Get IRS 1099-S Form

When people think about selling a property, they often focus on the numbers: sale price, closing costs, and profit. However, an important piece that shouldn't be overlooked in this financial puzzle is the IRS 1099-S form. This form is crucial for reporting the sale of real estate to the Internal Revenue Service. Whether you're selling your primary home, a piece of land, or a rental property, if the transaction qualifies, you'll need to report it using the 1099-S form. It's not just for individual sellers; entities like corporations, trusts, and estates must also use this form if they're involved in real estate transactions. The form helps ensure that all necessary taxes on real estate transactions are paid. It covers a broad spectrum, requiring information on the sale's gross proceeds among other details. Understanding the significance of the 1099-S form is key to navigating the complexities of real estate transactions and complying with tax obligations.

IRS 1099-S Example

Attention:

Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file copy A downloaded from this website; a penalty may be imposed for filing with the IRS information return forms that can’t be scanned. See part O in the current General Instructions for Certain Information Returns, available at www.irs.gov/form1099, for more information about penalties.

Please note that Copy B and other copies of this form, which appear in black, may be downloaded and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns, which include a scannable Copy A for filing with the IRS and all other applicable copies of the form, visit www.IRS.gov/orderforms. Click on Employer and Information Returns, and we’ll mail you the forms you request and their instructions, as well as any publications you may order.

Information returns may also be filed electronically using the IRS Filing Information Returns Electronically (FIRE) system (visit www.IRS.gov/FIRE) or the IRS Affordable Care Act Information Returns (AIR) program (visit www.IRS.gov/AIR).

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

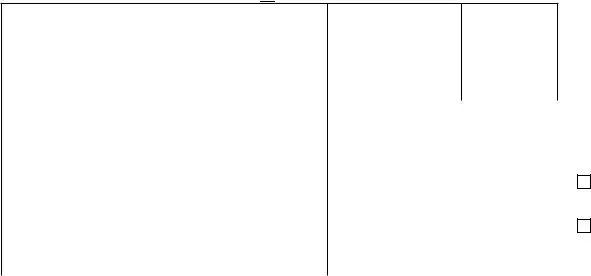

7575 |

VOID |

CORRECTED |

|

|

|

|

|||

FILER’S name, street address, city or town, state or province, country, |

1 |

Date of closing |

|

OMB No. |

|

|

|

||

ZIP or foreign postal code, and telephone number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2021 |

|

Proceeds From Real |

|

|

|

|

2 |

Gross proceeds |

|

|

Estate Transactions |

||

|

|

|

$ |

|

|

Form |

|

|

|

FILER’S TIN |

TRANSFEROR’S TIN |

|

3 |

Address (including city, state, and ZIP code) or legal description |

Copy A |

||||

|

|

|

|

|

|

|

|

|

For |

|

|

|

|

|

|

|

|

|

Internal Revenue |

TRANSFEROR’S name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Service Center |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

File with Form 1096. |

|

|

|

4 |

Check here if the transferor received or will receive |

|

||||

|

|

|

|

For Privacy Act |

|||||

|

|

|

|

property or services as part of the consideration |

▶ |

|

|||

Street address (including apt. no.) |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

and Paperwork |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Check here if the transferor is a foreign person |

|

Reduction Act |

|||

City or town, state or province, country, and ZIP or foreign postal code |

|

(nonresident alien, foreign partnership, foreign estate, |

|

Notice, see the |

|||||

|

|

|

|

or foreign trust) . . . . |

. . . . . |

▶ |

|

2021 General |

|

|

|

|

|

|

|

|

|

|

Instructions for |

Account number (see instructions) |

|

|

6 |

Buyer’s part of real estate tax |

|

|

|

Certain Information |

|

|

|

|

$ |

|

|

|

|

|

Returns. |

Form |

Cat. No. 64292E |

|

www.irs.gov/Form1099S |

Department of the Treasury - Internal Revenue Service |

|||||

Do Not Cut or Separate Forms on This Page — Do Not Cut or Separate Forms on This Page

