Get IRS 8718 Form

For organizations seeking recognition of their tax-exempt status under various provisions, navigating the complexities of the required documentation can be a daunting task. Key among the required documents is the IRS Form 8718, a crucial component in the process of applying for tax exemption. This form serves as a user fee for exempt organization determination letter request, essentially functioning as the payment form for the processing of the status application. Its significance cannot be understated, as it accompanies the exemption application to ensure that the review of an organization's request is initiated. The form itself is relatively straightforward but requires meticulous attention to detail to ensure that all pertinent information is accurately captured. From specifying the type of exemption being sought to calculating the correct fee based on the organization’s financial thresholds, the form encapsulates a critical step in achieving the coveted tax-exempt status. Furthermore, it represents the tangible commitment of the organization to comply with the federal regulations governing charitable and non-profit entities, marking the beginning of a transparent and accountable relationship with the Internal Revenue Service.

IRS 8718 Example

|

|

|

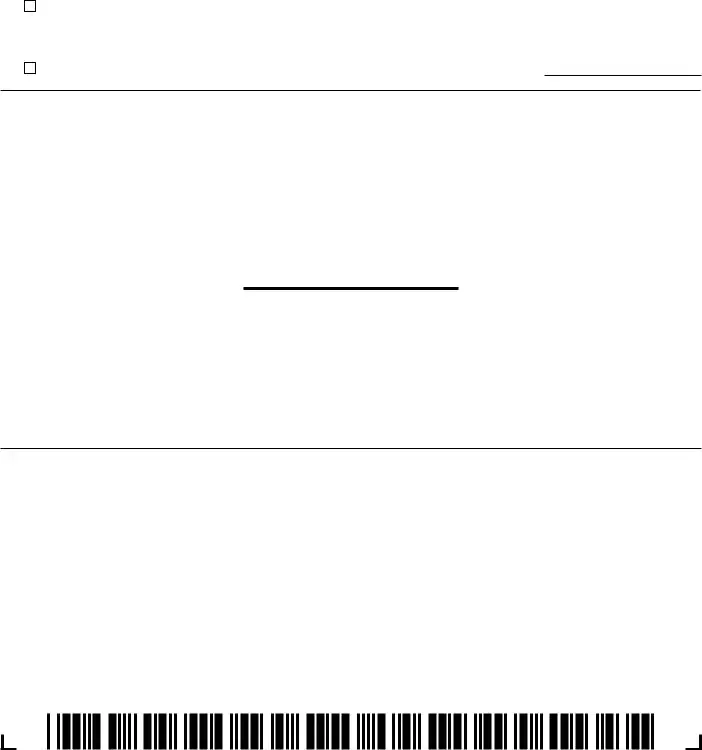

User Fee for Exempt Organization |

|

|

For |

|

|

|

|

|

||

Form 8718 |

|

|

|

|

Control number |

||||||||

|

|

|

|

|

|

|

|

|

|

OMB No. |

|||

|

|

|

|

Determination Letter Request |

|

|

IRS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

(Rev. November 2021) |

|

▶ Attach this form to determination letter application. |

|

|

Use |

|

Amount paid |

|

|||||

Department of the Treasury |

|

(Form 8718 is NOT a determination letter application.) |

|

|

Only |

|

User fee screener |

||||||

|

▶ Go to www.irs.gov/Form8718 for the latest information. |

|

|

|

|

|

|

|

|

||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

||||

Name of organization |

|

|

Employer Identification |

Number |

|

|

|

|

|

||||

|

|

|

|

|

|||||||||

|

|

Caution: Do not attach Form 8718 to an application for a pension plan determination letter. Use Form 8717 instead. |

|||||||||||

1 |

|

Type of request |

|

|

|

|

|

|

Fee |

||||

a |

Application for recognition of exemption under section 501 or under section 521 from |

|

|

|

|

|

|

|

|

||||

|

|

organizations (other than pension, |

|

|

|

|

|

|

|

|

|||

|

|

section 401). Enter the applicable fee amount . . . . . . . . . . . . . . ▶ |

$ |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b

Group exemption letters . . . . . . . . . . . . . . . . . . . . . ▶ $

Section references are to the Internal Revenue Code, unless otherwise noted.

Instructions

The law requires payment of a user fee with each application for a determination letter. For more information, see Rev. Proc.

Check only one box on line 1 for the type of application you are submitting. Then, enter the appropriate user fee amount in the space provided.

Caution: The application will not be processed without payment of the proper user fee.

