Get IRS 1065 Form

When navigating the complexities of tax season, business partnerships find themselves facing the crucial task of filing a specific document known as the IRS 1065 form. This form is not just another piece of paperwork; it plays a pivotal role in reporting the income, gains, losses, deductions, and credits of a business to the Internal Revenue Service. Understanding this form is essential for partners who wish to comply with tax obligations accurately, avoiding common pitfalls and ensuring the financial health of their partnership. It acts as a transparent medium that details how the business's profits or losses are shared among its partners, which subsequently affects each partner's individual tax liabilities. Despite its importance, many find the form daunting due to its detailed requirements and the implications it carries for future financial decisions. A thorough grasp of the IRS 1065 form is, therefore, indispensable for those seeking to navigate their financial responsibilities with confidence and precision.

IRS 1065 Example

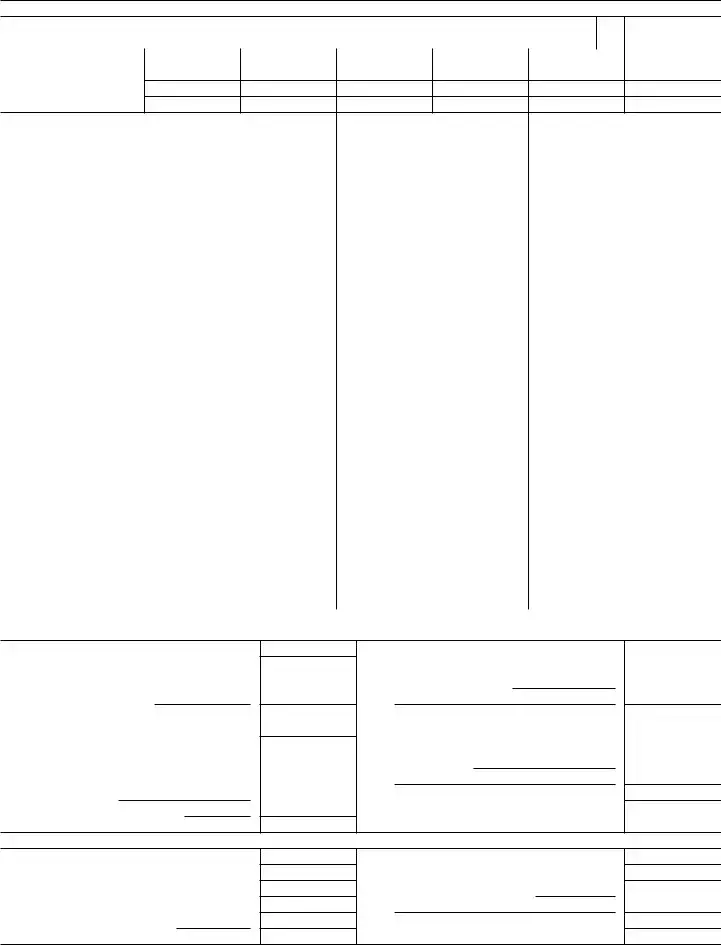

Form 1065 |

|

|

U.S. Return of Partnership Income |

|

|

|

OMB No. |

|||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Department of the Treasury |

For calendar year 2021, or tax year beginning |

|

, 2021, ending |

, 20 |

. |

|

2021 |

|||||

|

|

▶ Go to www.irs.gov/Form1065 for instructions and the latest information. |

|

|

||||||||

Internal Revenue Service |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|||

A Principal business activity |

|

Name of partnership |

|

|

|

|

|

|

D Employer identification number |

|||

|

|

|

|

|

|

|||||||

B Principal product or service |

Type |

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

|

E Date business started |

|||||||

|

|

or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

C Business code number |

City or town, state or province, country, and ZIP or foreign postal code |

|

|

F Total assets |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

G |

Check applicable boxes: |

(1) |

Initial return |

(2) |

Final return |

(3) |

Name change (4) |

Address change |

(5) |

Amended return |

||

H |

Check accounting method: |

(1) |

Cash |

(2) |

Accrual |

(3) |

Other (specify) ▶ |

|

|

|

|

|

INumber of Schedules

J |

Check if Schedules C and |

. . . . . . . . . . . . . . . . ▶ |

|

K |

Check if partnership: (1) |

Aggregated activities for section 465 |

Grouped activities for section 469 passive activity purposes |

Caution: Include only trade or business income and expenses on lines 1a through 22 below. See instructions for more information.

