Get IRS 8300 Form

Engaging with the financial side of operations is a critical aspect for individuals and businesses alike, especially when it involves substantial amounts of cash. One of the pivotal components in this domain is the IRS 8300 form, a crucial document for reporting cash payments over $10,000 received in a trade or business. This form serves as a tool for the Internal Revenue Service (IRS) and the Financial Crimes Enforcement Network (FinCEN) to track large sums of money, aiming to prevent money laundering and ensure compliance with tax laws. Its importance cannot be overstated, as failure to properly file this form can lead to significant penalties. The form requires detailed information about the transaction, including the identity of the person from whom the cash was received, making it a potent instrument against illegal financial activities. Navigating through the rules and requirements of the IRS 8300 form can be daunting, yet understanding its purpose, the process of completion, and the implications of non-compliance is essential for anyone involved in sizable cash transactions within their business operations.

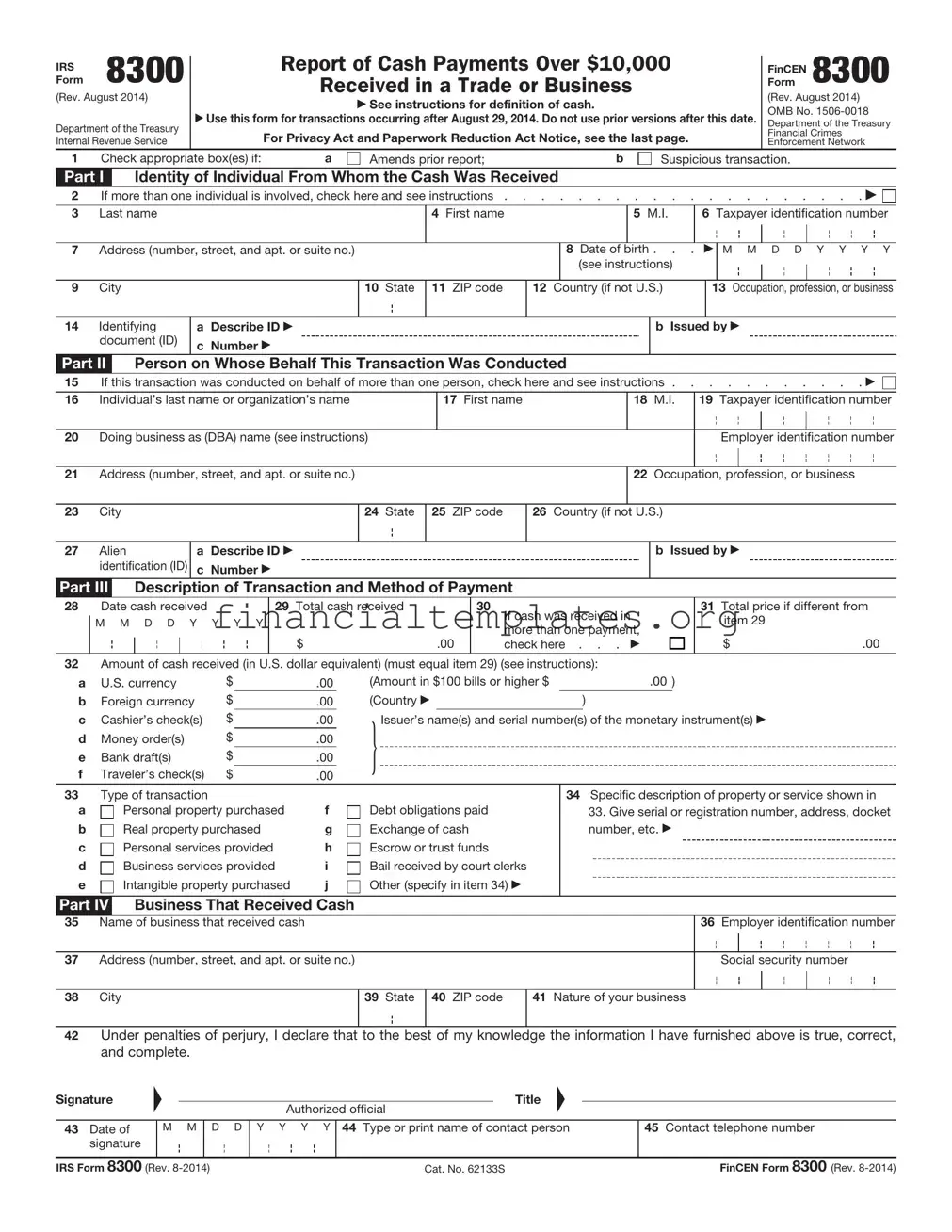

IRS 8300 Example

IRSForm 8300

(Rev. August 2014)

Department of the Treasury Internal Revenue Service

Report of Cash Payments Over $10,000

Received in a Trade or Business

See instructions for definition of cash.

Use this form for transactions occurring after August 29, 2014. Do not use prior versions after this date.

For Privacy Act and Paperwork Reduction Act Notice, see the last page.

FinCENForm 8300

(Rev. August 2014) OMB No.

Department of the Treasury

Financial Crimes

Enforcement Network

1 |

Check appropriate box(es) if: |

a |

Amends prior report; |

b |

Suspicious transaction.