Attach to Form 8718 a check or money order payable to the “United States Treasury” for the full amount of the user fee. If you do not include the full amount, your application will be returned. Attach Form 8718 to your determination letter application.

Generally, the user fee will be refunded only if the Internal Revenue Service declines to issue a determination.

Where To File

Send the determination letter application and Form 8718 to:

Internal Revenue Service

TE/GE Stop 31A Team 105 P.O. Box 12192 Covington, KY

Who Should File

Organizations applying for federal income tax exemption, other than filers of Form 1023, Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code, Form

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated burden for tax exempt taxpayers filing this form is approved under OMB control number

If you have suggestions for making this form simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/FormComments. Or you can send your comments to the Internal Revenue Service, Tax Forms and Publications, 1111 Constitution Ave. NW,

Cat. No. 64728Z |

Form 8718 (Rev. |

Document Specifics

| Fact Number | Description |

|---|---|

| 1 | The Form 8718 is used by organizations seeking to be recognized as tax-exempt under certain sections of the Internal Revenue Code. |

| 2 | This form must accompany the application for recognition of exemption, specifically when a user fee is required. |

| 3 | It assists in determining the correct user fee applicable to the exemption application, based on the organization's financial data. |

| 4 | The IRS categorizes fees into different tiers, depending on the organization's gross receipts and type of exemption sought. |

| 5 | Completion of Form 8718 is critical for the processing of the exemption application; incorrect or missing information can lead to delays. |

| 6 | As of the last update, the form does not have state-specific versions; it is a federal form administered by the Internal Revenue Service. |

| 7 | Governing laws for Form 8718 include federal tax laws and regulations pertaining to tax-exempt status, primarily found in the Internal Revenue Code. |

Guide to Writing IRS 8718

Filing out the IRS 8718 form is a critical step for organizations seeking to attain or retain a tax-exempt status. Once submitted, this form will be processed by the IRS to review the organization's status. Completing this form accurately is essential for ensuring a smooth process. The steps outlined below will guide individuals through the necessary sections of the form to complete and submit it properly.

- Start by providing the organization's name and Employer Identification Number (EIN) in the spaces allocated at the top of the form.

- Under "User Fee Information," select the type of application your organization is submitting the form for. This could be for a new application or a reinstatement.

- Identify the appropriate user fee for your organization based on its average annual gross receipts. This information informs the fee you will need to include with your submission.

- Fill in the amount of the user fee in the space provided. Ensure the amount is correct as per the instructions provided in the form based on your organization's gross receipts.

- Provide the date and your title in the organization in the section designed for the authorized signature. By signing the form, you are certifying that all the information provided is accurate to the best of your knowledge.

- Double-check all the information provided for accuracy. Verify that the form is signed and dated.

- Mail the completed form along with the necessary user fee payment to the address provided in the form's instructions. Make sure to use a mail service that provides tracking for your records.

After the form is sent, it is crucial to wait patiently for the IRS to process your submission. Processing times can vary based on the volume of applications the IRS is handling. Keep a copy of the submitted form and any postal service tracking information as part of your records. This ensures that you have the necessary documentation if the IRS requires further information or if there are any questions about your submission.

Understanding IRS 8718

-

What is the IRS 8718 form used for?

The IRS 8718 form, officially known as the "User Fee for Exempt Organization Determination Letter Request," is a document used by organizations seeking recognition of tax-exempt status under certain sections of the Internal Revenue Code. This form accompanies the application for exemption, determining the fee required based on the type of exemption requested. Its primary function is to calculate and collect the user fee necessary for the processing of exemption applications.

-

Who needs to file IRS Form 8718?

Organizations applying for tax-exempt status with the IRS, including charities, non-profits, and religious organizations, need to file IRS Form 8718 alongside their exemption application, such as Form 1023 or Form 1024, among others. This requirement applies to entities seeking recognition under sections that necessitate a user fee for processing their applications.

-

How is the fee on Form 8718 determined?

The fee for processing an exemption application, as determined by Form 8718, varies depending on the type of application submitted and the organization's gross receipts. The IRS sets specific fee tiers; organizations with lower annual receipts typically pay a lower fee than larger organizations. The form includes instructions to help determine the fee category applicable to your organization.

-

Can the fee for IRS Form 8718 be waived?

Generally, the IRS does not waive the user fee for processing exemption applications. However, in very rare and exceptional cases, an organization may request a fee reduction or waiver. Such requests must include a detailed explanation and justification for the waiver, and the final decision rests with the IRS. It is important to review the current IRS guidelines or consult with a tax professional for the most accurate information regarding fee waivers.