|

|

1a |

Gross receipts or sales |

. |

1a |

|

|

|

|

|

|

|

|

|

||||

|

|

b |

Returns and allowances |

. |

1b |

|

|

|

|

|

|

|

|

|

||||

|

|

c |

Balance. Subtract line 1b from line 1a |

. . . . . . . . . |

|

1c |

|

|

|

|

||||||||

Income |

|

2 |

Cost of goods sold (attach Form |

. . . . . . . . . |

|

2 |

|

|

|

|

||||||||

|

3 |

Gross profit. Subtract line 2 from line 1c |

. . . . . . . . . |

|

3 |

|

|

|

|

|||||||||

|

4 |

Ordinary income (loss) from other partnerships, estates, and trusts (attach statement) . . . . |

|

4 |

|

|

|

|

||||||||||

|

5 |

Net farm profit (loss) (attach Schedule F (Form 1040)) |

. . . . . . . . . |

|

5 |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

6 |

Net gain (loss) from Form 4797, Part II, line 17 (attach Form 4797) . |

. . . . . . . . . |

|

6 |

|

|

|

|

||||||||

|

|

7 |

Other income (loss) (attach statement) |

. . . . . . . . . |

|

7 |

|

|

|

|

||||||||

|

|

8 |

Total income (loss). Combine lines 3 through 7 |

. . . . . . . . . |

|

8 |

|

|

|

|

||||||||

limitations) |

|

9 |

Salaries and wages (other than to partners) (less employment credits) |

. . . . . . . . . |

|

9 |

|

|

|

|

||||||||

|

10 |

Guaranteed payments to partners |

. . . . . . . . . |

|

10 |

|

|

|

|

|||||||||

|

11 |

Repairs and maintenance |

. . . . . . . . . |

|

11 |

|

|

|

|

|||||||||

|

12 |

Bad debts |

. . . . . . . . . |

|

12 |

|

|

|

|

|||||||||

for |

|

|

|

|

|

|

||||||||||||

|

13 |

Rent |

. . . . . . . . . |

|

13 |

|

|

|

|

|||||||||

instructions |

|

|

|

|

|

|

||||||||||||

|

14 |

Taxes and licenses |

. . . . . . . . . |

|

14 |

|

|

|

|

|||||||||

|

15 |

Interest (see instructions) |

. . . . . . . . . |

|

15 |

|

|

|

|

|||||||||

|

16a |

Depreciation (if required, attach Form 4562) |

. |

16a |

|

|

|

|

|

|

|

|

|

|||||

(see |

|

|

|

|

|

|

|

|

|

|

||||||||

|

b |

Less depreciation reported on Form |

. |

16b |

|

|

|

|

16c |

|

|

|

|

|||||

Deductions |

|

|

|

|

|

|

|

|

|

|||||||||

|

17 |

Depletion (Do not deduct oil and gas depletion.) |

. . . . . . . . . |

|

17 |

|

|

|

|

|||||||||

|

18 |

Retirement plans, etc |

. . . . . . . . . |

|

18 |

|

|

|

|

|||||||||

|

19 |

Employee benefit programs |

. . . . . . . . . |

|

19 |

|

|

|

|

|||||||||

|

20 |

Other deductions (attach statement) |

. . . . . . . . . |

|

20 |

|

|

|

|

|||||||||

|

|

21 |

Total deductions. Add the amounts shown in the far right column for lines 9 through 20 . . . |

