

Check here, and

enter the final date you paid wages

/ /

; also attach a statement to your return. See instructions.

18 If you’re a seasonal employer and you don’t have to file a return for every quarter of the year . . .

Check here.

19 |

Qualified health plan expenses allocable to qualified sick leave wages |

19 |

20 |

Qualified health plan expenses allocable to qualified family leave wages |

20 |

21 |

Qualified wages for the employee retention credit |

21 |

22 |

Qualified health plan expenses allocable to wages reported on line 21 |

22 |

23 |

Credit from Form |

23 |

.

.

.

.

.

24 Deferred amount of the employee share of social security tax included on line 13b . . . 24

.

|

|

|

25 |

Reserved for future use . . . . . . . . . . . . . . . . . . . . . . 25 |

. |

Part 4: May we speak with your

Do you want to allow an employee, a paid tax preparer, or another person to discuss this return with the IRS? See the instructions

for details.

Yes. Designee’s name and phone number

Yes. Designee’s name and phone number

Select a

No.

Part 5: Sign here. You MUST complete all three pages of Form 941 and SIGN it.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

✗Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Address

City

State

Check if you’re

PTIN |

|

|

|

|

|

|

|

Date |

/ |

/ |

|

EIN |

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

ZIP code

Page 3 |

Form 941 (Rev. |

951020

This page intentionally left blank

Form

Purpose of Form

Complete Form

Making Payments With Form 941

To avoid a penalty, make your payment with Form 941 only if:

•Your total taxes after adjustments and nonrefundable credits (Form 941, line 12) for either the current quarter or the preceding quarter are less than $2,500, you didn’t incur a $100,000

•You’re a monthly schedule depositor making a payment in accordance with the Accuracy of Deposits Rule. See section 11 of Pub. 15 for details. In this case, the amount of your payment may be $2,500 or more.

Otherwise, you must make deposits by electronic funds transfer. See section 11 of Pub. 15 for deposit instructions. Don’t use Form

▲! Use Form

CAUTION Form 941 that should’ve been deposited, you may be subject to a penalty. See Deposit Penalties in section 11 of Pub. 15.

Specific Instructions

Box

Box

Box

Box

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your

EIN, “Form 941,” and the tax period (“1st Quarter 2020,” “2nd Quarter 2020,” “3rd Quarter 2020,” or “4th Quarter 2020”) on your check or money order. Don’t send cash.

Don’t staple Form

•Detach Form

and Form 941 to the address in the Instructions for Form 941.

Note: You must also complete the entity information above Part 1 on Form 941.

|

✁ |

▼ |

Detach Here and Mail With Your Payment and Form 941. |

▼ |

|

✃ |

||||||

|

|

|

|

|

|

|

|

|

|

|||

Form |

|

|

|

|

|

Payment Voucher |

|

OMB No. |

||||

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

Department of the Treasury |

|

|

|

▶ Don’t staple this voucher or your payment to Form 941. |

|

2020 |

|||||

|

Internal Revenue Service |

|

|

|

|

|||||||

|

1 Enter your employer identification |

|

2 |

|

|

Dollars |

|

Cents |

||||

|

|

number (EIN). |

|

|

|

|

|

Enter the amount of your payment. ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Make your check or money order payable to “United States Treasury” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Tax Period |

|

|

|

|

4 Enter your business name (individual name if sole proprietor). |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1st |

|

|

3rd |

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter your address. |

|

|

|

|||

|

|

Quarter |

|

|

Quarter |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||||

|

|

2nd |

|

|

4th |

|

|

|

||||

|

|

|

|

|

|

Enter your city, state, and ZIP code; or your city, foreign country name, foreign province/county, and foreign postal code. |

||||||

|

|

Quarter |

|

|

Quarter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 941 (Rev.

Privacy Act and Paperwork Reduction Act Notice. We ask for the information on Form 941 to carry out the Internal Revenue laws of the United States. We need it to figure and collect the right amount of tax. Subtitle C, Employment Taxes, of the Internal Revenue Code imposes employment taxes on wages and provides for income tax withholding. Form 941 is used to determine the amount of taxes that you owe. Section 6011 requires you to provide the requested information if the tax is applicable to you. Section 6109 requires you to provide your identification number. If you fail to provide this information in a timely manner, or provide false or fraudulent information, you may be subject to penalties.