-

What happens if the wrong fee is submitted with Form 8718?

If an organization submits the incorrect fee with Form 8718, it may delay the processing of the exemption application. The IRS might reach out to the organization to request the additional amount needed or, if overpaid, notify them of the overpayment. To prevent delays, it's crucial to carefully review the fee schedule and ensure the correct amount is submitted with the application.

-

Where do I send IRS Form 8718 and the associated application?

The mailing address for IRS Form 8718, along with the associated exemption application, depends on the type of organization and its location. The IRS provides specific mailing addresses for different forms and types of applicants on its official website. Always check the most recent IRS instructions for Form 8718 to find the correct mailing address and ensure your application is sent to the right place.

Common mistakes

When filling out the IRS 8718 form, users often encounter a series of common errors that can delay the processing of their applications or even lead to rejections. It's crucial to approach this document with meticulous attention to detail. Below are seven mistakes frequently made:

-

Not Checking the Appropriate User Fee Box: One of the initial steps when filling out Form 8718 involves selecting the specific user fee box applicable to your request. This selection is crucial because it determines the processing fee required. Applicants sometimes overlook or mistakenly check the wrong box, leading to incorrect fee submissions.

-

Incomplete Information: Leaving sections blank is a common error. The IRS requires complete information to process the form efficiently. Neglecting to fill in all the required fields can result in significant processing delays or the need to resubmit the form.

-

Incorrect Payment Amount: Calculating the correct fee can be tricky, and applicants often submit either too much or too little. This mistake usually stems from not thoroughly reading the instructions or misunderstanding the fee structure related to their specific application.

-

Failure to Sign the Form: An unsigned form is like an unanswered call—it goes nowhere. The omission of a signature is a surprisingly common oversight that invalidates the submission. Always double-check that every required signature is in place before sending off the document.

-

Miswriting the EIN or SSN: Each organization or individual has a unique Employer Identification Number (EIN) or Social Security Number (SSN) that must be accurately included on the form. Miswriting these numbers can misdirect your application or result in processing delays.

-

Wrong Address or Contact Information: If the IRS needs to reach out for further information or to deliver a decision, outdated or incorrect contact details can significantly complicate matters. Ensure that every piece of contact information is current and correct.

-

Forgetting to Attach Required Documents: The IRS 8718 form often requires supplementary documents. Failing to attach all necessary documentation can halt the processing of your application. Always cross-reference your submission with the checklist provided in the form's instructions to verify that nothing is missing.

To sidestep these pitfalls, applicants should take their time, meticulously review every section of the form and the accompanying instructions, and double-check their information before submission. A careful approach ensures that your application is processed smoothly and without unnecessary delay.

Documents used along the form

When organizations apply for tax-exempt status, the IRS Form 8718 often serves as a cornerstone document. However, this form rarely travels alone. Other forms and documents typically accompany it, each playing its own crucial role in the application process or in maintaining the status once granted. Having a comprehensive understanding of these additional forms not only streamlines the application process but also ensures organizations remain in good standing with regulatory requirements.

- Form 1023: This is the application for recognition of exemption under section 501(c)(3) of the Internal Revenue Code. It's detailed and requires substantial information about the organization's purpose, governance, and financial projections.

- Form 1024: Similar to Form 1023, this form is used by organizations seeking tax-exempt status but under sections other than 501(c)(3). It caters to a wide variety of organizations including social clubs, trade associations, and fraternal societies.

- Form 990: Known as the "Return of Organization Exempt From Income Tax," this form is filed annually. It provides the IRS with information about the organization's operations and financial status. It's a public document, often used by donors and analysts to assess an organization's health and compliance.

- Form 8821: This form authorizes individuals or organizations to request and inspect confidential IRS information on your behalf. It's often used in conjunction with applications for tax-exempt status to enable legal or financial representatives to interact with the IRS directly.

- Bylaws: These are not IRS forms but are critical documents that outline the governance rules under which a tax-exempt organization operates. The IRS may request a copy to understand the organizational structure and ensure compliance with regulations governing tax-exempt entities.

- Articles of Incorporation: Required for incorporation, these legal documents establish the creation of an organization. They are typically filed with a state government and must be provided to the IRS when applying for tax-exempt status.

- Conflict of Interest Policy: This document outlines procedures to prevent the personal interest of an organization's leaders from interfering with their duty to the organization. The IRS reviews this policy to ensure that the organization is being run for the benefit of the public, and not for private interests.