|

21 |

|

|

|

|

|||||||||

|

|

22 |

Ordinary business income (loss). Subtract line 21 from line 8 . . |

. . . . . . . . . |

|

22 |

|

|

|

|

||||||||

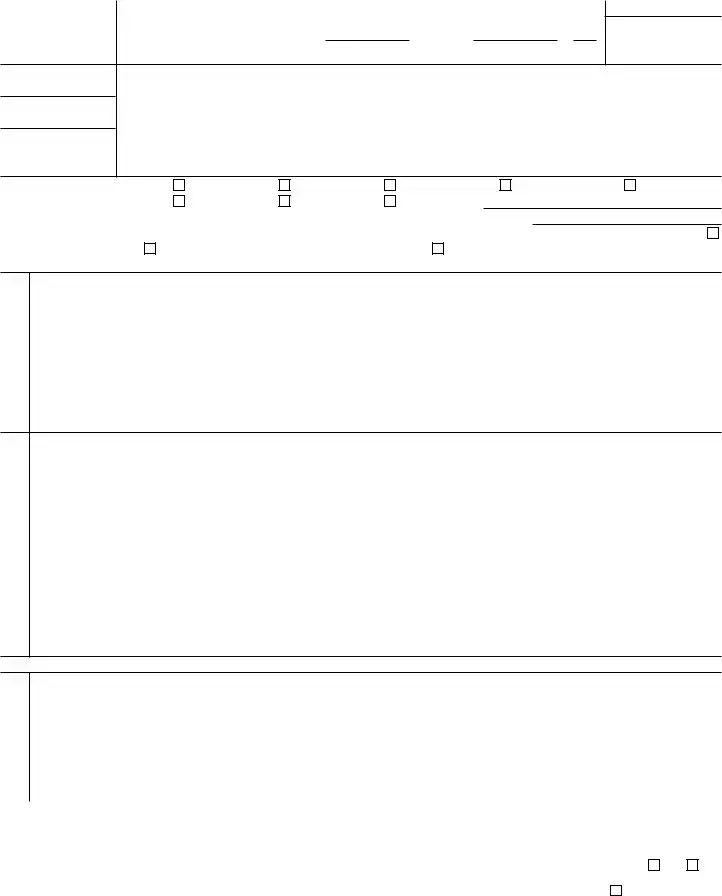

Payment |

|

23 |

Interest due under the |

|

23 |

|

|

|

|

|||||||||

|

24 |

Interest due under the |

|

24 |

|

|

|

|

||||||||||

|

25 |

BBA AAR imputed underpayment (see instructions) |

. . . . . . . . . |

|

25 |

|

|

|

|

|||||||||

|

26 |

Other taxes (see instructions) |

. . . . . . . . . |

|

26 |

|

|

|

|

|||||||||

and |

|

27 |

Total balance due. Add lines 23 through 26 |

. . . . . . . . . |

|

27 |

|

|

|

|

||||||||

|

28 |

Payment (see instructions) |

. . . . . . . . . |

|

28 |

|

|

|

|

|||||||||

Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

29 |

Amount owed. If line 28 is smaller than line 27, enter amount owed . |

. . . . . . . . . |

|

29 |

|

|

|

|

|||||||||

|

30 |

Overpayment. If line 28 is larger than line 27, enter overpayment . |

. . . . . . . . . |

|

30 |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge |

|||||||||||||||

Sign |

|

and belief, it is true, correct, and complete. Declaration of preparer (other than partner or limited liability company member) is based on all information of |

||||||||||||||||

|

which preparer has any knowledge. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

May the IRS discuss this return |

|||||||

Here |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

with the preparer shown below? |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions. Yes |

No |

||||

|

|

|

▲ Signature of partner or limited liability company member |

▲ |

Date |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Paid |

|

Print/Type preparer’s name |

Preparer’s signature |

|

|

|

Date |

|

Check |

if |

|

PTIN |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Firm’s name ▶ |

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

|

|||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Firm’s address ▶ |

|

|

|

|

|

|

Phone no. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

Cat. No. 11390Z |

|

|

|

|

|

Form 1065 (2021) |

||||||||||

Form 1065 (2021) |

|

|

|

|

|

|

|

Page 2 |

|||

Schedule B |

Other Information |

|

|

|

|

|

|

|

|

|

|

1 What type of entity is filing this return? Check the applicable box: |

|

|

Yes |

No |

|||||||

a |

Domestic general partnership |

b |

Domestic limited partnership |

|

|

|

|

|

|||

c |

Domestic limited liability company |

d |

Domestic limited liability partnership |

|

|

|

|

||||

e |

Foreign partnership |

f |

Other ▶ |

|

|

|

|

|

|||

2 At the end of the tax year: |

|

|

|

|

|

|

|

|

|

||

a Did any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or tax- |

|

|

|

||||||||

|

exempt organization, or any foreign government own, directly or indirectly, an interest of 50% or more in the profit, |

|

|

|

|||||||

|

loss, or capital of the partnership? For rules of constructive ownership, see instructions. If “Yes,” attach Schedule |

|

|

|

|||||||

|

|

|

|

||||||||

b Did any individual or estate own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital of |

|

|

|||||||||

|

|

|

|||||||||

|

the partnership? For rules of constructive ownership, see instructions. If “Yes,” attach Schedule |

|

|

|

|||||||

|

on Partners Owning 50% or More of the Partnership |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||

3 At the end of the tax year, did the partnership: |

|

|

|

|

|

|

|

|

|

||

a Own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of |

|

|

|

||||||||

|

stock entitled to vote of any foreign or domestic corporation? For rules of constructive ownership, see instructions. |

|

|

|

|||||||

|

If “Yes,” complete (i) through (iv) below |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(i) Name of Corporation |

|

|

(ii) Employer Identification |

|

(iii) Country of |

(iv) Percentage |

|||

|

|

|

|

|

Number (if any) |

|

Incorporation |

Owned in Voting Stock |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v) below . .

