Get Irs 656 Form

The IRS Form 656, belonging to the Offer in Compromise booklet, stands as a beacon for taxpayers seeking relief from overwhelming tax debts, symbolizing a government attempt to meet taxpayers halfway in instances of genuine financial distress. The form allows taxpayers to propose a settlement to the IRS to pay less than the total amount owed on their tax debts, predicated on a careful scrutiny of their ability to pay. Applicants must navigate through a multifaceted process involving eligibility prerequisites, such as the filing of all required tax returns, the settlement of any required estimated tax payments for the current year, and crucially, the absence of ongoing bankruptcy proceedings which would render them ineligible. The form further details the process of applying, key considerations including the taxpayer’s future refunds, and the implications of a Notice of Federal Tax Lien. Taxpayers are guided on selecting payment terms for their offer, which could either be a lump sum or periodic payments, alongside a mandatory application fee, subject to exemptions for those meeting low-income certifications. The booklet underscores the importance of continued compliance with tax obligations during and after the offer process and elaborates on scenarios that might lead to the return or rejection of the offer. Additionally, it links to resources such as the Pre-Qualifier tool for preliminary eligibility assessment and the Taxpayer Advocate Service for those needing assistance or facing undue hardship because of IRS actions. By navigating these stipulations, taxpayers find a potential avenue for resolving tax liabilities in a manner that respects their limited financial capacity while ensuring that the IRS recovers a fair and collectible amount.

Irs 656 Example

Form 656 Booklet |

|

Offer in |

|

Compromise |

|

CONTENTS |

|

■ What you need to know |

1 |

■ Paying for your offer |

3 |

■ How to apply |

4 |

■ Completing the application package |

5 |

■ Important information |

6 |

■Removable Forms - Form

Collection Information Statement for Businesses; Form 656, Offer in |

|

Compromise |

7 |

■ Application Checklist |

29 |

IRS contact information

If you want to see if you qualify for an offer in compromise before filling out the paperwork, you may use the Offer in Compromise

If you have questions regarding qualifications for an offer in compromise, please call our

Taxpayer resources

The Taxpayer Advocate Service (TAS) is an independent organization within the Internal Revenue Service that helps taxpayers and protects taxpayer rights. TAS helps taxpayers whose problems with the IRS are causing financial difficulties, who've tried but haven't been able to resolve their problems with the IRS or believe an IRS system or procedure isn't working as it should. The service is free. Your local advocate's number is in your local directory and at taxpayeradvocate.irs.gov. You can also call us at

WHAT YOU NEED TO KNOW

What is an Offer? |

An Offer in Compromise (offer) is an agreement between you (the taxpayer) and |

|

|

the IRS that settles a tax debt for less than the full amount owed. The offer |

|

|

program provides eligible taxpayers with a path toward paying off their tax debt. |

|

|

The ultimate goal is a compromise that suits the best interest of both the taxpayer |

|

|

and the IRS. Generally, you must |

make an appropriate offer based on what the |

|

IRS considers your true ability to |

pay. |

|

Submitting an application does not ensure that the IRS will accept your offer. |

|

|

It begins a process of evaluation and verification by the IRS, taking into |

|

|

consideration any special circumstances that may affect your ability to pay. |

|

|

This booklet will lead you through a series of steps to help you calculate an |

|

|

appropriate offer based on your assets, income, expenses, and future earning |

|

|

potential. The application requires you to describe your financial situation in detail, |

|

|

so before you begin, make sure you have the necessary information and |

|

|

documentation. |

|

Are You Eligible? |

Before your offer can be considered, you must (1) file all tax returns you are legally |

|

|

required to file, (2) have received a bill for at least one tax debt included on your |

|

|

offer, (3) make all required estimated tax payments for the current year, and (4) |

|

|

make all required federal tax deposits for the current quarter if you are a business |

|

|

owner with employees. The IRS will immediately return your offer without further |

|

|

consideration if you have not filed all legally required tax returns. |

|

|

Note: If it is determined you have not filed all tax returns you are legally |

|

|

required to file, the IRS will apply any initial payment you sent with your offer |

|

|

to your tax debt and return both your offer and application fee to you. You |

|

|

cannot appeal this decision. |

|

Bankruptcy, Open Audit or |

If you or your business is currently in an open bankruptcy proceeding, you are not |

|

Innocent Spouse Claim |

eligible to apply for an offer. Any resolution of your outstanding tax debts generally |

|

|

must take place within the context of your bankruptcy proceeding. |

|

|

If you are not sure of your bankruptcy status, contact the Centralized Insolvency |

|

|

Operation at |

|

|

and/or Taxpayer Identification Number. |

|

|

Resolve any open audit or outstanding innocent spouse claim issues before |

|

|

you submit an offer. |

|

Can You Pay in Full? |

Generally, the IRS will not accept an offer if you can pay your tax debt in full |

|

|

through an installment agreement or equity in assets. |

|

|

Note: Adjustments or exclusions, which may be considered during the offer |

|

|

investigation, such as allowance of $1,000 to a bank balance or $3,450 against the |

|

|

value of a car, are only applied if you are an individual and after it is determined |

|

|

that you cannot pay your tax debt in full. |

|

Your Future Tax Refunds |

The IRS will keep any refund, including interest, for tax periods extending through |

|

|

the calendar year that the IRS accepts the offer. For example, the IRS accepts |

|

|

your offer in 2020 and you file your 2020 Form 1040 on April 15, 2021 showing a |

|

|

refund; the IRS will apply your refund to your tax debt. The refund is not |

|

|

considered as a payment toward your offer. |

|

Doubt as to Liability |

If you have a legitimate doubt that you owe part or all of the tax debt, complete and |

|

|

submit a Form |

|

|

Form |

|

|

FORM |

|

Note: Do not submit both an offer under Doubt as to Liability and an offer under Doubt as to Collectibility or Effective Tax Administration at the same time. You must resolve any doubt you owe part or all of the tax debt before submitting an offer based on your ability to pay.