Part I |

|

Identity of Individual From Whom the Cash Was Received |

|

|

|

|

|

||||||

2 |

If more than one individual is involved, check here and see instructions |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

Last name |

|

4 First name |

|

|

5 M.I. |

6 Taxpayer identification number |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

|

8 Date of |

birth . . . |

|

|

M M D D Y Y Y Y |

||||

|

|

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|||

9 |

City |

|

10 State |

11 ZIP code |

12 |

Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

Part II Person on Whose Behalf This Transaction Was Conducted

15 If this transaction was conducted on behalf of more than one person, check here and see instructions . . . . . . . . . . .

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

Part III Description of Transaction and Method of Payment

28Date cash received

M M D D Y Y Y Y

29Total cash received

$.00

30

If cash was received in more than one payment, check here . . .

31Total price if different from item 29

$.00

32Amount of cash received (in U.S. dollar equivalent) (must equal item 29) (see instructions):

a |

U.S. currency |

$ |

.00 |

(Amount in $100 bills or higher $ |

.00 ) |

|||||

b |

Foreign currency |

$ |

.00 |

(Country |

|

) |

|

|||

c |

|

$ |

|

} |

|

|

|

|

|

|

Cashier’s check(s) |

.00 |

Issuer’s name(s) and serial number(s) of the monetary instrument(s) |

||||||||

|

||||||||||

d |

Money order(s) |

$ |

.00 |

|

|

|

|

|

|

|

e |

Bank draft(s) |

$ |

.00 |

|

|

|

|

|

|

|

f |

Traveler’s check(s) |

$ |

.00 |

|

|

|

|

|

|

|

33Type of transaction

a |

Personal property purchased |

f |

b |

Real property purchased |

g |

c |

Personal services provided |

h |

d |

Business services provided |

i |

e |

Intangible property purchased |

j |

Debt obligations paid Exchange of cash Escrow or trust funds

Bail received by court clerks Other (specify in item 34)

34Specific description of property or service shown in

33.Give serial or registration number, address, docket number, etc.

Part IV Business That Received Cash

35Name of business that received cash

36Employer identification number

37Address (number, street, and apt. or suite no.)

Social security number

38City

39State

40ZIP code

41Nature of your business

42Under penalties of perjury, I declare that to the best of my knowledge the information I have furnished above is true, correct, and complete.

Signature

43Date of signature

|

|

|

|

|

|

Title |

|

|

|

F |

Authorized official |

F |

|

|

|||||

|

|

|

|||||||

|

M M |

D D |

Y Y Y Y |

44 Type or print name of contact person |

|

45 Contact telephone number |

|||

|

|

|

|

|

|

|

|

|

|

IRS Form 8300 (Rev. |

Cat. No. 62133S |

FinCEN Form 8300 (Rev. |

IRS Form 8300 (Rev.

Multiple Parties

(Complete applicable parts below if box 2 or 15 on page 1 is checked.)

Part I

3Last name

4First name

5M.I.

6Taxpayer identification number

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

8 Date of birth . . . |

M M D D Y Y Y Y |

|||||

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

12 Country (if |

not U.S.) |

13 Occupation, profession, or business |

|||

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

3Last name

4First name

5M.I.

6Taxpayer identification number

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

8 Date of birth . . . |

M M D D Y Y Y Y |

|||||

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

12 Country (if |

not U.S.) |

13 Occupation, profession, or business |

|||

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

Part II

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

Comments – Please use the lines provided below to comment on or clarify any information you entered on any line in Parts I, II, III, and IV

IRS Form 8300 (Rev. |

FinCEN Form 8300 (Rev. |

IRS Form 8300 (Rev. |

Page 3 |

FinCEN Form 8300 (Rev. |

Section references are to the Internal Revenue Code unless otherwise noted.

Future Developments

For the latest information about developments related to Form 8300 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/form8300.

Important Reminders

•Section 6050I (26 United States Code (U.S.C.) 6050I) and 31 U.S.C. 5331 require that certain information be reported to the IRS and the Financial Crimes Enforcement Network (FinCEN). This information must be reported on IRS/FinCEN Form 8300.

•Item 33, box i, is to be checked only by clerks of the court; box d is to be checked by bail bondsmen. See Item 33 under Part III, later.

•The meaning of the word “currency” for purposes of 31 U.S.C. 5331 is the same as for the word “cash” (See Cash under Definitions, later).

General Instructions

Who must file. Each person engaged in a trade or business who, in the course of that trade or business, receives more than $10,000 in cash in one transaction or in two or more related transactions, must file Form 8300. Any transactions conducted between a payer (or its agent) and the recipient in a

Keep a copy of each Form 8300 for 5 years from the date you file it.

Clerks of federal or state courts must file Form 8300 if more than $10,000 in cash is received as bail for an individual(s) charged with certain criminal offenses. For these purposes, a clerk includes the clerk’s office or any other office, department, division, branch, or unit of the court that is authorized to receive bail. If a person receives bail on behalf of a clerk, the clerk is treated as receiving the bail. See Item 33 under Part III, later.