(i)Name of Entity

(ii)Employer Identification

Number (if any)

(iii)Type of Entity

(iv)Country of Organization

(v)Maximum Percentage Owned in Profit, Loss, or Capital

4 Does the partnership satisfy all four of the following conditions? |

Yes No |

aThe partnership’s total receipts for the tax year were less than $250,000.

bThe partnership’s total assets at the end of the tax year were less than $1 million.

cSchedules

d The partnership is not filing and is not required to file Schedule

If “Yes,” the partnership is not required to complete Schedules L,

5 Is this partnership a publicly traded partnership, as defined in section 469(k)(2)? . . . . . . . . . . .

6During the tax year, did the partnership have any debt that was canceled, was forgiven, or had the terms modified

so as to reduce the principal amount of the debt? . . . . . . . . . . . . . . . . . . . . .

7Has this partnership filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide

information on any reportable transaction? . . . . . . . . . . . . . . . . . . . . . . . .

8At any time during calendar year 2021, did the partnership have an interest in or a signature or other authority over a financial account in a foreign country (such as a bank account, securities account, or other financial account)? See instructions for exceptions and filing requirements for FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR). If “Yes,” enter the name of the foreign country ▶

9At any time during the tax year, did the partnership receive a distribution from, or was it the grantor of, or transferor to, a foreign trust? If “Yes,” the partnership may have to file Form 3520, Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. See instructions . . . . . . . . .

10a Is the partnership making, or had it previously made (and not revoked), a section 754 election? . . . . . .

See instructions for details regarding a section 754 election.

bDid the partnership make for this tax year an optional basis adjustment under section 743(b) or 734(b)? If “Yes,”

attach a statement showing the computation and allocation of the basis adjustment. See instructions . . . .

Form 1065 (2021)

Form 1065 (2021) |

|

|

Page 3 |

Schedule B |

Other Information (continued) |

|

|

c Is the partnership required to adjust the basis of partnership assets under section 743(b) or 734(b) because of a |

|

Yes No |

|

substantial |

|

||

734(d))? If “Yes,” attach a statement showing the computation and allocation of the basis adjustment. See instructions |

|

||

11Check this box if, during the current or prior tax year, the partnership distributed any property received in a like- kind exchange or contributed such property to another entity (other than disregarded entities wholly owned by the

partnership throughout the tax year) . . . . . . . . . . . . . . . . . . . . . . . . ▶

12At any time during the tax year, did the partnership distribute to any partner a

undivided interest in partnership property? . . . . . . . . . . . . . . . . . . . . . . . .

13If the partnership is required to file Form 8858, Information Return of U.S. Persons With Respect To Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs), enter the number of Forms 8858 attached. See

instructions . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

14Does the partnership have any foreign partners? If “Yes,” enter the number of Forms 8805, Foreign Partner’s

Information Statement of Section 1446 Withholding Tax, filed for this partnership . . . ▶

15Enter the number of Forms 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, attached

|

to this return . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ |

16a |

Did you make any payments in 2021 that would require you to file Form(s) 1099? See instructions |

b |

If “Yes,” did you or will you file required Form(s) 1099? |

17Enter the number of Forms 5471, Information Return of U.S. Persons With Respect To Certain Foreign

Corporations, attached to this return |

. . |

. |

. |

▶ |

||

|

|

|

|

|

|

|

18 Enter the number of partners that are foreign governments under section 892 |

. . |

. |

. |

▶ |

|

|

19During the partnership’s tax year, did the partnership make any payments that would require it to file Forms 1042 and

20Was the partnership a specified domestic entity required to file Form 8938 for the tax year? See the Instructions for Form 8938

21Is the partnership a section 721(c) partnership, as defined in Regulations section

22During the tax year, did the partnership pay or accrue any interest or royalty for which one or more partners are

not allowed a deduction under section 267A? See instructions . . . . . . . . . . . . . . . . .

If “Yes,” enter the total amount of the disallowed deductions . . . . . . . . . ▶ $

23Did the partnership have an election under section 163(j) for any real property trade or business or any farming

business in effect during the tax year? See instructions . . . . . . . . . . . . . . . . . . . .