1

Notice of Federal Tax Lien |

A lien is a legal claim against all your current and future property. When you don’t |

|

pay your first bill for taxes due, a lien is created by law and attaches to your |

|

property. A Notice of Federal Tax Lien (NFTL) provides public notice to creditors. |

|

The IRS files the NFTL to establish priority of the IRS claim versus the claims of |

|

certain other creditors. The IRS may file a NFTL at any time. If the tax lien(s) has/ |

|

have not been released, the IRS may be entitled to any proceeds from the sale of |

|

property subject to the lien(s). You may be entitled to file an appeal under the |

|

Collection Appeals Program (CAP) before this occurs or request a Collection Due |

|

Process hearing after this occurs. |

|

Note: A Notice of Federal Tax Lien (NFTL) will not be filed on any individual shared |

|

responsibility payment under the Affordable Care Act. |

Trust Fund Taxes |

If your business owes liabilities that include trust fund taxes, the IRS may hold |

|

responsible individuals liable for the trust fund portion of the tax pursuant to |

|

applicable law. Trust fund taxes are the money withheld from an employee's |

|

wages, such as income tax, Social Security, and Medicare taxes. If the IRS enters |

|

into a compromise with an employer for a portion of the trust fund tax liability, the |

|

remainder of the trust fund taxes must be collected from the responsible parties. |

|

You are not eligible for consideration of an offer unless the trust fund portion of the |

|

tax is paid, or the IRS has made the Trust Fund Recovery Penalty determination(s) |

|

on all potentially responsible individual(s). However, if you are submitting the offer |

|

as a victim of payroll service provider fraud or failure, the trust fund recovery |

|

penalty assessment discussed above is not required prior to submitting the offer. |

Other Important Facts |

Each and every taxpayer has a set of fundamental rights they should be aware of |

|

when interacting with the IRS. Explore your rights and our obligations to protect |

|

them. For more information on your rights as a taxpayer, go to http://www.irs.gov/ |

|

|

|

Penalties and interest will continue to accrue. |

|

After you submit your offer, you must continue to timely file and pay all required tax |

|

returns, estimated tax payments, and federal tax payments for yourself and any |

|

business in which you have an interest. Failure to meet your filing and payment |

|

responsibilities during consideration of your offer will result in the IRS returning |

|

your offer. If the IRS accepts your offer, you must continue to stay current with all |

|

tax filing and payment obligations through the fifth year after your offer is accepted |

|

(including any extensions). |

|

Note: If you have filed your tax returns but you have not received a bill for at |

|

least one tax debt included on your offer, your offer and application fee may |

|

be returned and any initial payment sent with your offer will be applied to |

|

your tax debt. To prevent the return of your offer, include a complete copy of |

|

any tax return filed within 12 weeks of this offer submission. |

|

The IRS can't process your offer if the IRS referred your case, or cases, involving |

|

all of the liabilities identified in the offer to the Department of Justice. In addition, |

|

the IRS cannot compromise any tax liability arising from a restitution amount |

|

ordered by a court or a tax debt reduced to judgment. Furthermore, the IRS will not |

|

compromise any IRC § 965 tax liability for which an election was made under IRC |

|

§ 965(i). You cannot appeal this decision. |

|

Note: Any offer containing a liability for which payment is being deferred under IRC |

|

§ 965(h)(1) can only be processed for investigation if an acceleration of payment |

|

under section 965(h)(3) and the regulations thereunder has occurred and no |

|

portion of the liability to be compromised resulted from entering into a transfer |

|

agreement under section 965(h)(3). |

|

The law requires the IRS to make certain information from accepted offers |

|

available for public inspection and review. Find instructions to request a public |

|

inspection file at www.IRS.gov keyword "OIC". |

2

|

The IRS may levy your assets up to the time the IRS official signs and |

|

acknowledges your offer as pending. In addition, the IRS may keep any proceeds |

|

received from the levy. If your assets are levied after your offer is submitted and |

|

pending evaluation, immediately contact the IRS employee whose name and |

|

phone number are listed on the levy. |

|

If you currently have an approved installment agreement, you will not be required |

|

to make your installment agreement payments while your offer is being |

|

considered. If your offer is not accepted and you have not incurred any additional |

|

tax debt, the IRS will reinstate your installment agreement. |

|

|

PAYING FOR YOUR OFFER |

|

Application Fee |

Offers require a $205 application fee. |

|

Exception: If you are an individual and meet the |

|

guidelines, there is no requirement to send any money with your offer. You |

|

are considered an individual if you are seeking compromise of a liability for which |

|

you are personally responsible, including any liability you incurred as a sole |

|

proprietor. |

Payment Options |

You must select a payment option and include the initial payment with your offer. |

|

The amount of the initial payment and subsequent payments will depend on the |

|

total amount of your offer and which of the following payment options you choose: |

|

Lump Sum Cash: This option requires 20% of the total offer amount to be paid |

|

with the offer and the remaining balance paid in 5 or fewer payments within 5 or |

|

fewer months of the date your offer is accepted. |

|

Periodic Payment: This option requires you to make the first payment with the |

|

offer and the remaining balance paid in monthly payments within 6 to 24 months, |

|

in accordance with your proposed offer terms. |

|

Note: Under the periodic payment option, you must continue to make |

|

monthly payments while the IRS is evaluating your offer. If you fail to make |

|

these payments at any time prior to receiving a final decision letter, the IRS will |

|

return your offer. You cannot appeal this decision. Total payments must equal the |

|

total offer amount. |

|

Reminder: The initial payment and monthly payments are not required if you meet |

|

the |

|

Generally, payments made on an offer will not be returned. You may make a |

|

deposit, as described in Form 656, Section 5, which may be returned if the offer is |

|

not accepted. If the IRS accepts your offer, your payments made during the offer |

|

process, including any money designated as a deposit, will be applied to your offer |

|

amount. |

|

If you do not have sufficient cash to pay for your offer, you may need to consider |

|

borrowing money from a bank, friends, and/or family. Other options may include |

|

borrowing against or selling other assets. |

|

If you are an individual, use the OIC |

|

at http://irs.treasury.gov/oic_pre_qualifier/ to assist in determining a starting |

|

point for your offer amount. |

|

Note: You may not pay your offer amount with an expected or current tax |

|

refund, money already paid, funds attached by any collection action, or |

|

anticipated benefits from a capital or net operating loss. If you are planning to |

|

use your retirement savings from an IRA or 401k plan, you may have future tax |

|

debt as a result. Contact the IRS or your tax advisor before taking this action. |