CORRECTED (if checked)

CORRECTED (if checked)

FILER’S name, street address, city or town, state or province, country, |

1 Date of closing |

OMB No. |

ZIP or foreign postal code, and telephone number |

|

|

|

|

|

|

|

|

2021 |

Proceeds From Real |

|

|

|

|

2 Gross proceeds |

Estate Transactions |

||||

|

|

$ |

|

|

Form |

|

|

|

FILER’S TIN |

TRANSFEROR’S TIN |

|

3 Address (including city, state, and ZIP code) or legal description |

Copy B |

||||

|

|

|

|

|

|

|

|

For Transferor |

TRANSFEROR’S name |

|

|

|

|

|

|

|

This is important tax |

|

|

|

|

|

|

|

|

information and is being |

|

|

|

|

|

|

|

|

furnished to the IRS. If |

|

|

4 |

Transferor received or will receive property or services |

|||||

|

|

you are required to file a |

||||||

Street address (including apt. no.) |

|

|

|

as part of the consideration (if checked) . . . |

|

|||

|

|

|

▶ |

return, a negligence |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

penalty or other |

|

|

5 |

If checked, transferor is a foreign person (nonresident |

|||||

|

|

sanction may be |

||||||

City or town, state or province, country, and ZIP or foreign postal code |

|

|

alien, foreign partnership, foreign estate, or foreign |

|||||

|

|

imposed on you if this |

||||||

|

|

trust) |

. . . . . |

▶ |

||||

|

|

|

|

item is required to be |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

reported and the IRS |

Account number (see instructions) |

|

6 |

Buyer’s part of real estate tax |

|

|

|||

|

|

|

determines that it has |

|||||

|

|

$ |

|

|

|

|

not been reported. |

|

Form |

(keep for your records) |

www.irs.gov/Form1099S |

Department of the Treasury - Internal Revenue Service |

|||||

Instructions for Transferor

For sales or exchanges of certain real estate, the person responsible for closing a real estate transaction must report the real estate proceeds to the IRS and must furnish this statement to you. To determine if you have to report the sale or exchange of your main home on your tax return, see the Instructions for Schedule D (Form 1040). If the real estate was not your main home, report the transaction on Form 4797, Form 6252, and/or the Schedule D for the appropriate income tax form. If box 4 is checked and you received or will receive

Federal mortgage subsidy. You may have to recapture (pay back) all or part of a federal mortgage subsidy if all the following apply.

•You received a loan provided from the proceeds of a qualified mortgage bond or you received a mortgage credit certificate.

•Your original mortgage loan was provided after 1990.

•You sold or disposed of your home at a gain during the first 9 years after you received the federal mortgage subsidy.

•Your income for the year you sold or disposed of your home was over a specified amount.

This will increase your tax. See Form 8828 and Pub. 523.

Transferor’s taxpayer identification number (TIN). For your protection, this form may show only the last four digits of your TIN (social security number (SSN), individual taxpayer identification number (ITIN), adoption taxpayer identification number (ATIN), or employer identification number (EIN)). However, the issuer has reported your complete TIN to the IRS.

Account number. May show an account or other unique number the filer assigned to distinguish your account.

Box 1. Shows the date of closing.

Box 2. Shows the gross proceeds from a real estate transaction, generally the sales price. Gross proceeds include cash and notes payable to you, notes assumed by the transferee (buyer), and any notes paid off at settlement. Box 2 does not include the value of other property or services you received or will receive. See Box 4.

Box 3. Shows the address or legal description of the property transferred.

Box 4. If checked, shows that you received or will receive services or property (other than cash or notes) as part of the consideration for the property transferred. The value of any services or property (other than cash or notes) is not included in box 2.

Box 5. If checked, shows that you are a foreign person (nonresident alien, foreign partnership, foreign estate, or foreign trust).