- Financial Statements: Comprehensive financial records are crucial. They can include balance sheets, income statements, and statements of functional expenses. These documents offer the IRS insights into the organization's financial viability and adherence to the principles guiding tax-exempt entities.

Understanding and preparing these documents with care can significantly affect an organization's ability to achieve and maintain tax-exempt status. Each document serves a unique purpose, acting as a building block in the foundation of a transparent, compliant, and effective organization. Comprehensive preparation and attention to detail in this process not only facilitate a smoother application but also pave the way for ongoing success.

Similar forms

The IRS form 8718 is crucial for tax-exempt organizations, particularly those seeking to obtain or maintain their tax-exempt status. A document closely related to the IRS Form 8718 is the IRS Form 1023. The IRS Form 1023 is specifically designed for organizations applying for recognition of exemption under section 501(c)(3) of the Internal Revenue Code. Both forms are integral to the process of being recognized as a tax-exempt entity, yet the IRS Form 1023 is more detailed, requiring comprehensive information about the organization's structure, governance, and program activities.

Similarly, IRS Form 1024 shares a common purpose with IRS Form 8718 in that it is used by organizations seeking tax-exempt status but under different sections of the Internal Revenue Code, such as 501(c)(4), (c)(6), or (c)(7). Both forms serve as a means to apply for tax exemption, but Form 1024 caters to a broader category of organizations, demanding specific details about their objectives, memberships, and operations to justify their tax-exempt requests.

Another document that shares similarities with the IRS Form 8718 is the IRS Form 990. This form is an annual reporting return that certain tax-exempt organizations must file with the IRS. It provides the IRS with information on the organization's operations, financial condition, and compliance with tax obligations. While Form 8718 is typically a onetime submission for fee determination related to tax-exempt status, Form 990 is an ongoing requirement, emphasizing the operational and financial transparency of the organization.

IRS Form 8868 is another document akin to the IRS Form 8718 in the context of tax-exempt organizations. This form is used to request an automatic extension of time to file an organization's Form 990, 990-EZ, 990-PF, or 990-T. Although IRS Form 8868 deals with extending filing deadlines and Form 8718 relates to the fee determination for tax-exempt status applications, both are crucial in the administrative maintenance and compliance of tax-exempt organizations with IRS regulations.

The IRS Form 8940 shares a slight resemblance with IRS Form 8718, as it is used by tax-exempt organizations to request specific determinations or rulings from the IRS. Requests can include changes in organizational structure, classification, or operation. While Form 8718 is focused on the fee determination for applying for exemption status, Form 8940 covers a variety of other requests that an already tax-exempt organization might need to remain in compliance or to update its status with the IRS.

IRS Form SS-4, Application for Employer Identification Number (EIN), is indirectly related to the IRS Form 8718. Though their purposes differ significantly—Form SS-4 is for obtaining an EIN, necessary for tax reporting, opening bank accounts, and hiring employees—both forms are initial steps that newly established organizations often complete. Securing an EIN is a precursor to many organizational activities, including applying for tax-exempt status, for which the IRS Form 8718 fee determination is a crucial part.

Lastly, the IRS Form 5578 is somewhat similar to the IRS Form 8718 in its association with tax-exempt status, specifically in ensuring compliance with anti-discrimination laws. Form 5578 is an annual certification used by tax-exempt private schools to affirm that they have adopted racially nondiscriminatory policies. While Form 5578 focuses on compliance with civil rights, and Form 8718 on tax-exemption application fees, both underscore the breadth of regulatory compliance necessary for tax-exempt organizations.

Dos and Don'ts

When filling out the IRS 8718 form, which is used to determine the user fee for a tax-exempt application, individuals should pay close attention to detail and adhere to the following guidelines:

Do's:

- Ensure that all information is complete and accurate. Checking and double-checking the filled-out form can prevent unnecessary delays or issues with the application process.

- Use the most current version of the form. The Internal Revenue Service (IRS) frequently updates its forms, so using the latest version ensures compliance with the current requirements.

- Consult the instructions provided by the IRS for the 8718 form. These instructions provide valuable guidance on how to correctly fill out the form and calculate the required user fee.

- Keep a copy of the filled-out form for your records. This is crucial for future reference or in case the IRS has questions or requires additional information.

Don'ts:

- Do not leave any required fields blank. Incomplete forms may result in processing delays or rejection of the application.

- Avoid making handwritten changes or corrections to the form. If a mistake is made, it is better to start with a fresh form to ensure legibility and avoid confusion.