If multiple payments are made in cash to satisfy bail and the initial payment does not exceed $10,000, the initial payment and subsequent payments must be aggregated and the information return must be filed by the 15th day after receipt of the payment that causes the aggregate amount to exceed $10,000 in cash. In such cases, the reporting requirement can be satisfied by sending a single written statement with the

aggregate Form 8300 amounts listed relating to that payer. Payments made to satisfy separate bail requirements are not required to be aggregated. See Treasury Regulations section

Casinos must file Form 8300 for nongaming activities (restaurants, shops, etc.).

Voluntary use of Form 8300. Form

8300 may be filed voluntarily for any suspicious transaction (see Definitions, later) for use by FinCEN and the IRS, even if the total amount does not exceed $10,000.

Exceptions. Cash is not required to be reported if it is received:

•By a financial institution required to file FinCEN Report 112, BSA Currency Transaction Report (BCTR);

•By a casino required to file (or exempt from filing) FinCEN Report 112, if the cash is received as part of its gaming business;

•By an agent who receives the cash from a principal, if the agent uses all of the cash within 15 days in a second transaction that is reportable on Form 8300 or on FinCEN Report 112, and discloses all the information necessary to complete Part II of Form 8300 or FinCEN Report 112 to the recipient of the cash in the second transaction;

•In a transaction occurring entirely outside the United States. See Publication 1544, Reporting Cash Payments of Over $10,000 (Received in a Trade or Business), regarding transactions occurring in Puerto Rico and territories and possessions of the United States; or

•In a transaction that is not in the course of a person’s trade or business.

When to file. File Form 8300 by the 15th day after the date the cash was received. If that date falls on a Saturday, Sunday, or legal holiday, file the form on the next business day.

Where to file. File the form with the Internal Revenue Service, Detroit Computing Center, P.O. Box 32621, Detroit, Ml 48232.

You may be able to

TIP electronically file Form 8300 using FinCEN's Bank Secrecy Act (BSA) Electronic Filing

Statement to be provided. You must give a written or electronic statement to each person named on a required Form 8300 on or before January 31 of the year following the calendar year in which the

cash is received. The statement must show the name, telephone number, and address of the information contact for the business, the aggregate amount of reportable cash received, and that the information was furnished to the IRS. Keep a copy of the statement for your records.

Multiple payments. If you receive more than one cash payment for a single transaction or for related transactions, you must report the multiple payments any time you receive a total amount that exceeds $10,000 within any

Taxpayer identification number (TIN). You must furnish the correct TIN of the person or persons from whom you receive the cash and, if applicable, the person or persons on whose behalf the transaction is being conducted. You may be subject to penalties for an incorrect or missing TIN.

The TIN for an individual (including a sole proprietorship) is the individual’s social security number (SSN). For certain resident aliens who are not eligible to get an SSN and nonresident aliens who are required to file tax returns, it is an IRS Individual Taxpayer Identification Number (ITIN). For other persons, including corporations, partnerships, and estates, it is the employer identification number (EIN).

If you have requested but are not able to get a TIN for one or more of the parties to a transaction within 15 days following the transaction, file the report and use the comments section on page 2 of the form to explain why the TIN is not included.

Exception. You are not required to provide the TIN of a person who is a nonresident alien individual or a foreign organization if that person or foreign organization:

•Does not have income effectively connected with the conduct of a U.S. trade or business;

•Does not have an office or place of business, or a fiscal or paying agent in the U.S.;

•Does not furnish a withholding certificate described in

(3) or

•Does not have to furnish a TIN on any return, statement, or other document as required by the income tax regulations under section 897 or 1445.

IRS Form 8300 (Rev. |

Page 4 |

FinCEN Form 8300 (Rev. |

Penalties. You may be subject to penalties if you fail to file a correct and complete Form 8300 on time and you cannot show that the failure was due to reasonable cause. You may also be subject to penalties if you fail to furnish timely a correct and complete statement to each person named in a required report. A minimum penalty of $25,000 may be imposed if the failure is due to an intentional or willful disregard of the cash reporting requirements.

Penalties may also be imposed for causing, or attempting to cause, a trade or business to fail to file a required report; for causing, or attempting to cause, a trade or business to file a required report containing a material omission or misstatement of fact; or for structuring, or attempting to structure, transactions to avoid the reporting requirements. These violations may also be subject to criminal prosecution which, upon conviction, may result in imprisonment of up to 5 years or fines of up to $250,000 for individuals and $500,000 for corporations or both.

Definitions

Cash. The term “cash” means the following.

•U.S. and foreign coin and currency received in any transaction; or

•A cashier’s check, money order, bank draft, or traveler’s check having a face amount of $10,000 or less that is received in a designated reporting transaction (defined below), or that is received in any transaction in which the recipient knows that the instrument is being used in an attempt to avoid the reporting of the transaction under either section 6050I or 31 U.S.C. 5331.

Note. Cash does not include a check drawn on the payer’s own account, such as a personal check, regardless of the amount.

Designated reporting transaction. A retail sale (or the receipt of funds by a broker or other intermediary in connection with a retail sale) of a consumer durable, a collectible, or a travel or entertainment activity.

Retail sale. Any sale (whether or not the sale is for resale or for any other purpose) made in the course of a trade or business if that trade or business principally consists of making sales to ultimate consumers.

Consumer durable. An item of tangible personal property of a type that, under ordinary usage, can reasonably be expected to remain useful for at least 1 year, and that has a sales price of more than $10,000.