3

HOW TO APPLY

Application Process |

The application must include: |

|

• Form 656, Offer in Compromise |

|

• Completed and signed Form |

|

Wage Earners and |

|

• Completed and signed Form |

|

Businesses, if applicable |

|

• $205 application fee, unless you meet |

|

• Initial offer payment based on the payment option you choose, unless you |

|

meet |

|

Note: Your offer(s) cannot be considered without the completed and signed |

|

Form(s) 656, |

|

documentation. |

If You and Your Spouse Owe |

If you and your spouse have joint tax debt(s) and you or your spouse are also |

Joint and Separate Tax Debts |

responsible for separate tax debt(s) (including Trust Fund Recovery Penalty), you |

|

will each need to send in a separate Form 656. You will complete one Form 656 |

|

for yourself listing all your joint and any separate tax debts and your spouse will |

|

complete one Form 656 listing all his or her joint tax debt(s) plus any separate tax |

|

debt(s), for a total of two Forms 656. |

|

If you and your spouse or |

|

spouse does not want to be part of the offer, you may submit a Form 656 to |

|

compromise your responsibility for the joint tax debt. |

|

Each Form 656 will require the $205 application fee and initial payment |

|

unless you are an individual and meet the |

|

guidelines. |

If You Owe Individual and |

If you have individual and business tax debt that you wish to compromise, you will |

Business Tax Debt |

need to send in two Forms 656. Complete one Form 656 for your individual tax |

|

debts and one Form 656 for your business tax debts. Each Form 656 will require |

|

the $205 application fee and initial payment. |

|

Note: A business is defined as a corporation, partnership, or any business that is |

|

operated as other than a |

|

individual's share of a partnership debt. The partnership must submit its own offer |

|

based on the partnership's and partners' ability to pay. |

4

COMPLETING THE APPLICATION PACKAGE

Step 1 – Gather Your Information

Step 2 – Fill out Form

To calculate an offer amount, you will need to gather information about your financial situation, including cash, investments, available credit, assets, income, and debt.

You will also need to gather information about your household's gross monthly income and average expenses. The entire household includes all those in addition to yourself who contribute money to pay expenses relating to the household such as, rent, utilities, insurance, groceries, etc. This is necessary for the IRS to accurately evaluate your offer. The IRS may also use this to determine your share of the total household income and expenses.

In general, the IRS will not consider expenses for tuition for private schools, college expenses, charitable contributions, and other unsecured debt payments as part of the expense calculation.

Fill out Form

Step 3 – Fill out Form

Fill out Form

Step 4 – Attach Required |

You will need to attach supporting documentation with Form(s) |

Documentation |

|

|

copies of all required attachments. Do not send original documents. |

Step 5 – Fill out Form 656, Offer in Compromise

Step 6 – Include Initial Payment and $205 Application Fee

Step 7 – Mail the Application Package

Fill out Form 656. The Form 656 identifies the tax years and type of tax you would like to compromise. It also identifies your offer amount and the payment terms.

Include a personal check, cashier's check, or money order for your initial payment based on the payment option you selected (20% of the offer amount for a lump sum cash offer or the first month's payment for a periodic payment offer). Generally, initial payments will not be returned but will be applied to your tax debt if your offer is not accepted.

Include a separate personal check, cashier's check, or money order for the application fee. Make both payments (in U.S. dollars) payable to the “United States Treasury”.

You may choose to make your initial offer payment and application fee through the Electronic Federal Tax Payment System (EFTPS).

Reminder: If you meet the

Make a copy of your application package and keep it for your records.

Mail the completed application package to the appropriate IRS facility. See page 29, Application Checklist, for details.

Note: If you are working with an IRS employee, let him or her know you are sending or have sent an offer to compromise your tax debt(s).

5

IMPORTANT INFORMATION

After You Mail Your Application: We will contact you after we receive and review your offer application. Promptly reply to any requests for additional information within the time frame specified. Failure to reply timely will result in the return of your offer without appeal rights.

If the IRS accepts your offer, you must continue to timely file all required tax returns and timely pay all estimated tax payments and federal tax payments that become due in the future. If you fail to timely file and timely pay any tax obligations that become due within the five years after your offer acceptance (including any extensions) your offer may be defaulted. If the IRS defaults your offer, you will be liable for the original tax debt, less payments made, and all accrued interest and penalties. An offer does not stop the accrual of interest and penalties. Please note that if your final payment is more than the agreed amount, the IRS will not return the money but will apply it to your tax debt.

In addition, the IRS may default your offer if you fail to promptly pay any tax debts assessed after acceptance of your offer for any tax years prior to acceptance that were not included in your original offer.