You’re not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books and records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law.

Generally, tax returns and return information are confidential, as required by section 6103. However, section 6103 allows or requires the IRS to disclose or give the information shown on your tax return to others as described in the Code. For example, we may disclose your tax information to the Department of

Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

The time needed to complete and file Form 941 will vary depending on individual circumstances. The estimated average time is:

Recordkeeping . . . . . . . . . . 20 hr., 19 min.

Learning about the law or the form . . |

. . 53 min. |

Preparing, copying, assembling, and |

|

sending the form to the IRS |

1 hr., 16 min. |

If you have comments concerning the accuracy of these time estimates or suggestions for making Form 941 simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/FormComments. Or you can send your comments to Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

Document Specifics

| Fact Name | Description |

|---|---|

| Purpose of Form 941 | Used by employers to report quarterly federal tax withholding, Social Security, and Medicare taxes. |

| Filing Frequency | Form 941 is filed four times a year, aligning with the end of each quarter. |

| Employer Requirement | All employers who withhold income taxes, Social Security tax, or Medicare tax must file Form 941. |

| Due Dates | The form is due by the last day of the month following the end of a quarter. |

| Governing Law | Federal law governs the Form 941, specifically under the Internal Revenue Code. |

Guide to Writing IRS 941

Filling out the IRS 941 form, a crucial step for many employers, requires careful attention to detail and accuracy. This form is used by employers to report quarterly federal tax returns, including withheld income tax, and the employer and employee's share of Social Security and Medicare taxes. Ensure all the information is correct and up-to-date to avoid potential issues with the IRS. Follow these steps meticulously to complete the form properly.

- Gather necessary information including your Employer Identification Number (EIN), the total number of employees, and the total pay for the quarter.

- Enter your business information at the top of the form, including the EIN, the name, and the address of your business.

- Fill in the reporting period at the top of the form, indicating which quarter of the year you're reporting for.

- On line 1, enter the number of employees who received wages, tips, or other compensation for the pay period.

- On line 2, enter the total wages, tips, and other compensation paid to employees during the quarter.

- Calculate the federal income tax withheld from the employees' wages, tips, etc., and enter this amount on line 3.

- On lines 5a through 5d, calculate the taxable Social Security and Medicare wages and tips, and enter the amounts. Make sure to follow the form's instructions to multiply the wages by the current rate provided for both the employer and employee portions.

- If applicable, fill in lines 6 and 7 for any adjustments for tips and group-term life insurance.

- Sum up the totals for lines 3, 5a, 5b, 5c, 5d, 6, and 7 to calculate your total taxes before adjustments, and enter this on line 10.

- Complete any applicable adjustments on lines 11 through 13.

- Add the total deposits made during the quarter, including overpayments applied from a prior quarter, and enter this on line 14.

- If applicable, fill out the section for the Qualified Small Business Payroll Tax Credit for Increasing Research Activities.

- Calculate any balance due or overpayment, and enter the amount on lines 15 and 16.

- Sign and date the form. If you're a paid preparer, also complete the 'Paid Preparer Use Only' section.

- Double-check all entries for accuracy and completeness before mailing the form to the IRS or filing electronically.

Accurately completing and submitting the IRS 941 form is essential for compliance with federal tax regulations. By following these outlined steps, employers can ensure they meet their responsibilities and provide the necessary information to the IRS. Careful preparation and understanding of the form's requirements can minimize errors and potential complications with tax filings.

Understanding IRS 941

-

What is the IRS 941 form?

The IRS 941 form, also known as the Employer's Quarterly Federal Tax Return, is a document that employers must file on a quarterly basis. It's used to report income taxes, social security tax, or Medicare tax withheld from employee's paychecks. Additionally, it reports the employer's portion of social security or Medicare tax. This form plays a critical role in ensuring that employees' tax withholdings are correctly reported to the IRS.

-

Who needs to file the IRS 941 form?