Collectible. Any work of art, rug, antique, metal, gem, stamp, coin, etc.

Travel or entertainment activity. An item of travel or entertainment that pertains to a single trip or event if the combined sales price of the item and all other items relating to the same trip or event that are sold in the same transaction (or related transactions) exceeds $10,000.

Exceptions. A cashier’s check, money order, bank draft, or traveler’s check is not considered received in a designated reporting transaction if it constitutes the proceeds of a bank loan or if it is received as a payment on certain promissory notes, installment sales contracts, or down payment plans. See Publication 1544 for more information.

Person. An individual, corporation, partnership, trust, estate, association, or company.

Recipient. The person receiving the cash. Each branch or other unit of a person’s trade or business is considered a separate recipient unless the branch receiving the cash (or a central office linking the branches), knows or has reason to know the identity of payers making cash payments to other branches.

Transaction. Includes the purchase of property or services, the payment of debt, the exchange of cash for a negotiable instrument, and the receipt of cash to be held in escrow or trust. A single transaction may not be broken into multiple transactions to avoid reporting.

Suspicious transaction. A suspicious transaction is a transaction in which it appears that a person is attempting to cause Form 8300 not to be filed, or to file a false or incomplete form.

Specific Instructions

You must complete all parts. However, you may skip Part II if the individual named in Part I is conducting the transaction on his or her behalf only. For voluntary reporting of suspicious transactions, see Item 1, next.

Item 1. If you are amending a report, check box 1a. Complete the form in its entirety (Parts

To voluntarily report a suspicious transaction (see Suspicious transaction above), check box 1b. You may also telephone your local IRS Criminal Investigation Division or call the FinCEN Financial Institution Hotline at

Part I

Item 2. If two or more individuals conducted the transaction you are reporting, check the box and complete Part I on page 1 for any one of the individuals. Provide the same

information for the other individual(s) by completing Part I on page 2 of the form. If more than three individuals are involved, provide the same information in the comments section on page 2 of the form.

Item 6. Enter the taxpayer identification number (TIN) of the individual named. See Taxpayer identification number (TIN), earlier, for more information.

Item 8. Enter eight numerals for the date of birth of the individual named. For example, if the individual’s birth date is July 6, 1960, enter “07” “06” “1960.”

Item 13. Fully describe the nature of the occupation, profession, or business (for example, “plumber,” “attorney,” or “automobile dealer”). Do not use general or nondescriptive terms such as “businessman” or

Item 14. You must verify the name and address of the named individual(s). Verification must be made by examination of a document normally accepted as a means of identification when cashing checks (for example, a driver’s license, passport, alien registration card, or other official document). In item 14a, enter the type of document examined. In item 14b, identify the issuer of the document. In item 14c, enter the document’s number. For example, if the individual has a Utah driver’s license, enter “driver’s license” in item 14a, “Utah” in item 14b, and the number appearing on the license in item 14c.

Note. You must complete all three items (a, b, and c) in this line to make sure that Form 8300 will be processed correctly.

Part II

Item 15. If the transaction is being conducted on behalf of more than one person (including husband and wife or parent and child), check the box and complete Part II for any one of the persons. Provide the same information for the other person(s) by completing Part II on page 2. If more than three persons are involved, provide the same information in the comments section on page 2 of the form.

Items 16 through 19. If the person on whose behalf the transaction is being conducted is an individual, complete items 16, 17, and 18. Enter his or her TIN in item 19. If the individual is a sole proprietor and has an employer identification number (EIN), you must enter both the SSN and EIN in item 19. If the person is an organization, put its name as shown on required tax filings in item 16 and its EIN in item 19.

Item 20. If a sole proprietor or organization named in items 16 through 18 is doing business under a name other than that entered in item 16 (for example, a “trade” or “doing business as (DBA)” name), enter it here.

IRS Form 8300 (Rev. |

Page 5 |

FinCEN Form 8300 (Rev. |

Item 27. If the person is not required to furnish a TIN, complete this item. See Taxpayer identification number (TIN), earlier. Enter a description of the type of official document issued to that person in item 27a (for example, a “passport”), the country that issued the document in item 27b, and the document’s number in item 27c.

Note. You must complete all three items (a, b, and c) in this line to make sure that Form 8300 will be processed correctly.

Part III

Item 28. Enter the date you received the cash. If you received the cash in more than one payment, enter the date you received the payment that caused the combined amount to exceed $10,000. See Multiple payments, earlier, for more information.

Item 30. Check this box if the amount shown in item 29 was received in more than one payment (for example, as installment payments or payments on related transactions).

Item 31. Enter the total price of the property, services, amount of cash exchanged, etc. (for example, the total cost of a vehicle purchased, cost of catering service, exchange of currency) if different from the amount shown in item 29.

Item 32. Enter the dollar amount of each form of cash received. Show foreign currency amounts in U.S. dollar equivalent at a fair market rate of exchange available to the public. The sum of the amounts must equal item 29. For cashier’s check, money order, bank draft, or traveler’s check, provide the name of the issuer and the serial number of each instrument. Names of all issuers and all serial numbers involved must be provided. If necessary, provide this information in the comments section on page 2 of the form.