Box 6. Shows certain real estate tax on a residence charged to the buyer at settlement. If you have already paid the real estate tax for the period that includes the sale date, subtract the amount in box 6 from the amount already paid to determine your deductible real estate tax. But if you have already deducted the real estate tax in a prior year, generally report this amount as income on the “Other income” line of Schedule 1 (Form 1040). For more information, see Pub. 523, Pub. 525, and Pub. 530.

Future developments. For the latest developments related to Form

FreeFile. Go to www.irs.gov/FreeFile to see if you qualify for

|

VOID |

CORRECTED |

|

|

|

|

|||

FILER’S name, street address, city or town, state or province, country, |

1 Date of closing |

|

OMB No. |

|

|

|

|||

ZIP or foreign postal code, and telephone number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2021 |

|

Proceeds From Real |

|

|

|

|

2 |

Gross proceeds |

|

|

Estate Transactions |

||

|

|

|

$ |

|

|

Form |

|

|

|

FILER’S TIN |

TRANSFEROR’S TIN |

|

3 |

Address (including city, state, and ZIP code) or legal description |

Copy C |

||||

|

|

|

|

|

|

|

|

|

For Filer |

TRANSFEROR’S name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Street address (including apt. no.) |

|

|

4 |

Check here if the transferor received or will receive |

|

For Privacy Act |

|||

|

|

|

property or services as part of the consideration |

▶ |

|

and Paperwork |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reduction Act |

|

|

|

5 |

Check here if the transferor is a foreign person |

|

||||

|

|

|

|

Notice, see the |

|||||

City or town, state or province, country, and ZIP or foreign postal code |

|

(nonresident alien, foreign partnership, foreign estate, |

|

||||||

|

or foreign trust) . . . . |

. . . . . ▶ |

|

2021 General |

|||||

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

Instructions for |

Account number (see instructions) |

|

|

6 |

Buyer’s part of real estate tax |

|

|

|

Certain Information |

|

|

|

|

$ |

|

|

|

|

|

Returns. |

|

|

|

|

|

|

|

|

|

|

Form |

|

www.irs.gov/Form1099S |

Department of the Treasury - Internal Revenue Service |

||||||

Instructions for Filer

To complete Form

•The 2021 General Instructions for Certain Information Returns, and

•The 2021 Instructions for Form

To order these instructions and additional forms, go to www.irs.gov/Form1099S.

Caution: Because paper forms are scanned during processing, you cannot file Forms 1096, 1097, 1098, 1099, 3921, or 5498 that you print from the IRS website.

Due dates. Furnish Copy B of this form to the transferor by February 15, 2022.

File Copy A of this form with the IRS by

February 28, 2022. If you file electronically, the due date is March 31, 2022. To file electronically, you must have software that generates a file according to the

specifications in Pub. 1220. The IRS does not provide a

Foreign transferors. Sales or exchanges involving foreign transferors are reportable on Form

Need help? If you have questions about reporting on Form

Document Specifics

| Fact Name | Description |

|---|---|

| Purpose of Form 1099-S | Used to report proceeds from real estate transactions to the IRS. |

| Who Files Form 1099-S | Typically filed by the person responsible for closing the transaction, such as a real estate broker. |

| Transaction Types Covered | Includes sales or exchanges of real property, including homes, buildings, and land. |

| Threshold for Reporting | Transactions must be reported if the proceeds are $600 or more. |

| Exemptions | Primary residence sales may be exempt if certain requirements are met. |

| Filing Deadline | Must be filed with the IRS by March 31st of the year following the transaction if filing electronically, or February 28th if filing by paper. |

| Recipient Copy Deadline | The person involved in the transaction must receive their copy of Form 1099-S by January 31st following the year of the transaction. |

| Governing Laws | Federal law requires the filing of Form 1099-S, while state-specific requirements may vary. |

Guide to Writing IRS 1099-S

Filling out the IRS 1099-S Form is a necessary step for reporting certain types of real estate transactions. This procedure ensures that all parties involved comply with tax reporting requirements. The process may seem daunting at first, but with a clear understanding of the steps involved, individuals can accurately complete the form. Here, we will guide you through each crucial step, ensuring that you are well-prepared to handle this task. The sequence listed below simplifies the process, making it less overwhelming and helps to avoid common mistakes. Remember, after submitting the form, keep a copy for your records, as it may be needed for future reference or inquiries.