6

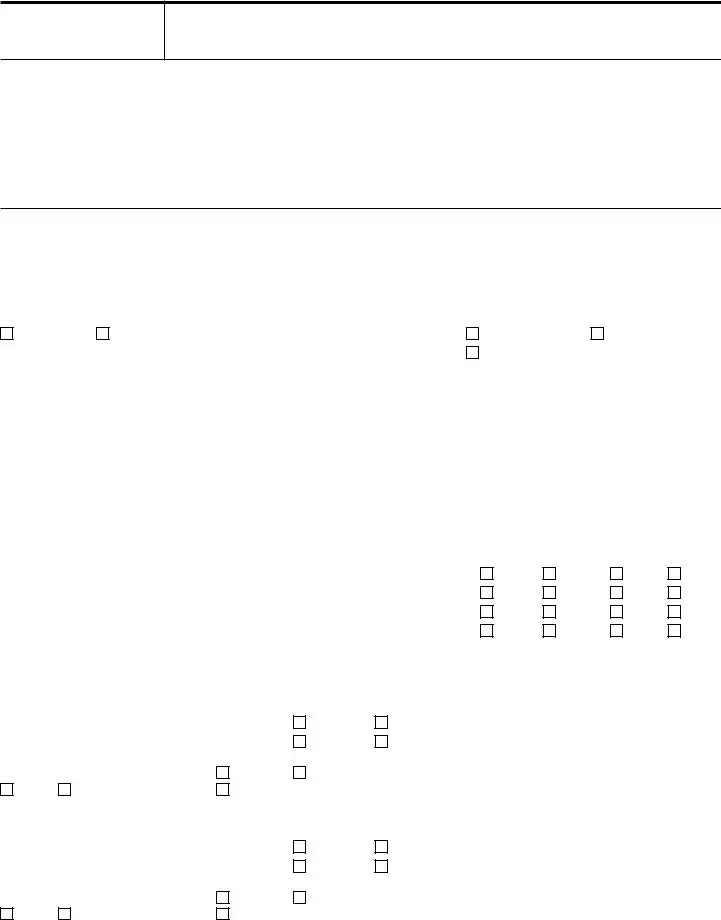

Form

(April 2021)

Department of the Treasury — Internal Revenue Service

Collection Information Statement for Wage Earners and

Use this form if you are

►An individual who owes income tax on a Form 1040, U.S. Individual Income Tax Return

►An individual with a personal liability for Excise Tax

►An individual responsible for a Trust Fund Recovery Penalty

►An individual who is

►An individual who is personally responsible for a partnership liability (only if the partnership is submitting an offer)

►An individual who is submitting an offer on behalf of the estate of a deceased person

Note: Include attachments if additional space is needed to respond completely to any question. This form should only be used with the Form 656, Offer in Compromise.

Section 1 |

|

|

|

|

Personal and Household Information |

|

|

|

|

|

||||||

Last name |

|

First name |

|

|

Date of birth (mm/dd/yyyy) |

|

|

Social Security Number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

- |

Marital status |

|

Home physical address (street, city, state, ZIP code) |

Do you |

|

|

|

|

|

||||||||

|

Unmarried |

Married |

|

|

|

|

|

|

|

|

Own your home |

|

|

|

Rent |

|

If married, date of marriage (mm/dd/yyyy) |

|

|

|

|

|

|

|

|

Other (specify e.g., share rent, live with relative, etc.) |

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

County of residence |

|

Primary phone |

|

|

Home mailing address (if different from above or post office box number) |

|||||||||||

|

|

|

|

( |

) |

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Secondary phone |

|

|

FAX number |

|

|

|

|

|

|

|

|

|

|

|||

( |

) |

- |

|

( |

) |

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Provide information about your spouse. |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Spouse's last name |

|

Spouse's first name |

|

Date of birth (mm/dd/yyyy) |

|

|

Social Security Number |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

- |

Provide information for all other persons in the household or claimed as a dependent. |

|

|

|

|

|

|

|

|||||||||

|

|

Name |

|

|

|

Age |

|

Relationship |

|

Claimed as a dependent |

Contributes to |

|||||

|

|

|

|

|

|

|

on your Form 1040 |

|

household income |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Section 2 |

|

|

|

Employment Information for Wage Earners |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete this section if you or your spouse are wage earners and receive a Form

Your employer’s name |

Pay period |

Weekly |

Employer’s address (street, city, state, ZIP code) |

||||

|

|

|

Monthly |

Other |

|

|

|

|

|

|

|

|

|||

Do you have an ownership interest in this |

If yes, check the business interest that applies |

|

|

||||

business |

|

Partner |

Sole proprietor |

|

|

||

Yes |

No |

Officer (complete Form |

|

|

|||

|

|

|

|

|

|

||

Your occupation |

How long with this employer |

|

|

|

|

||

|

|

|

(years) |

(months) |

|

|

|

|

|

|

|

|

|

||

Spouse’s employer's name |

Pay period |

Weekly |

Employer’s address (street, city, state, ZIP code) |

||||

|

|

|

Monthly |

Other |

|

|

|

|

|

|

|

||||

Does your spouse have an ownership |

If yes, check the business interest that applies |

|

|

||||

interest in this business |

Partner |

Sole proprietor |

|

|

|||

Yes |

No |

Officer (complete Form |

|

|

|||

|

|

|

|

|

|

||

Spouse's occupation |

How long with this employer |

|

|

|

|

||

|

|

|

(years) |

(months) |

|

|

|

|

|

|

|

|

|

||

Catalog Number 55896Q |

|

www.irs.gov |

|

|

Form |

|

|

Page 2

Section 3 |

Personal Asset Information |

|

|

Use the most current statement for each type of account, such as checking, savings, money market and online accounts, stored value cards (such as a payroll card from an employer), investment, retirement accounts (IRAs, Keogh, 401(k) plans, stocks, bonds, mutual funds, certificates of deposit) and virtual currency (such as Bitcoin, Ripple, Ethereum, etc.), life insurance policies that have a cash value, and safe deposit boxes. Asset value is subject to adjustment by IRS based on individual circumstances. Enter the total amount available for each of the following (if additional space is needed include attachments).

Round to the nearest dollar. Do not enter a negative number. If any line item is a negative number, enter "0".