Item 33. Check the appropriate box(es) that describe the transaction. If the transaction is not specified in boxes

Part IV

Item 36. If you are a sole proprietorship, you must enter your SSN. If your business also has an EIN, you must provide the EIN as well. All other business entities must enter an EIN.

Item 41. Fully describe the nature of your business, for example, “attorney” or “jewelry dealer.” Do not use general or nondescriptive terms such as “business” or “store.”

Item 42. This form must be signed by an individual who has been authorized to do so for the business that received the cash.

Comments

Use this section to comment on or clarify anything you may have entered on any line in Parts I, II, III, and IV. For example, if you checked box b (Suspicious transaction) in line 1 above Part I, you may want to explain why you think that the cash transaction you are reporting on Form 8300 may be suspicious.

Privacy Act and Paperwork Reduction Act Notice. Except as otherwise noted, the information solicited on this form is required by the IRS and FinCEN in order to carry out the laws and regulations of the United States. Trades or businesses and clerks of federal and state criminal courts are required to provide the information to the IRS and FinCEN under section 6050I and 31 U.S.C. 5331, respectively. Section 6109 and 31 U.S.C. 5331 require that you provide your identification number. The principal purpose for collecting the information on this form is to maintain reports or records which have a high degree of usefulness in criminal, tax, or regulatory investigations or proceedings, or in the conduct of intelligence or

You are not required to provide information as to whether the reported transaction is deemed suspicious. Failure to provide all other requested information, or providing fraudulent information, may result in criminal prosecution and other penalties under 26 U.S.C. and 31 U.S.C.

Generally, tax returns and return information are confidential, as stated in section 6103. However, section 6103

allows or requires the IRS to disclose or give the information requested on this form to others as described in the Internal Revenue Code. For example, we may disclose your tax information to the Department of Justice, to enforce the tax laws, both civil and criminal, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions, to carry out their tax laws. We may disclose this information to other persons as necessary to obtain information which we cannot get in any other way. We may disclose this information to federal, state, and local child support agencies; and to other federal agencies for the purposes of determining entitlement for benefits or the eligibility for and the repayment of loans. We may also provide the records to appropriate state, local, and foreign criminal law enforcement and regulatory personnel in the performance of their official duties. We may also disclose this information to other countries under a tax treaty, or to federal and state agencies to enforce federal nontax criminal laws and to combat terrorism. In addition, FinCEN may provide the information to those officials if they are conducting intelligence or

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any law under 26 U.S.C. or 31 U.S.C.

The time needed to complete this form will vary depending on individual circumstances. The estimated average time is 21 minutes. If you have comments concerning the accuracy of this time estimate or suggestions for making this form simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/ formspubs. Click on More Information and then click on Give us feedback. Or you can send your comments to Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

Document Specifics

| Fact Name | Description |

|---|---|

| Purpose of IRS 8300 | Used to report cash payments over $10,000 received in a trade or business. |

| Filing Requirement | Must be filed by individuals, companies, corporations, partnerships, associations, trusts, or estates that receive more than $10,000 in cash in a single transaction or related transactions. |

| Transaction Types | Includes transactions related to sales of goods or services, sale of property, rental of property, exchange of cash for other cash, establishment or replenishment of a trust or escrow account, or payment of a loan. |

| Form Details | The form requires identification of the person or entity making the transaction, the amount of cash received, the date of the transaction, and the nature of the transaction. |

| Filing Deadline | The form must be filed within 15 days after the date the cash is received. |

| Identification Requirement | Identification for both the person on whose behalf the transaction is made and the individual conducting the transaction must be provided. |

| Penalties for Non-compliance | Failing to report, intentionally disregarding the requirement, or structuring transactions to avoid reporting can result in civil and criminal penalties. |

| Reporting Method | The form can be filed electronically through the BSA E-Filing System or mailed to the IRS. |

| Governing Law | Federal law as part of the Bank Secrecy Act mandating the reporting of certain transactions to prevent money laundering and other financial crimes. |

Guide to Writing IRS 8300

Filling out the IRS 8300 form is a required process for businesses and individuals alike who receive over $10,000 in cash from a single transaction or related transactions. This form is crucial for reporting these transactions to the IRS and FinCEN, helping in the fight against money laundering. The process can appear daunting at first, but breaking it down into steps can make it manageable and straightforward.

- Start by gathering all necessary information about the transaction or series of related transactions that amounted to more than $10,000 in cash. This includes the date, amount, and nature of the transaction, as well as personal details about the individual or entity from whom you received the cash.

- Access the IRS 8300 form. It can be downloaded from the official IRS website. Ensure you have the latest version of the form to comply with current reporting requirements.

- Fill out Part I of the form, which requires identifying information about the individual or entity from whom you received the cash. This will include their name, address, taxpayer identification number (TIN), and occupation or type of business.

- In Part II, detail the transaction. This section asks for the date the cash was received, the amount, and whether the transaction was conducted on behalf of someone else. If reporting transactions related to a trade or business, you’ll also need to check the appropriate box indicating as much.

- Part III requires information on the person or organization on whose behalf the transaction is being reported, if applicable. This section is especially relevant if the cash was received on behalf of another individual or entity.

- Complete Part IV only if the cash was received in a foreign currency. This part asks for the name of the currency and the U.S. dollar equivalent of the cash received.