Most employers operating a business and employing workers who receive wages subject to federal income tax withholding, social security, and Medicare taxes must file the IRS 941 form. However, there are exceptions. For instance, employers of agricultural workers or household employees do not use this form but instead may use forms 943 or 1040, Schedule H, respectively. To confirm if your business needs to file this form, it's advisable to refer to the IRS guidelines or consult a tax professional.

-

When are the due dates for filing the IRS 941 form?

The IRS 941 form must be filed four times a year. The due dates are as follows:

- April 30, for the first quarter (January 1 - March 31)

- July 31, for the second quarter (April 1 - June 30)

- October 31, for the third quarter (July 1 - September 30)

- January 31, for the fourth quarter (October 1 - December 31)

If the due date falls on a weekend or legal holiday, the deadline is the next business day.

-

How can one file the IRS 941 form?

Employers have the option to file the IRS 941 form electronically or on paper. The IRS encourages electronic filing for its efficiency and convenience. To e-file, employers can use an IRS-authorized e-file provider. Alternatively, they can choose to complete a paper form and mail it to the specified address provided by the IRS. Regardless of the method chosen, it's crucial to ensure that the form is filed accurately and on time to avoid penalties.

Common mistakes

Not filing on time: Failing to submit the 941 form by the deadline can lead to penalties. The IRS is strict about deadlines, and even a day late can be costly.

Incorrect Employer Identification Number (EIN): Using the wrong EIN can cause significant delays. The IRS uses this number to track your business's tax filings.

Math errors: Simple mistakes in addition or subtraction can throw off your entire tax calculation. Always double-check your math.

Forgetting to sign the form: An unsigned 941 form is considered incomplete. Remember, a physical signature is required for paper filings.

Not filling in all required lines: Every line of the 941 form should be completed. Missing information can lead to processing delays and possible follow-up from the IRS.

Misclassifying workers: Incorrectly classifying employees as independent contractors or vice versa can affect your tax liabilities.

Overlooking the COBRA premium assistance payments: Not considering these payments can lead to inaccuracies in your reported tax credits.

Incorrect tax period: Make sure you indicate the correct quarter for which you are filing. It's an easy detail to overlook but crucial for correct processing.

Using the wrong form version: The IRS updates forms periodically. Ensure you are using the most recent version of the 941 form.

Neglecting to report adjustments: If you discover a mistake after submitting a previous quarter's 941 form, you need to report these adjustments properly in the following quarter. Failing to do so can cause discrepancies.

To ensure accuracy:

Always double-check your work and compare it to your payroll records.

Use IRS tools and resources, which can help clarify instructions and common questions.

Consider using payroll software that automatically fills out the 941 for you based on the payroll information you enter throughout the quarter.

If you're unsure about something, don't hesitate to consult with a tax professional. It's better to seek help than to guess and make a mistake.

In summary, attention to detail and thoroughness are your best defenses against common mistakes on the IRS 941 form. A proactive approach to gathering and checking your information can save you from headaches down the road.

Documents used along the form

When businesses navigate their way through tax forms, the IRS 941 form, which is used to report quarterly federal tax returns, often needs the support of additional documents for a smoother and more accurate process. These forms work in conjunction to ensure employers are compliant with tax reporting and payment obligations. Understanding these supplementary documents can greatly alleviate the stress of tax season for employers and their accounting teams.

- Form W-2: This document is essential for employers as it reports an employee's annual wages and the amount of taxes withheld from their paycheck. It provides the information needed to complete Form 941 and must be sent to employees and the Social Security Administration at the end of each year.

- Form W-3: The Transmittal of Wage and Tax Statements works alongside Form W-2. It is a summary form sent to the Social Security Administration, accompanying Form W-2, to report the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the previous year.

- Form W-4: This form is filled out by employees to inform employers of their withholding allowances. Employers use this form to determine the correct amount of federal income tax to withhold from employees’ paychecks, affecting the amounts reported on Form 941.

- Form 940: This form is the Employer's Annual Federal Unemployment (FUTA) Tax Return. It calculates and reports the employer's federal unemployment tax liability. While it focuses on unemployment tax, rather than income tax withholding, it is an important part of overall tax compliance and complements the information submitted through Form 941.