Cash and Investments (domestic and foreign)

|

Cash |

Checking |

Savings |

Money Market Account/CD |

Online Account |

Stored Value Card |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bank name |

|

|

|

|

|

|

|

|

|

|

|

Account number |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1a) |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Checking |

|

Savings |

Money Market Account/CD |

Online Account |

Stored Value Card |

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bank name |

|

|

|

|

|

|

|

|

|

|

|

Account number |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1b) |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total of bank accounts from attachment |

(1c) |

$ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Add lines (1a) through (1c) minus ($1,000) = |

(1) |

$ |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment account |

|

|

Stocks |

|

|

Bonds |

|

Other |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name of Financial Institution |

|

|

|

|

|

Account number |

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current market value |

|

|

|

|

|

|

|

|

|

|

|

Minus loan balance |

|

|

|

|

|||||||

$ |

|

|

|

|

|

|

X .8 = $ |

|

|

|

|

|

|

– $ |

|

|

|

= |

(2a) |

$ |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Investment account |

|

|

Stocks |

|

|

Bonds |

|

Other |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Name of Financial Institution |

|

|

|

|

|

Account number |

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Current market value |

|

|

|

|

|

|

|

|

|

|

|

Minus loan balance |

|

|

|

|

|||||||

$ |

|

|

|

|

|

|

X .8 = $ |

|

|

|

|

|

|

– $ |

|

|

|

= |

(2b) |

$ |

|||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Virtual currency |

|

|

Name of virtual currency |

|

Email address used to |

Location(s) of virtual |

|

|

|

|||||||||||||

|

|

|

|

|

wallet, exchange or digital |

currency |

|

|

|

||||||||||||||

Type of virtual currency |

|

|

|

|

|||||||||||||||||||

|

currency exchange (DCE) |

currency exchange or DCE |

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Current market value in U.S. dollars as of today |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

$ |

|

|

|

|

|

|

X .8 = $ |

|

|

|

|

|

|

|

|

|

|

|

= |

(2c) |

$ |

||

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

Total investment accounts from attachment. [current market value minus loan balance(s)] |

(2d) |

$ |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Add lines (2a) through (2d) =

(2) $

Retirement account |

401K |

IRA |

Other |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Financial Institution |

|

|

|

Account number |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Current market value |

|

|

|

|

|

Minus loan balance |

|

|

|

|||

$ |

|

|

X .8 = $ |

|

|

|

– $ |

|

= |

(3a) |

$ |

|

|

|

|

|

|||||||||

|

Total of retirement accounts from attachment. [current market value X .8 minus loan balance(s)] |

(3b) |

$ |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Add lines (3a) through (3b) =

(3) $

Note: Your reduction from current market value may be greater than 20% due to potential tax consequences/withdrawal penalties.

Cash value of Life Insurance Policies |

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Insurance Company |

Policy number |

|

|

|

||

|

|

|

|

|

|

|

Current cash value |

Minus loan balance |

|

|

|

||

$ |

|

– $ |

|

= |

(4a) |

$ |

|

|

|

|

|

||

Total cash value of life insurance policies from attachment |

Minus loan balance(s) |

|

|

|

||

$ |

|

– $ |

|

= |

(4b) |

$ |

|

|

|

|

|

|

|

|

|

|

Add lines (4a) through (4b) = |

(4) |

$ |

|

|

|

|

|

|||

Catalog Number 55896Q |

www.irs.gov |

|

Form |

|||

Document Specifics

| Facts | Details |

|---|---|

| What is Form 656 | An agreement proposal between the taxpayer and the IRS to settle a tax debt for less than the full amount owed. |

| Eligibility Requirements | Taxpayers must file all required tax returns, have received a bill for at least one tax debt included on the offer, make all required estimated tax payments for the current year, and all required federal tax deposits for business owners with employees. |

| Pre-Qualifier Tool | The IRS offers a Pre-Qualifier tool online to help taxpayers determine eligibility for an offer in compromise before applying. |

| Application Fee | A $205 application fee is required, except for individuals meeting Low-Income Certification guidelines who are not required to send any money with their offer. |

| Payment Options | Lump Sum Cash (20% upfront with the balance paid in 5 or fewer payments within 5 months) or Periodic Payment (first payment with offer and the remaining balance paid in monthly payments within 6 to 24 months). |

| Effect on Future Tax Refunds | The IRS will keep any refund, including interest, for tax periods extending through the calendar year that the IRS accepts the offer. The refund is not considered as a payment toward the offer. |

| Public Inspection | The law requires the IRS to make certain information from accepted offers available for public inspection and review. |

Guide to Writing Irs 656

Filling out Form 656, the Offer in Compromise, is a crucial step for taxpayers seeking a resolution for their tax liabilities. This form allows taxpayers to settle their tax debt for less than the full amount owed, if they meet specific eligibility criteria. It involves a detailed process to ensure all necessary information and documentation is accurately presented. The steps outlined below guide you through completing this form correctly. Before you begin, ensure you have gathered all required financial documents and understand your tax situation thoroughly. This process requires patience and precision, but it's essential for exploring all possibilities of resolving your tax obligations.

- Review the entire Form 656 Booklet to fully understand the Offer in Compromise process, requirements, and eligibility.

- Gather all necessary financial documents, including income statements, bank statements, and expenses, as these will inform the details of your offer.

- Ensure you have filed all required tax returns up to date, as this is a prerequisite to qualify for an Offer in Compromise.

- Use the IRS Offer in Compromise Pre-Qualifier tool online to assess your eligibility and get an estimate of an acceptable offer amount.

- Complete Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses to provide a detailed financial statement required for the Offer in Compromise. This includes information on assets, liabilities, income, and expenses.

- Fill out Form 656, starting from Section 1, by providing your personal information, including your name, social security number, address, and tax periods for which the offer is made.

- Select the reason for your offer on the form, whether it is based on doubt as to collectibility, effective tax administration, or doubt as to liability.

- Choose your payment terms on Form 656, deciding between a Lump Sum Cash offer or a Periodic Payment offer, and calculate your initial payment accordingly.

- Include the $205 application fee with your offer unless you meet the Low-Income Certification guidelines, which would exempt you from this fee. Also, include the initial payment as per your chosen payment option.