- Begin by obtaining the correct version of the IRS 1099-S Form for the tax year in question. This can be done through the IRS website.

- Enter the Filer's name, street address, city, state, ZIP code, and telephone number in the appropriate sections at the top of the form.

- Provide the Filer’s identification number and the Transferor's identification number in the designated areas.

- Fill in the Transferor's name. If the property is owned jointly, include the names of all parties on separate lines.

- Complete the address section with the Transferor’s street address, city, state, and ZIP code.

- Report the date of closing for the real estate transaction in the space provided.

- Enter the gross proceeds from the transaction. This refers to the total amount the property was sold for, not including expenses such as closing costs.

- If applicable, fill in the section concerning the transferor’s part of the real estate tax. This is only necessary if part of the real estate tax was paid by the seller as part of the closing agreement.

- Before signing, review the form to ensure all the information is correct and complete. Mistakes can lead to processing delays or inquiries from the IRS.

- Finally, sign and date the form in the designated area. If you are filing electronically, the process for signing may differ based on the software or service used.

After the form is filled out and submitted, the next steps involve waiting for any communications from the IRS should there be issues or questions regarding the submitted form. It is important to respond promptly to any requests from the IRS to avoid penalties. Additionally, the individual should monitor their tax records to ensure that the transaction is recorded accurately for future tax returns. This careful attention to detail will serve as a cornerstone for managing tax obligations efficiently and accurately.

Understanding IRS 1099-S

-

What is a 1099-S form and who needs to file it?

The 1099-S form is a tax document used to report proceeds from real estate transactions. It's typically filed by the person responsible for closing the sale, such as a title or settlement company, a mortgage lender, or a real estate broker. This form must be filed for transactions involving a wide array of real estate properties, including land, buildings, homes, and any related structures, if the proceeds from the sale exceed a certain threshold. Individuals who have sold their main home may not need to file this form if they meet specific IRS requirements for exclusion.

-

What information do I need to fill out the 1099-S form?

To properly fill out the 1099-S form, you'll need several pieces of information:

- The seller's name, address, and taxpayer identification number (TIN or SSN).

- The date of the closing of the transaction.

- The gross proceeds from the transaction.

- Any real estate property involved in the transaction.

- Information about whether the seller received or will receive property or services as part of the transaction.

This information helps the IRS track real estate transactions and ensure that sellers are reporting their sales correctly on their tax returns.

-

How do I know if I’m exempt from filing the 1099-S form for the sale of my main home?

You may be exempt from filing the 1099-S form for the sale of your main home if you meet certain conditions:

- You used the home as your main residence for at least two of the last five years.

- The gain from the sale is $250,000 or less if single or $500,000 or less if married filing jointly.

- You have not excluded the gain on another home sale in the two years before the current sale.

Even if you meet these conditions, other factors may still require you to file a 1099-S. Consulting with a tax professional can help clarify your specific situation.

-

Where do I file the 1099-S form and what are the deadlines?

The 1099-S form should be filed with the IRS, and a copy must also be sent to the person(s) involved in the transaction. The deadline for sending the form to the recipient is January 31 of the year following the transaction. The deadline for filing with the IRS varies:

- If filing by paper, the deadline is February 28.

- If filing electronically, the deadline is March 31.

It’s important to meet these deadlines to avoid penalties. However, if the date falls on a weekend or a legal holiday, the deadline is the next business day.