- Do not estimate or guess when providing information. All data should be accurate and verifiable to avoid issues with the IRS.

- Resist the temptation to submit the form without the necessary supporting documents. The absence of required attachments could lead to the application being deemed incomplete.

Misconceptions

When it comes to understanding IRS forms, it's easy to get lost in the complex maze of documents and instructions. The IRS 8718 form is no exception, and there are several common misconceptions surrounding its use and purpose. Let's demystify some of these misunderstandings:

It's only for tax-exempt organizations. A common misconception is that the IRS 8718 form is exclusively for organizations seeking tax-exempt status. While it's true that tax-exempt organizations use this form as part of their application process, it's actually a user fee form for requesting certain services from the IRS, not limited to tax-exempt status applications. This form is required for various determinations and changes, including but not limited to tax-exempt status.

The form can be filed electronically. In an era where digital filing is becoming the norm for many tax-related forms, people often assume that IRS 8718 can easily be submitted through the IRS’s electronic filing systems. However, as of the last update, this specific form must be completed and submitted in paper form along with the appropriate payment for the user fee. It's essential to check the latest filing requirements directly with the IRS or through a professional, as these guidelines can change.

Completion of the form guarantees initiation of the process. Completion and submission of IRS 8718, along with the correct fee, is indeed required to begin the process for which the form is intended. However, submission alone does not guarantee that the process will be initiated without any hitches. The IRS may request additional information or clarification, which can delay the process. It's crucial for applicants to ensure that all sections of the form are filled out accurately and that the accompanying documentation is complete to avoid any unnecessary delays.

Fees are the same for all types of requests. It's easy to assume that the user fee for submitting IRS 8718 is a one-size-fits-all. However, the truth is that the fee can vary significantly depending on the specific request or application being made. Fees are determined by the IRS and can change, so it's important for applicants to verify the current fee schedule before making a payment. This will ensure that the submission process is not delayed due to issues with the payment amount.

Understanding these misconceptions can greatly ease the process of dealing with IRS 8718 and ensure that individuals and organizations are better prepared when submitting their forms. As with any IRS form, when in doubt, seeking clarification from a tax professional or directly from the IRS is always the best course of action.

Key takeaways

The IRS Form 8718 is a crucial document for organizations seeking tax-exempt status or submitting certain requests to the Internal Revenue Service. Understanding its purpose, how to fill it out correctly, and its role in the submission process is important for a smooth experience. Here are ten key takeaways for dealing with this form:

- Determine Applicability: Before starting, ensure that Form 8718 is required for your specific application or request. This form is primarily used for certain tax-exempt status applications.

- Accurate Information: Double-check all entered information for accuracy. Mistakes can delay processing or result in the need to resubmit the form.

- User Fee: Form 8718 is used to compute and submit the user fee for your application. Make sure to calculate this fee correctly based on the latest IRS guidelines.

- Current Version: Use the most current version of Form 8718. The IRS periodically updates forms, so using the most recent version ensures compliance with current regulations.

- Read Instructions Carefully: Thoroughly read the instructions provided by the IRS for Form 8718. These instructions contain important details about how to properly complete and submit the form.

- Attach Required Documentation: Ensure all necessary documentation is attached to your Form 8718 submission. Missing documents can lead to delays.

- Sign and Date: Don’t forget to sign and date Form 8718. An unsigned form is considered incomplete and will not be processed.

- Keep a Copy: Always keep a copy of the completed Form 8718 and any attached documents for your records. This can be helpful in case of inquiries or for tracking the status of your application.

- Follow Submission Guidelines: Pay close attention to the submission guidelines. This includes where to send the form, whether electronic filing is an option, and any other specific mailing instructions.

- Be Prepared for Follow-up: After submitting Form 8718, be prepared for potential follow-up from the IRS. They may request additional information to process your application.

Successfully submitting IRS Form 8718 is a step toward achieving your organization’s tax-exempt status or other tax-related objectives. Paying attention to the details and understanding the form’s requirements can streamline the process, making it as efficient as possible.

Popular PDF Documents

1099-div Form 2022 - Investors with diversified portfolios might receive multiple 1099-DIV forms, each needing to be reported separately in their tax filings.

Wv Sales and Use Tax Form - Outlines that specific agricultural equipment and services, including propane for poultry heating, are covered under this exemption.

IRS 2106 - IRS Form 2106 is specifically for employees who itemize deductions on Schedule A of the 1040 form.