- Review your completed forms and attached documents to ensure accuracy and completeness. Use the Application Checklist provided to verify all parts are included.

- Mail your completed application package, including Form 656, Form 433-A (OIC)/Form 433-B (OIC), and all supporting documentation, to the IRS at the address provided in the instructions.

After submitting your Offer in Compromise, the IRS will review your application to determine your eligibility and the adequacy of the offer amount. During this review process, the IRS may request additional documentation or clarification. It's important to respond to any IRS inquiries promptly to avoid delays in the processing of your offer. If your offer is accepted, you must adhere to the payment terms and stay compliant with all filing and payment obligations to prevent the offer from being revoked. Remember, the goal is to settle your tax debt in a way that is manageable for you and acceptable to the IRS, allowing you to move forward free from overwhelming tax liabilities.

Understanding Irs 656

What is an Offer in Compromise (OIC)?

An Offer in Compromise is a program that allows taxpayers to settle their tax debt for less than the full amount owed. It is designed for taxpayers who are unable to pay their full tax liability, or doing so would create financial hardship. The aim is to agree on an amount that is doable for the taxpayer, while also being acceptable to the IRS.

Who is eligible for an OIC?

Eligibility for an OIC requires that you have filed all required tax returns, received a bill for at least one tax debt included in the offer, made all estimated tax payments for the current year, and, if applicable, made all required federal tax deposits for the current quarter. If any required tax returns have not been filed, the IRS will return the OIC application.

Can I apply for an OIC if I am in bankruptcy or have an open audit?

No, if you or your business is currently in an open bankruptcy proceeding, you are not eligible for an OIC. Likewise, you should resolve any open audits or outstanding innocent spouse claims before submitting an OIC application. These situations must be resolved within their own contexts before the IRS can consider an OIC.

What if I can pay the full amount through another method?

The IRS generally will not accept an OIC if you can pay your tax debt in full through an installment agreement or by using the equity in your assets. However, certain allowances and exclusions may be applied to your case during the IRS’s evaluation of your offer.

What happens to future tax refunds if my OIC is accepted?

Any tax refunds due to you up to the calendar year the IRS accepts your OIC will be applied to your tax debt. These refunds are not considered part of your OIC payment.

What is Doubt as to Liability?

If you believe that you do not owe part or all of the tax debt, you can submit a Form 656-L, Offer in Compromise (Doubt as to Liability). This form is specifically for taxpayers who have a legitimate doubt about the amount of tax debt owed.

What are the payment options for an OIC?

- Lump Sum Cash: Requires 20% of the total offer amount with the application, with the balance paid in five or fewer payments within five months after acceptance.

- Periodic Payment: Requires the first payment with the application and the balance paid within 6 to 24 months, according to proposed offer terms. Monthly payments must be made while the IRS evaluates the offer.

Note: There is a $205 application fee for an OIC, but individuals who meet Low-Income Certification guidelines are exempt from this fee and the initial payment requirements.

Can I appeal a decision on my OIC?

If your OIC is rejected, you have the right to appeal the decision. However, certain actions, like failing to make required payments while your offer is being evaluated, cannot be appealed if they result in your offer being returned.

Common mistakes

When individuals attempt to navigate the complexities of the IRS Form 656, the Offer in Compromise application, they often encounter challenges. To help guide those who are preparing to tackle this form, it's crucial to highlight some common mistakes to avoid:

Not filing all required tax returns prior to submission. The IRS demands that all necessary tax returns are filed before they will consider an Offer in Compromise.

Overlooking the need to stay current with estimated tax payments for the current year and, if applicable for business owners, making necessary federal tax deposits for the current quarter.

Including a tax debt in the offer that has not yet been billed. The IRS specifies that at least one tax debt must be formally billed to be considered for an offer.

Applying while in an open bankruptcy proceeding. As bankruptcy provides its own mechanisms for handling debts, those in active bankruptcy are not eligible for an Offer in Compromise.

Failure to resolve any open audit issues or outstanding innocent spouse claims, which need to be settled before submitting the offer.

Misunderstanding the eligibility regarding tax lien discharges. If a Notice of Federal Tax Lien has been filed, it may influence the outcome of the offer.

Attempting to include taxes that are not eligible for compromise, such as certain trust fund taxes without addressing the trust fund recovery penalty assessments.

Not correctly utilizing the Offer in Compromise Pre-Qualifier tool or misunderstanding its purpose in providing a preliminary offer amount for the IRS's consideration.

Neglecting to send the required $205 application fee or the initial payment with the offer, unless qualified for the Low-Income Certification exemption.

Choosing an inappropriate payment option or failing to adhere to the payment terms selected for the offer, which can result in the offer being returned.

Additionally, the complexities of the Offer in Compromise process also include recognizing that:

Future tax refunds may be applied to your debt: For any tax year that ends before your offer is accepted, the IRS will keep any tax refunds.

Penalties and interest continue to accrue: Until an offer is accepted, penalties and interest on the outstanding tax debt will not pause.

Submission of an offer doesn't guarantee acceptance: The IRS evaluates various factors including ability to pay, income, expenses, and asset equity.

Maintaining compliance post-acceptance is critical: After acceptance, it is imperative to stay current with all filing and payment obligations to avoid defaulting on the offer.

Understanding these potential pitfalls can be instrumental in preparing an Offer in Compromise that accurately reflects an individual's financial situation and increases the likelihood of acceptance by the IRS.

Documents used along the form

When navigating the complexities of resolving tax debts through an Offer in Compromise (OIC) with the IRS, understanding and preparing the required forms and documents is crucial. The IRS Form 656 is at the core of the OIC process, offering a pathway for qualified individuals and businesses to settle tax debts for less than the full amount owed. To support an OIC application, several additional forms and documents are commonly used to provide comprehensive financial details, ensure compliance, and meet the program's requirements. Here's a closer look at these essential forms and documents.