Common mistakes

-

Not Reporting the Transaction: Many individuals mistakenly believe they don't need to report the sale if it was a personal residence or if the profit was below a certain threshold. However, all real estate transactions need to be reported, regardless of profit or property type.

-

Incorrectly Reporting the Seller's Information: Sometimes, the name and Social Security Number (SSN) or Employer Identification Number (EIN) of the seller are incorrectly listed. Accuracy here is paramount to ensure there are no mismatches with IRS records.

-

Misunderstanding the Date of Sale: The actual closing date should be reported as the date of sale, not when the contract was signed or when possession was transferred if different from the closing date.

-

Omitting or Misreporting Gross Proceeds: Individuals often make the mistake of not reporting, underreporting, or overreporting the gross proceeds from the sale. It's essential to list the total amount received, as documented in the closing statement.

-

Failure to Distinguish Personal Property from Real Property: In transactions where both types of property are sold together (like a furnished home), sellers sometimes fail to separate the values of the real property (the land and building) from the personal property (the furnishings).

-

Incorrect Allocation Among Multiple Sellers: When a property has multiple sellers, the amount of gross proceeds must be allocated accurately among them according to their ownership interests.

-

Using Incorrect Form Versions: The IRS occasionally updates tax forms. Using an outdated version of the 1099-S form can lead to processing delays or the form being rejected altogether.

-

Neglecting State Reporting Requirements: Beyond the federal IRS requirements, some states have their own reporting requirements for real estate sales. Sellers should verify whether they need to submit similar information at the state level.

In summary, filling out the IRS 1099-S form requires careful attention to detail and an understanding of your obligations. By avoiding these common mistakes, you can help ensure your real estate transactions are reported clearly and accurately, thereby avoiding potential pitfalls with the IRS.

Documents used along the form

When dealing with the IRS 1099-S form, which reports proceeds from real estate transactions, it's essential to gather and prepare other related documents to ensure a thorough and compliant submission. These materials not only complement the information on the 1099-S but also provide a comprehensive view of the transaction's financial and legal parameters. Below is a list of other forms and documents that are often used in conjunction with the IRS 1099-S form, each serving a unique purpose in the broader context of real estate transactions and tax reporting.

- IRS Form 1040: The U.S. Individual Income Tax Return is where individuals report their annual income, including any capital gains from real estate sales, which ties into the information provided by the 1099-S form.

- Schedule D (Form 1040): This form is used to summarize capital gains and losses from transactions, including those reported on the 1099-S, and is essential for accurately calculating tax liability.

- IRS Form 1099-MISC: If there were miscellaneous income payments made related to the real estate transaction, such as contractor payments during a property sale, this form would be necessary.

- IRS Form 4797: Used for the sale of business property, it's relevant when the real estate transaction involves property used in a trade or business and can work alongside the 1099-S for reporting purposes.

- Closing Disclosure: This document summarizes the details of the transaction, including the sale price and any real estate commissions. It's crucial for verifying the information reported on the 1099-S.

- HUD-1 Settlement Statement: Although now mostly replaced by the Closing Disclosure for consumer home purchases, this form is still used for certain types of real estate transactions and provides a detailed financial breakdown.

- Escrow Statement: This statement outlines the funds held in escrow during the real estate transaction, including taxes, commissions, and other fees, offering insight into the financial flow of the sale.

- Property Deed: While not a tax form, the deed proves ownership transfer and is essential for legal verification of the sale, which underpins the financial information reported on the 1099-S.

Gathering these documents when working with a 1099-S form provides a holistic view of the transaction and ensures that all relevant financial activities are accurately reported to the IRS. This collection of forms and documents ultimately supports the primary objective of compliance and streamlined processing of real estate transaction information for taxation purposes. Specifically, they facilitate transparent reporting, proper tax calculation, and a clear record of the property's transfer of ownership.