- Provide a detailed explanation of the transaction in Part V. This is where you describe the nature of the transaction, including any additional relevant information that wasn’t captured in the earlier sections of the form.

- Review the form for any errors or omissions. Make sure all the information provided is accurate and complete to the best of your knowledge.

- Once the form is filled out, sign and date the bottom, affirming that the information is accurate and complete.

- Lastly, submit the completed form to the IRS within 15 days of the transaction. The form can be mailed to the address specified in the form’s instructions or filed electronically, depending on your preference or requirement.

After you have submitted the IRS 8300 form, it's important to keep a copy for your records. The IRS may contact you for additional information if they have any questions about the report. Compliance with the reporting requirements is crucial, not just for legal reasons, but also as a measure to prevent and detect illegal activities such as money laundering.

Understanding IRS 8300

What is the IRS 8300 form?

The IRS 8300 form, officially known as the "Report of Cash Payments Over $10,000 Received in a Trade or Business," is a document that businesses must file with the Internal Revenue Service (IRS) when they receive more than $10,000 in cash from one buyer as a result of a single transaction or two or more related transactions. The form is used to report any transaction or series of related transactions in which the total amount of cash received is over $10,000.

Who needs to file the IRS 8300 form?

Individuals, companies, corporations, partnerships, associations, trusts, or estates that receive more than $10,000 in cash in a single transaction or related transactions within their trade or business are required to file this form. This requirement applies to all businesses, regardless of size, which engage in a trade or business that receives cash payments over the threshold.

What types of transactions require the filing of form 8300?

The filing of form 8300 is required for transactions that involve the receipt of more than $10,000 in cash. This includes, but is not limited to, sales of goods or services, sales of real property, sales of intangible property, rental fees, or exchange of cash for other cash. The transactions can be either a single transaction or two or more related transactions.

What constitutes 'cash' for the purpose of the IRS 8300 form?

For the purposes of the IRS 8300 form, 'cash' includes U.S. and foreign currency, cashier's checks, bank drafts, traveler's checks, and money orders with a face value of $10,000 or less. Personal checks drawn on the account of the writer are not considered 'cash' for the purposes of this form. Also, there are special rules for cashier's checks, bank drafts, traveler's checks, and money orders received in designated reporting transactions or received in any transaction in which the recipient knows the payer is trying to avoid the reporting of the transaction on Form 8300.

When should the IRS 8300 form be filed?

Businesses must file Form 8300 within 15 days after the date the cash was received. If the 15th day falls on a weekend or holiday, the next business day becomes the deadline. Timely filing of this form is crucial to avoid penalties.

What information is required on the IRS 8300 form?

When completing the IRS 8300 form, businesses need to provide detailed information about the transaction. This includes the amount of cash received, the date of the transaction, the business that received the cash, and the identity of the payer. Additional details about the transaction, including a description of the related transaction(s), if applicable, are also required.

Are there any consequences for not filing the IRS 8300 form or filing it late?

Yes, failure to file Form 8300 on time, or intentionally not filing it, can lead to civil and criminal penalties. These penalties are determined based on whether the failure was due to a reasonable cause or was willful. It is important for businesses to file this form when required to avoid potential penalties.

How can I file the IRS 8300 form?

The IRS 8300 form can be filed either electronically or on paper. For electronic filing, businesses can use the Electronic Federal Tax Payment System (EFTPS) or any IRS-approved electronic filing system. For paper filing, the completed form should be mailed to the address listed on the IRS website for the 8300 form. Detailed instructions for filing are available in the form's instructions.

Common mistakes

Filling out the IRS 8300 form can be a critical task for individuals and businesses that have received cash payments over $10,000. The form is used to report these large transactions to the IRS and the Financial Crimes Enforcement Network (FinCEN) to prevent money laundering and other illegal activities. However, errors can occur during the process, leading to potential audits or penalties. Below are seven common mistakes made when filling out the IRS 8300 form.

Not filing the form on time. The IRS mandates that the 8300 form must be filed within 15 days after receiving the payment. Late submissions can attract unwanted attention and might lead to penalties.

Failing to report all qualifying transactions. Some people mistakenly believe that only certain types of transactions need to be reported. In reality, all transactions over $10,000 in cash, including those from related transactions, need to be reported.

Incorrectly identifying the payer. Proper identification of the individual or entity from whom the cash was received is crucial. Errors in names, addresses, or taxpayer identification numbers can lead to processing delays and other issues.

Overlooking details about the transaction. Every detail of the transaction must be reported accurately, including the date, amount, and nature of the transaction. Missing or erroneous details can cause the form to be rejected.

Not including all necessary signatures. The form requires the signatures of the person who received the payment and the individual who is filing the form. Forgetting any of the required signatures can invalidate the submission.

Mismanaging digital and paper submissions. The IRS 8300 form can be filed either by mail or electronically. Choosing the wrong submission method based on your requirement or failing to follow through with the correct procedure can lead to filing errors.

Lack of record keeping. After submitting the IRS 8300 form, it's mandatory to keep a copy for your records for at least five years. Failure to retain these records can result in complications if the IRS or FinCEN requests further information.

Being aware of these mistakes can greatly improve the accuracy of the form submission and ensure compliance with IRS regulations. If there is any doubt or confusion, consulting with a tax professional may help alleviate potential issues.