- Form 433-A (OIC) – Collection Information Statement for Wage Earners and Self-Employed Individuals: Provides the IRS with detailed information about the applicant's financial situation, including income, expenses, assets, and liabilities.

- Form 433-B (OIC) – Collection Information Statement for Businesses: Similar to Form 433-A but tailored for businesses, offering a snapshot of the business's financial health through details on assets, liabilities, income, and expenses.

- Form 656-L – Offer in Compromise (Doubt as to Liability): Used when the applicant believes they do not owe the tax debt or the amount assessed is incorrect. It provides a separate avenue within the OIC process for disputing the liability.

- Form 2848 – Power of Attorney and Declaration of Representative: Authorizes an individual, such as an attorney or accountant, to represent the taxpayer before the IRS, allowing them to make inquiries, provide information, and negotiate the OIC.

- Form 8821 – Tax Information Authorization: Grants a third party the permission to access and review the applicant's tax information, helpful for preparers assessing the situation and for family members or other parties assisting with the case.

- Form 4506-T – Request for Transcript of Tax Return: Allows taxpayers to request previous tax returns and income information, which may be necessary to substantiate financial claims made in the OIC application.

- IRS Publication 1 – Your Rights as a Taxpayer: Provides information on a taxpayer's rights throughout the IRS interaction, including the OIC process, essential for ensuring fair treatment and understanding the procedural safeguards in place.

- IRS Publication 594 – The IRS Collection Process: Offers insight into the collection process for taxpayers who owe taxes, including options for resolving tax debt and the role of the OIC within these procedures.

- IRS Notice CP 90 – Final Notice, Notice of Intent to Levy and Notice of Your Right to a Hearing: Frequently involved in cases leading to an OIC, as it indicates the IRS's intention to levy assets, prompting many taxpayers to seek resolution through an OIC.

Successfully navigating the Offer in Compromise application requires careful attention to detail and thorough preparation of all relevant forms and documentation. The forms listed above are often crucial in establishing the taxpayer's financial situation, ensuring compliance with tax laws, and presenting a compelling case to the IRS for why an offer should be accepted. It's essential to understand the purpose and requirements of each document in the context of the OIC process to move forward with confidence towards resolving one's tax liabilities.

Similar forms

The Form 433-A (OIC), Collection Information Statement for Wage Earners and Self-Employed Individuals, bears resemblance to the IRS 656 form in several aspects. Both documents require detailed financial information to assess the taxpayer's ability to pay their tax debt. While Form 656 initiates a request for an Offer in Compromise, Form 433-A provides the IRS with the necessary financial details to evaluate the taxpayer’s offer. This evaluation is crucial, as it determines the feasibility of the requested compromise by analyzing the taxpayer’s income, expenses, and asset equity.

Form 433-B (OIC), Collection Information Statement for Businesses, is another document similar to the IRS 656 form, targeted towards businesses seeking an Offer in Compromise. Like its counterpart for individuals, this form collects financial data but focuses on the business’s financial health, including assets, liabilities, and operational expenses. The completion of this form is pivotal for businesses to illustrate their incapability to fulfill their full tax liabilities, thereby necessitating the consideration for an Offer in Compromise encapsulated within Form 656.

Form 656-L, Offer in Compromise (Doubt as to Liability), shares a foundational purpose with Form 656; both aim to resolve tax liabilities under specific conditions. However, Form 656-L is distinct as it caters to taxpayers disputing the accuracy of the tax debt imposed on them, endeavoring for an adjustment on the grounds of doubt regarding the liability amount. While Form 656 addresses the ability to pay, Form 656-L centers on disputing the actual tax debt, reflecting different facets of resolving tax liabilities with the IRS.

IRS Form 1040, the U.S. Individual Income Tax Return, although primarily a tax filing document, indirectly relates to Form 656 as part of the prerequisite conditions. Before considering an Offer in Compromise through Form 656, taxpayers must ensure they’ve filed all required tax returns, including Form 1040. This compliance serves as a critical initial step in demonstrating the taxpayer’s commitment to rectifying their tax situation, thereby affecting the eligibility and assessment process of their offer.

The Application for Reduced User Fee for Installment Agreements similarly links with the concept of alleviating the taxpayer's financial burden, akin to Form 656. Though this application focuses on reducing the fee for establishing a payment plan, it aligns with the Offer in Compromise’s objective of making tax liabilities manageable for financially constrained taxpayers. Both documents facilitate the IRS’ engagement in solutions aimed at recovery of debts in consideration of the taxpayer's ability to fulfill their obligations.

IRS Form 2848, Power of Attorney and Declaration of Representative, complements the aim of Form 656, albeit through a different mechanism. Taxpayers looking to submit an Offer in Compromise may utilize Form 2848 to authorize a tax professional to act on their behalf in negotiations and communications with the IRS. This legal representation can be pivotal in effectively presenting and managing an Offer in Compromise, demonstrating the forms’ collaborative roles in addressing tax liabilities.

Form 8821, Tax Information Authorization, while not directly part of the Offer in Compromise process, supports it by allowing designated individuals to access a taxpayer’s information, which can be instrumental in preparing a comprehensive and accurate Form 656. By enabling a tax professional to review tax histories and liabilities, Form 8821 assists in gathering the necessary backdrop and details for a viable Offer in Compromise.

The Collection Information Statement for Wage Earners and Self-Employed Individuals, without a specific form number akin to Form 433-A (OIC), serves a parallel purpose. It underscores the necessity for taxpayers to comprehensively disclose their financial landscape. This detailed disclosure is essential for the IRS to ascertain the taxpayer’s capability to settle their tax debt, echoing the informational requirements posed by Form 656 in the Offer in Compromise process.

Lastly, the Department of Justice’s role in tax liability settlements, though not encapsulated in a singular form, intersects with the conditions outlined in Form 656 regarding the ineligibility for an Offer in Compromise during ongoing Department of Justice proceedings. This contextual similarity underlines the broader regulatory and procedural framework within which tax liabilities and compromises are navigated, demarcating the boundaries and possibilities for tax debt resolution efforts.