Similar forms

The IRS 1099-S form is closely related to the IRS 1099-MISC form, as both are part of the 1099 series used to report non-employment income to the Internal Revenue Service (IRS). The 1099-MISC is specifically utilized for reporting payments made in the course of a trade or business to individuals not employed by the paying entity, covering categories like rent, prizes, awards, and other income payments. This similarity lies in their shared purpose of informing the IRS about income that might not be subject to regular wage withholding, helping to ensure that all income is reported accurately for tax purposes.

Similarly, the IRS 1099-INT form is akin to the 1099-S, since it’s used to report interest income to the taxpayer and the IRS. Financial institutions and other entities pay interest on investments or accounts, and when they do, the 1099-INT form outlines the amount of interest paid over the year. Both of these forms are crucial for taxpayers, as the information they provide is necessary to accurately report income and determine tax liability, reflecting their role in promoting transparent and thorough income reporting.

The IRS 1099-DIV form also shares a resemblance with the 1099-S. This form reports dividends and other distributions to investors, particularly focusing on income received from stocks and mutual funds. Like the 1099-S, which reports proceeds from real estate transactions, the 1099-DIV helps taxpayers and the IRS track another type of investment income, ensuring that all earnings are accounted for when filing taxes. Each of these forms plays a distinctive role in the broader landscape of income and tax reporting by highlighting different sources of income.

Another document in this series, the IRS 1099-R, shares a purpose with the 1099-S but focuses on distributions from pensions, annuities, retirement plans, IRAs, or insurance contracts. It reports any money that was paid out to the taxpayer from these sources over the year. Both the 1099-S and 1099-R assist in the comprehensive reportage of financial transactions that could affect an individual's tax obligations, despite focusing on distinct types of transactions. This ensures that taxpayers can account for various types of income that might otherwise be overlooked.

The IRS 1040 form, while not a part of the 1099 series, is intrinsically linked to the 1099-S and its counterparts. It is the primary form individuals use to file their annual income tax returns. The information reported on the 1099 forms, including the 1099-S, needs to be reflected on the taxpayer’s 1040 form. Specific lines on the 1040 form are designated for reporting different types of income documented by various 1099 forms, demonstrating the interconnectivity between these documents in the tax reporting process.

Lastly, the Schedule D (Form 1040) is related to the 1099-S through its focus on capital gains and losses. Individuals use Schedule D to summarize the capital gains and losses from transactions reported on forms like the 1099-S, which includes sales or exchanges of capital assets, including real estate. This relationship underscores the importance of both documents in calculating the taxpayer’s capital gains tax liabilities, highlighting how the comprehensive reporting of transactions can influence tax outcomes.

Dos and Don'ts

When it comes to handling IRS forms, precision and adherence to guidelines are paramount. The 1099-S form, widely used to report proceeds from real estate transactions, is no exception. Here's a breakdown of the dos and don'ts to ensure accuracy and compliance.

Do:

- Verify the taxpayer identification number (TIN) of the person you're reporting on. This vital piece of information must be accurate to ensure the IRS can correctly match the form to the individual.

- Report the exact amount of money or value of property received. It's crucial to meticulously calculate this figure to prevent discrepancies.

- Include all necessary details about the property, such as its location and a description. This helps the IRS understand the nature of the transaction.

- Utilize the IRS's electronic filing system if you're required to file 250 or more forms. This not only streamlines the process but is also mandated for large volume filings.

- Keep a copy of each 1099-S form for your records. Maintaining thorough records can assist in the event of any queries or audits from the IRS.

- Send the form to the recipient by the required deadline, typically January 31 following the year of the transaction. Timeliness is key in staying compliant.

Don't:

- Leave any fields blank. If a section does not apply, entering 'N/A' or '0' where appropriate is better than leaving a space empty.

- Forget to check the form for updates each tax year. The IRS might revise forms annually, and using an outdated version can lead to errors.

- Use the form to report transactions that are not related to real estate. The 1099-S is specific to real estate transactions and shouldn't be used for other purposes.