Documents used along the form

Completing and submitting the IRS Form 8300 is a critical procedure for businesses and individuals who receive more than $10,000 in cash from a transaction or a series of related transactions. This form helps the government track large cash transactions to prevent money laundering and other financial crimes. However, the IRS 8300 form doesn't always stand alone. Several other documents may either support the information on the form or are necessary due to the nature of the transaction. Understanding these documents ensures compliance with legal requirements and aids in accurate reporting.

- Form W-9, Request for Taxpayer Identification Number and Certification: Often used in conjunction with IRS 8300 to obtain the correct taxpayer identification number of the party from whom the cash was received. This ensures accurate reporting to the IRS and helps prevent tax evasion.

- Form W-2, Wage and Tax Statement: Necessary when the transaction involves compensation or remuneration for services, Form W-2 verifies the income of the individual receiving the payment.

- Form 1099-K, Payment Card and Third Party Network Transactions: In scenarios where the transaction is part of a business's taxable income, this form is required to report the payment transactions processed by payment settlement entities.

- Form 1099-MISC, Miscellaneous Income: Used to report payments made to individuals or entities in the course of a business's trade or business. It is relevant when the transaction involves rental, services, prizes, awards, or other income payments.

- Bank Secrecy Act (BSA) Forms: These include various forms such as the Currency Transaction Report (CTR) and the Suspicious Activity Report (SAR), which banks and other financial institutions are required to file to report large currency transactions or suspicious activity, potentially linked to the transaction requiring the IRS 8300 form.

- Customer Identification Program (CIP) Documents: Part of the USA PATRIOT Act requirements, these documents verify the identity of individuals engaging in significant transactions. They might be referenced or required for verification along with IRS 8300 submissions.

- Record of Sales and Purchase Invoices: Keeping thorough records of the transactions, including sales and purchase invoices, supports the cash payment reported on the IRS 8300. These documents provide a detailed context of the transaction.

For businesses and individuals navigating financial reporting requirements, the IRS 8300 form acts as a cornerstone document for transactions involving significant amounts of cash. The documents listed above play a vital role in ensuring that every transaction is accurately and fully reported. Familiarity with these forms and documents can help prevent legal complications and ensure compliance with federal regulations, making the process smoother and more efficient for all parties involved.

Similar forms

The IRS 8300 Form, required for reporting cash payments over $10,000, shares similarities with the FinCEN Form 104 (Currency Transaction Report). Both are used to report large transactions to the government, aiding in the fight against money laundering. The primary purpose is to ensure transparency in significant cash transactions, but whereas IRS 8300 applies to businesses receiving funds, FinCEN Form 104 is specifically for financial institutions reporting transactions occurring within their domain.

Another document with resemblance to the IRS 8300 Form is the W-9 Form (Request for Taxpayer Identification Number and Certification). Both forms are essential in the context of financial transactions and compliance with tax regulations. The IRS 8300 ensures the government is informed about large cash transactions, while the W-9 is used to collect taxpayer information for reporting purposes, ensuring accurate tax withholding and reporting, mainly during transactions involving services or independent contracting.

The Suspicious Activity Report (SAR) also mirrors the IRS 8300 Form in intent and purpose. Designed for financial institutions to report suspicious transactions that might signify money laundering, fraud, or other illegal activities, SARs, like the IRS 8300, play a crucial role in regulatory oversight and the prevention of financial crimes. Both documents are pivotal for law enforcement investigations and maintaining the integrity of the financial system.

Form 1099-MISC (Miscellaneous Income) shares a connection with the IRS 8300 Form in its role in tax reporting and compliance. The 1099-MISC is employed for reporting payments made in the course of business that are not wages or salaries, such as contractor payments. Although serving different specific functions, both forms are crucial for accurate financial and tax record-keeping, ensuring entities report their transactions comprehensively.

The Bank Secrecy Act (BSA) E-Filing System is related to the IRS 8300 Form in terms of regulatory compliance and the objective to counteract financial crimes. While the BSA E-Filing System is a broader platform for submitting various reports related to the Bank Secrecy Act, such as the Currency Transaction Report and Suspicious Activity Report, it shares the overall goal of the IRS 8300 to monitor and report significant cash transactions to deter and detect illicit activities.

The Foreign Bank and Financial Accounts Report (FBAR) is akin to the IRS 8300 Form, as both involve disclosure of financial activities to the authorities for oversight. The FBAR specifically requires U.S. persons to report foreign financial accounts exceeding certain thresholds to the Treasury Department, reflecting a broader scope of financial surveillance and compliance efforts similar to reasoning behind the IRS 8300, which focuses on large domestic cash transactions.

Last but not least, the Form 8938 (Statement of Specified Foreign Financial Assets) has parallels with the IRS 8300 in terms of international financial reporting. While Form 8938 requires the disclosure of sizable foreign financial assets to the IRS, part of the FATCA (Foreign Account Tax Compliance Act) regulations, it complements the domestic financial transparency sought by the IRS 8300. Both forms are critical in the broader fabric of financial reporting and compliance, aiming to mitigate tax evasion and financial crimes on both domestic and international fronts.