Dos and Don'ts

When engaging in the process of filling out the IRS Form 656, Offer in Compromise, there are several essential practices to adopt and pitfalls to avoid to enhance your chances of reaching a favorable outcome. Here is a guide to help navigate this form:

- Do:

- Ensure you have filed all legally required tax returns before submitting Form 656. An offer will not be considered unless all necessary tax documentation is current and filed.

- Use the Offer in Compromise Pre-Qualifier tool available on the IRS website to assess eligibility before you begin the paperwork. This tool provides a preliminary understanding of your eligibility and potential offer amount.

- Confirm that you have received a bill for at least one tax debt included on your offer. The IRS needs this to proceed with your form.

- Include all required estimated tax payments for the current year and, if applicable, make all required federal tax deposits for the current quarter if you are a business owner with employees.

- Gather detailed financial information about your assets, income, expenses, and future earning potential as the application requires comprehensive disclosure.

- Don't:

- Submit Form 656 if you or your business is in an open bankruptcy proceeding. Such situations are handled within the bankruptcy process, not through an offer in compromise.

- Ignore open audit or outstanding innocent spouse claims. Be sure to resolve these issues before submitting your offer.

- File without considering your full ability to pay the debt through installment agreements or asset equity. The IRS seeks to compromise based on what you can legitimately afford to pay.

- Forget about your future tax refunds. Be aware that the IRS will apply any refunds you are due for tax periods through the calendar year in which they accept the offer to your tax debt. This will not be considered a payment toward your offer amount.

- Overlook the necessity of staying current with all tax filing and payment obligations during the consideration of your offer and for five years after acceptance. Failure to comply can result in the return or nullification of the accepted offer.

Adhering to these guidelines will streamline the process, potentially leading to a successful offer in compromise. It helps to address your tax liabilities thoughtfully and realistically, providing a pathway to financial recovery without exacerbating your situation.

Misconceptions

Understanding the IRS Form 656, an Offer in Compromise (OIC), can often lead to misconceptions. Here are four common misunderstandings and the truths behind them:

- Misconception #1: Submitting Form 656 guarantees the IRS will accept your offer.

Reality: Filing Form 656 starts a review process but does not guarantee acceptance. The IRS evaluates your ability to pay based on your financial situation, considering factors like income, expenses, and asset equity. Your offer must reflect your true ability to pay for it to be accepted.

- Misconception #2: You can’t make an offer if you haven’t filed all your tax returns.

Reality: Eligibility for an OIC requires you to have filed all legally required tax returns. The IRS will return your offer without consideration if all required returns are not filed, emphasizing the importance of being up-to-date with your tax filings before submitting Form 656.

- Misconception #3: An OIC stops all collection activities and penalties.

Reality: While submitting an OIC may temporarily suspend certain collection efforts, it does not stop penalties and interest from accruing. Additionally, the IRS can still levy your assets up until your offer is accepted. Keeping current with other tax obligations during the review process is crucial.

- Misconception #4: Future tax refunds will not be affected after an OIC is accepted.

Reality: The IRS will apply any tax refunds due to you for the calendar year in which your offer is accepted towards your tax debt. This includes any tax refund you would have received had your offer not been accepted, underscoring the need to understand the implications fully on future tax refunds.

Clearing up these misconceptions can help individuals better prepare for and understand the process of submitting an Offer in Compromise through Form 656, ultimately aiding in making informed decisions about tackling tax debt.

Key takeaways

The IRS Form 656, known as the Offer in Compromise (OIC) form, is a critical document for taxpayers seeking to resolve their tax debts for less than the full amount owed. Filling out and submitting this form initiates a detailed review process by the IRS. Here are five key takeaways about using the IRS Form 656:

- Eligibility requirements must be met before applying: Before considering an offer in compromise (OIC), taxpayers must ensure they have filed all required tax returns, received a bill for at least one tax debt included in the offer, made all required estimated tax payments for the current year, and if applicable, made all required federal tax deposits for the current quarter if they are a business owner with employees.

- Determining the offer amount is crucial: Taxpayers should use the OIC Pre-Qualifier tool available on the IRS website to help determine a preliminary offer amount. This tool assists in gathering necessary information and provides instant feedback based on the provided details. However, the initial offer amount suggested by the tool is not a guarantee of acceptance by the IRS.

- Submission of the form does not halt accrual of penalties and interest: While the IRS reviews the OIC, penalties and interest will continue to accrue on the outstanding tax debt. It's important for taxpayers to understand that submitting a Form 656 does not freeze the accrual of additional costs on their debt.

- Future tax refunds may be applied to your tax debt: If the IRS accepts a taxpayer's offer, any tax refund due to the taxpayer for the tax periods through the calendar year of acceptance will be applied to their tax debt. This means that taxpayers should not expect to receive tax refunds while their offer is being considered and possibly after acceptance.

- Payment options are available but come with requirements: Taxpayers can choose between a lump-sum cash payment or a periodic payment option when submitting their OIC. The lump-sum option requires 20% of the total offer amount upfront, with the balance paid within five months. The periodic payment option requires the first payment with the offer and the remaining balance paid within 6 to 24 months. For either payment option, failure to make the agreed payments can result in the return of the offer without appeal.

Filling out and submitting the IRS Form 656 is a process that requires thoroughness and accuracy. Taxpayers must provide comprehensive details about their financial situation, adhere to the eligibility criteria, and remain committed to the payment plan proposed in their offer. Understanding these key aspects can aid in preparing a credible and feasible Offer in Compromise application.

Popular PDF Documents

What Is an 8850 Form - The Work Opportunity Tax Credit program encourages the employment of individuals who face employment challenges.

IRS 1310 - This form allows individuals to claim a tax refund on behalf of someone who has passed away.