- Mistake the 1099-S for other 1099 forms. Each type of 1099 form serves a different purpose; ensure you're using the correct one for real estate transactions.

- Ignore IRS notices about mistakes on your form. If you receive communication regarding errors, address it promptly to avoid penalties.

- Omit sending a copy of the form to the state tax department if required by your state. Some states have additional filing requirements, so it's important to stay informed.

Misconceptions

The IRS 1099-S form is closely tied to real estate transactions, documenting proceeds from sales or exchanges. However, several misconceptions surround this form, impacting individuals’ understanding and compliance. Here, we clarify some common misunderstandings:

All real estate sales must be reported on the 1099-S form. Not all real estate transactions require filing a 1099-S. Specific criteria, such as the seller’s use of the property as a primary residence for at least two of the last five years, may exempt the sale from being reported.

If you don’t receive a 1099-S form, you don’t need to report the sale on your tax return. Even if a 1099-S is not issued, taxpayers must report all real estate transactions on their tax returns. The responsibility to accurately report lies with the taxpayer, regardless of receiving the form.

The 1099-S form is only for reporting the sale of buildings. This form also applies to land sales, including vacant land. Any real estate transaction, not just buildings, can be subject to reporting on the 1099-S.

Only the buyer’s information is required on the form. Both the buyer(s) and seller(s) information, including their tax identification numbers and the closing date of the transaction, need to be reported on the form.

Personal property sales are reported on a 1099-S form. The 1099-S form is designated for real estate transactions. Sales of personal property are typically reported on Form 1099-MISC or 1099-NEC, depending on the nature of the transaction.

Filing a 1099-S form always leads to a tax liability. Reporting a transaction via the 1099-S does not automatically result in a tax liability. Exclusions may apply, particularly if the property was used as the seller’s primary residence under certain conditions.

Reporting on Form 1099-S is only the responsibility of the real estate agent involved in the transaction. While real estate agents often assist in the process, the responsibility to file the 1099-S can also fall on attorneys, title companies, or even the property seller, depending on the transaction specifics.

The deadline to file a 1099-S form is the end of the tax year. Unlike personal tax returns, the 1099-S must be filed with the IRS by March 31 of the year following the calendar year in which the transaction occurred if filing electronically, or February 28 if filing by paper.

Key takeaways

Filing and utilizing the IRS 1099-S form, associated with real estate transactions, requires attention to specific details to ensure completeness and accuracy. Here are some key takeaways to guide you through the process:

The IRS 1099-S form is crucial for reporting proceeds from real estate transactions. Sellers of real estate properties, including land, permanently installed structures, buildings, and condominiums, need to disclose the sale on this form.

It's essential to determine if you're required to file the form. Not all real estate transactions necessitate a 1099-S. For example, personal residences may be exempt under certain conditions, such as if the sale price is below a specified threshold.

Accuracy is key when filling out the form. You must provide detailed information about the sale, including the date, sale price, and property description. Ensuring that all details are correct can prevent potential issues with the IRS in the future.

Timeliness matters. The 1099-S form must be submitted to the IRS by a specific deadline, usually by February 28th (or March 31st if filing electronically) of the year following the transaction. Late submissions can result in penalties.

Understand the implications for buyers and sellers. While the responsibility to file the 1099-S typically falls on the person responsible for closing the sale, such as the real estate professional or legal representative, both parties should ensure that the transaction is properly reported to avoid future disputes or audits.

By keeping these points in mind, individuals involved in real estate transactions can better navigate the complexities of the 1099-S form. Consultation with a tax professional is often beneficial to address specific concerns or unusual situations.

Popular PDF Documents

Proof of Payment Letter - A functional form that emphasizes Loyola Plans' commitment to customer service and account accuracy.

Does the Irs Accept Electronic Signatures on Form 1040 - By completing Form 2848, you can allow someone else, typically a tax attorney or accountant, to fully engage with the IRS for you.