Dos and Don'ts

When it comes to handling the IRS 8300 form, which is used for reporting cash payments over $10,000 received in a trade or business, accuracy and diligence are key. To ensure you're completing this form correctly and in compliance with legal requirements, here’s a concise guide on the dos and don'ts you should follow:

Do:- Review the instructions carefully before filling out the form to make sure you understand all the requirements.

- Gather all necessary information, including the payer's identification, the nature of the transaction, and the amount and date of the transaction, before you start.

- Be precise and accurate in entering information to avoid any discrepancies that could trigger an audit.

- Use the IRS’s electronic filing system if possible for a faster and more secure submission.

- Keep a copy of the completed form and all related documentation for your records for at least five years, as required by law.

- Don’t delay filing the form; it must be filed within 15 days after receiving the cash payment.

- Don’t omit any required details on the form, as incomplete forms can lead to penalties.

- Don’t ignore the form’s instructions about reporting transactions that occur in close succession that are related but fall just below the $10,000 threshold, as these can still be reportable.

Remember, accurately completing the IRS Form 8300 is crucial in maintaining compliance with tax laws and regulations, as well as helping to prevent money laundering. Taking the time to carefully follow these guidelines can save your business from future legal and financial problems.

Misconceptions

Understanding the IRS 8300 form is crucial for businesses and individuals who engage in significant cash transactions. However, misconceptions about this form are common, leading to confusion and potential non-compliance. Here’s a list of nine misconceptions that need clarification:

Only cash transactions over $10,000 need to be reported. It's a common belief that only transactions exceeding $10,000 require reporting. In reality, the form must be filed for all transactions over $10,000, including those that are just a penny over.

Businesses need to report only if the transaction is exactly $10,000. This is not true. The form is required for any transaction or set of related transactions that exceed $10,000 in a 24-hour period.

All transactions are reported to the Internal Revenue Service (IRS) only. While the form is submitted to the IRS, the information is shared with the Financial Crimes Enforcement Network (FinCEN), assisting in the fight against money laundering and other financial crimes.

Personal checks count towards the $10,000 threshold. Actually, the form is used primarily for reporting cash transactions. Personal checks, wire transfers, and similar forms of payment do not need to be reported on the IRS 8300 form.

Filing IRS 8300 is voluntary. This is incorrect. Filing the form is mandatory for businesses that receive more than $10,000 in cash from a single transaction or related transactions.

Only businesses in specific industries need to file the form. While it's true that certain industries may encounter this situation more frequently, any business that receives over $10,000 in cash through a transaction or related transactions is required to file.

The form must be filed immediately after the transaction. Businesses actually have 15 days after receiving the cash payment to submit the IRS 8300 form. This provides some leeway to gather necessary information and ensure accurate reporting.

Electronic transactions are reportable on Form 8300. The focus of the IRS 8300 is on cash transactions. Electronic transactions do not fall under the reporting requirements for this specific form.

Only one transaction can trigger the need to file. This is partially true. A single transaction over $10,000 requires filing, but so do multiple transactions that collectively exceed $10,000 and appear to be connected.

Clarifying these misconceptions helps businesses and individuals better understand their obligations, ensuring that they remain compliant and avoid potential penalties. When in doubt, reviewing the official guidelines or seeking expert advice is always a prudent approach.

Key takeaways

The IRS 8300 form is a crucial document for businesses and individuals who receive cash payments over $10,000. Understanding its requirements and the process for completion can ensure compliance with tax laws and avoid potential legal issues. Below are key takeaways regarding the filling out and use of the IRS 8300 form:

- Who Must File: Any individual, company, corporation, partnership, association, trust, or estate that receives more than $10,000 in cash in a single transaction, or in related transactions, must file Form 8300.

- Types of Payments: Form 8300 is not limited to transactions in U.S. dollars but also includes transactions in foreign currency and certain monetary instruments.

- Related Transactions: Two or more payments within 24 hours are considered related transactions. Payments made over a period of more than 24 hours could be considered related if the recipient knows, or has reason to know, they are structured to avoid reporting requirements.

- Filing Deadline: The form must be filed within 15 days after receiving the payment that puts the total amount received over $10,000.

- Information Required: To complete Form 8300, provide detailed information about the transaction, the business or individual receiving the payment, and the individual or entity making the payment.

- Use of Information: The IRS and the Financial Crimes Enforcement Network (FinCEN) use the information reported on Form 8300 for tax compliance and law enforcement purposes.

- Electronic Filing: Filers can submit Form 8300 electronically, which is encouraged for quicker processing and confirmation of receipt.

- Retention of Records: A filed Form 8300, or a copy, must be retained by the filer for five years from the date of filing.

- Notification to Payers: Businesses must notify each person named on a filed Form 8300 by January 31 of the year following the transaction, informing them that the information has been reported to the IRS.

- Penalties: Penalties may be imposed for failure to file, late filing, or intentional disregard of the filing requirements.

Compliance with the IRS 8300 form requirements is essential for businesses and individuals to avoid penalties and ensure proper reporting of large cash transactions. Understanding and adhering to these key points will facilitate accurate and timely filing.

Popular PDF Documents

Irs Power of Attorney - Both the taxpayer and the appointed representative must sign Form M-2848 for it to be valid and accepted by tax authorities.

Airserv Employment - Completion and submission of the waiver agreement are necessary steps for those seeking employment with Airserv, highlighting the company's comprehensive approach to legal matters.