Collectively, these forms create a framework that supports employers in fulfilling their tax reporting duties accurately and efficiently. By leveraging these documents alongside the IRS 941 form, businesses can better navigate the complexities of payroll tax reporting, ensuring that they meet federal requirements and contribute to the overall financial health and compliance of their operations.

Similar forms

The IRS 941 form, known as the Employer's Quarterly Federal Tax Return, is intricately tied to several other documents within the realm of payroll and tax reporting. Among these is the IRS 940 form, or the Employer's Annual Federal Unemployment (FUTA) Tax Return. While the 941 form deals with reporting wages, tips, and other compensation paid to an employee, along with withholding income, Social Security, and Medicare taxes each quarter, the 940 form focuses on the employer's annual report of unemployment taxes. Both forms ensure employers comply with their tax obligations, yet they serve different purposes under the federal tax system, emphasizing the employer’s responsibilities on a quarterly versus annual basis.

Another document similar to the IRS 941 form is the W-2, the Wage and Tax Statement. This form is a year-end document that employers must send to every employee and the Social Security Administration. It specifies the amount of wages paid and taxes withheld for the year on an individual employee basis. While the IRS 941 form provides a quarterly overview of payroll expenses and tax liabilities for all employees, the W-2 breaks down this information individually and annually, giving employees the details needed to file their personal tax returns.

The IRS 943 form, or the Employer's Annual Federal Tax Return for Agricultural Employees, also shares similarities with the IRS 941 form, but it is specifically designed for agricultural employers. Like the 941 form, the 943 form is used to report wages paid and taxes withheld. However, the significant difference lies in the target audience; the 941 form is for general employers, whereas the 943 focuses on those in the agricultural sector, highlighting the IRS's categorization of tax obligations by industry.

The IRS W-3 form, the Transmittal of Wage and Tax Statements, acts in concordance with the W-2 form but also shares a functional relation to the IRS 941 form. The W-3 is essentially a summary form sent to the Social Security Administration alongside a batch of W-2 forms. It consolidates the annual wage and tax information for all employees of a company. In comparison, the 941 form takes on a similar role but on a quarterly basis and with a focus on reporting to the IRS, ensuring that employers accurately report wage and tax withholding information throughout the year.

Correlating closely with the IRS 941 form is the 944 form, or the Employer's Annual Federal Tax Return. This document is designed for small employers whose annual liability for Social Security, Medicare, and withheld federal income taxes is $1,000 or less. It allows these small businesses to file annually instead of quarterly. The distinction here is in the frequency and eligibility for filing, separating smaller employers from those who are required to file the more routine 941 form.

Last but not least, the Form W-4, Employee's Withholding Certificate, while not a report, profoundly impacts the information on the IRS 941 form. The W-4 allows employees to determine the amount of federal income tax withheld from their paychecks. This form directly influences the withholdings reported on the IRS 941, as it dictates how much income tax an employer should withhold from an employee's wages each pay period. The W-4 and 941 forms work hand-in-hand to ensure accurate payroll tax withholding and reporting.

Dos and Don'ts

When filling out the IRS 941 form, it's important to follow certain guidelines to ensure accuracy and compliance with tax laws. Here’s a list of 10 do's and don'ts to help you complete the form correctly.

Do's:- Review all instructions carefully before beginning to fill out the form to ensure you understand the requirements.

- Ensure accuracy of all information, including Employer Identification Number (EIN), business name, and reporting period.

- Use accurate calculations to determine tax liabilities to avoid under or over-reporting.

- Report all compensation, tips, and other payments to employees within the reporting period.

- Double-check your math and ensure that all calculations are correct and that they align with current tax rates and laws.

- Sign and date the form when finished. An unsigned form is not valid and will not be processed.

- Keep a copy of the form and all relevant paperwork for your records.

- Use the IRS’s electronic filing system if possible for faster processing.

- Submit the form before the deadline to avoid penalties for late filing.

- Seek professional advice if you have any questions or uncertainties about how to complete the form.

- Don’t leave any fields blank; enter “0” or “N/A” where applicable.

- Don’t estimate amounts. Use precise figures for all financial entries.

- Don’t forget to include all necessary schedules or attachments that may apply to your situation.