24 Does the partnership satisfy one or more of the following? See instructions . . . . . . . . . . . . .

aThe partnership owns a

bThe partnership’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the partnership has business interest.

cThe partnership is a tax shelter (see instructions) and the partnership has business interest expense. If “Yes” to any, complete and attach Form 8990.

25 Is the partnership attaching Form 8996 to certify as a Qualified Opportunity Fund? . . . . . . . . . .

If “Yes,” enter the amount from Form 8996, line 15 . . . . . . . . . . . . ▶ $

26Enter the number of foreign partners subject to section 864(c)(8) as a result of transferring all or a portion of an interest in the partnership or of receiving a distribution from the partnership . . . . . ▶

Complete Schedule

27At any time during the tax year, were there any transfers between the partnership and its partners subject to the

disclosure requirements of Regulations section

28Since December 22, 2017, did a foreign corporation directly or indirectly acquire substantially all of the properties constituting a trade or business of your partnership, and was the ownership percentage (by vote or value) for purposes of section 7874 greater than 50% (for example, the partners held more than 50% of the stock of the foreign corporation)? If “Yes,” list the ownership percentage by vote and by value. See instructions.

Percentage: |

By Vote |

By Value |

29Is the partnership electing out of the centralized partnership audit regime under section 6221(b)? See instructions. If “Yes,” the partnership must complete Schedule

If “No,” complete Designation of Partnership Representative below.

Designation of Partnership Representative (see instructions)

Enter below the information for the partnership representative (PR) for the tax year covered by this return.

Name of PR ▶

U.S. address of PR

▲

U.S. phone number of

PR

▲

If the PR is an entity, name of the designated individual for the PR ▶

U.S. address of |

▲ |

designated individual |

U.S. phone number of designated individual

▲

Form 1065 (2021)

|

Form 1065 (2021) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Partners’ Distributive Share Items |

|

|

|

|

|||||||||

|

Schedule K |

|

|

|

|

|||||||||||

|

|

1 |

Ordinary business income (loss) (page 1, line 22) |

|||||||||||||

|

|

2 |

Net rental real estate income (loss) (attach Form 8825) |

|||||||||||||

|

|

3a |

Other gross rental income (loss) . . |

. . . . . . . . . . . |

3a |

|

||||||||||

|

|

b |

Expenses from other rental activities (attach statement) |

3b |

|

|||||||||||

|

|

c |

Other net rental income (loss). Subtract line 3b from line 3a |

|||||||||||||

|

(Loss) |

4 |

Guaranteed payments: a Services |

|

4a |

|

|

|

b Capital |

4b |

|

|||||

|

|

c Total. Add lines 4a and 4b |

||||||||||||||

|

|

|

||||||||||||||

|

|

5 |

Interest income |

|||||||||||||

|

Income |

6 |

Dividends and dividend equivalents: |

a Ordinary dividends |

||||||||||||

|

|

b Qualified dividends |

6b |

|

|

|

|

|

|

c Dividend equivalents |

6c |

|

||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

7 |

Royalties |

|||||||||||||

|

|

8 |

Net |

|||||||||||||

|

|

9a |

Net |

|||||||||||||

|

|

b |

Collectibles (28%) gain (loss) . . . |

. . . . . . . . . . . |

9b |

|

||||||||||

|

|

c |

Unrecaptured section 1250 gain (attach statement) |

9c |

|

|||||||||||

|

|

10 |

Net section 1231 gain (loss) (attach Form 4797) |

|||||||||||||

|

|

11 |

Other income (loss) (see instructions) |

Type ▶ |

|

|

|

|

||||||||

|

Deductions |

12 |

Section 179 deduction (attach Form 4562) |

|||||||||||||

|

d |

Other deductions (see instructions) |

Type ▶ |

|

|

|

|

|||||||||

|

|

13a |

Contributions |

|||||||||||||

|

|

b |

Investment interest expense |

|||||||||||||

|

|

c |

Section 59(e)(2) expenditures: |

(1) |

Type ▶ |

|

|

|

(2) Amount ▶ |

|||||||

- |

14a |

Net earnings (loss) from |

||||||||||||||

Self- Employ ment |

c |

Gross nonfarm income |

||||||||||||||

|

|

b |

Gross farming or fishing income |

|||||||||||||

|

|

15a |

|

|

|

|

||||||||||

|

Credits |

b |

||||||||||||||

|

c |

Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) . . |

||||||||||||||

|

|

|||||||||||||||

|

|

d |

Other rental real estate credits (see instructions) |

Type ▶ |

|

|

||||||||||

|

|

e |

Other rental credits (see instructions) |

Type ▶ |

|

|

|

|

||||||||

|

International Transactions |

f |

Other credits (see instructions) |

Type ▶ |

|

|

|

|

||||||||

|

16 |

Attach Schedule |

||||||||||||||

|

|

|||||||||||||||

|

|

|

this box to indicate that you are reporting items of international tax relevance |