- Don’t ignore IRS notices or requests for more information. Respond promptly to avoid further issues.

- Don’t use outdated forms. Always check the IRS website for the most current version.

- Don’t submit the form without reviewing it for mistakes. It’s important to catch any errors before submission.

- Don’t disregard line instructions. Each line has specific instructions that are important for proper completion.

- Don’t forget to update your information with the IRS if your business name, address, or EIN has changed.

- Don’t manually correct errors on the form after it’s been finalized. Instead, fill out a new form or follow IRS guidelines for amendments.

- Don’t panic if you make a mistake. The IRS allows amendments to previously filed 941 forms.

Misconceptions

Filing the IRS 941 form can sometimes be confusing. Many people hold misconceptions about how it works and its requirements. Let's debunk some of these myths to give you a clearer understanding.

It's only for large businesses: This is a common misconception. In reality, the IRS 941 form is required for businesses of all sizes that have employees. It's used to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks, and it's not limited to large corporations.

You only file it once a year: Unlike some other tax forms, the IRS 941 is filed quarterly. Businesses must submit it by the end of the month following the end of a quarter. This means deadlines are April 30th, July 31st, October 31st, and January 31st for the respective quarters.

If no taxes are owed, filing isn't necessary: Even if your business hasn't withheld any taxes for a quarter, you're still required to file a 941 form. This is to maintain accurate records and ensure compliance with IRS regulations.

Corrections can't be made after filing: Mistakes happen, and the IRS understands this. If you make an error on your 941 form, you can use Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund, to make corrections. However, it's important to submit it as soon as you identify the mistake.

Electronic filing is optional: As of now, the IRS encourages, but does not require, all businesses to e-file. However, businesses with a certain threshold of taxes due may be required to use the Electronic Federal Tax Payment System (EFTPS). It's always a good idea to check the latest requirements or speak with a tax professional.

The 941 form replaces the need for a W-2 form: This is not true. The IRS 941 form and W-2 form serve different purposes. Form 941 is used to report the total payroll taxes withheld from all employees’ paychecks quarterly, while the W-2 form reports an individual employee's annual wages and taxes withheld. Employers need to file both forms.

Small mistakes on the form aren't a big deal: Even small errors can lead to processing delays or notices from the IRS. It's crucial to double-check all entries on the form to ensure accuracy. This includes verifying Social Security numbers, calculations, and the total amounts of taxes withheld and paid.

You can't get help from the IRS with Form 941: The IRS provides resources and support for businesses struggling with Form 941. Their website offers instructions, FAQs, and even a dedicated helpline. If you're unsure about something, it's always better to ask for help rather than make an assumption.

Key takeaways

When it comes to managing your business's federal tax responsibilities, understanding how to properly fill out and use the IRS 941 form is crucial. This form is used to report quarterly payroll taxes. Here are five key takeaways to keep in mind:

- Know the deadlines: The IRS 941 form is due four times a year, following the end of each quarter. Specifically, it must be submitted by the last day of the month that follows the end of the quarter. This means the deadlines are April 30, July 31, October 31, and January 31 for the fourth quarter of the previous year.

- Gather your information: Before sitting down to fill out the form, make sure you have all necessary information on hand. This includes total wages paid, federal income tax withheld, and both employer and employee shares of Social Security and Medicare taxes.

- Accuracy is key: It's important to double-check your numbers. Reporting inaccurate information can lead to penalties or even an audit. If numbers have changed since you initially recorded them, be sure to update them before submitting the form.

- Electronic Filing: Employers can file the IRS 941 form electronically, which is faster and reduces the risk of errors. The IRS encourages electronic filing, but if you choose to mail your form, make sure it's sent to the correct address for your state.

- Keep records: After filing your IRS 941 form, keep a copy for your records. You should store all related documents for at least four years after the due date for filing. These records can be invaluable in case of questions from either the IRS or your employees about reported wages and taxes.

Popular PDF Documents

8814 Instructions - By using form 8814, parents can avoid the necessity of filing a separate tax return for their child, streamlining the tax filing process.

Pa Real Estate Forms - The form's structure and requirements reinforce the importance of full disclosure and transparency in property transactions.