|||||||||||||

Alternative MinimumTax Items(AMT) |

17a |

|||||||||||||||

b |

Adjusted gain or loss |

|||||||||||||||

c |

Depletion (other than oil and gas) |

|||||||||||||||

|

|

|||||||||||||||

|

|

d |

Oil, gas, and geothermal |

|||||||||||||

|

|

e |

Oil, gas, and geothermal |

|||||||||||||

|

|

f |

Other AMT items (attach statement) |

|||||||||||||

|

Information |

18a |

||||||||||||||

|

b |

Other |

||||||||||||||

|

|

|||||||||||||||

|

|

c |

Nondeductible expenses |

|||||||||||||

|

|

19a |

Distributions of cash and marketable securities |

|||||||||||||

|

|

b |

Distributions of other property |

|||||||||||||

|

Other |

20a |

Investment income |

|||||||||||||

|

b |

Investment expenses |

||||||||||||||

|

|

|||||||||||||||

|

|

c |

Other items and amounts (attach statement) |

|

|

|

|

|||||||||

|

|

21 |

Total foreign taxes paid or accrued |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 4

Total amount

1

2

3c

4c

5

6a

7

8

9a

10

11

12

13a

13b

13c(2)

13d

14a

14b

14c

15a

15b

15c

15d

15e

15f

17a

17b

17c

17d

17e

17f

18a

18b

18c

19a

19b

20a

20b

21

Form 1065 (2021)

Form 1065 (2021) |

Page 5 |

Analysis of Net Income (Loss)

1Net income (loss). Combine Schedule K, lines 1 through 11. From the result, subtract the sum of

|

Schedule K, lines 12 through 13d, and 21 |

. |

. . |

1 |

|

||||

2 |

Analysis by |

(i) Corporate |

(ii) Individual |

(iii) Individual |

(iv) Partnership |

(v) |

Exempt |

|

(vi) |

|

partner type: |

|

(active) |

(passive) |

|

Organization |

Nominee/Other |

||

aGeneral partners

bLimited partners

Schedule L |

|

Balance Sheets per Books |

Beginning of tax year |

|

End of tax year |

||||

|

|

|

Assets |

|

(a) |

(b) |

(c) |

|

(d) |

1 |

Cash |

|

|

|

|

|

|

||

2a |

Trade notes and accounts receivable |

|

|

|

|

|

|

||

b |

Less allowance for bad debts |

|

|

|

|

|

|

||

3 |

Inventories |

|

|

|

|

|

|

||

4 |

U.S. government obligations |

|

|

|

|

|

|

||

5 |

|

|

|

|

|

|

|||

6 |

Other current assets (attach statement) |

|

|

|

|

|

|

||

7a |

Loans to partners (or persons related to partners) . |

|

|

|

|

|

|

||

b |

Mortgage and real estate loans |

|

|

|

|

|

|

||

8 |

Other investments (attach statement) |

|

|

|

|

|

|

||

9a |

Buildings and other depreciable assets |

|

|

|

|

|

|

||

b |

Less accumulated depreciation |

|

|

|

|

|

|

||

10a |

Depletable assets |

|

|

|

|

|

|

||

b |

Less accumulated depletion |

|

|

|

|

|

|

||

11 |

Land (net of any amortization) |

|

|

|

|

|

|

||

12a |

Intangible assets (amortizable only) |

|

|

|

|

|

|

||

b |

Less accumulated amortization |

|

|

|

|

|

|

||

13 |

Other assets (attach statement) |

|

|

|

|

|

|

||

14 |

Total assets |

|

|

|

|

|

|

||

|

|

|

Liabilities and Capital |

|

|

|

|

|

|

15 |

Accounts payable |

|

|

|

|

|

|

||

16 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

||

17 |

Other current liabilities (attach statement) . . . . |

|

|

|

|

|

|

||

18 |

All nonrecourse loans |

|

|

|

|

|

|

||

19a |

Loans from partners (or persons related to partners) . |

|

|

|

|

|

|

||

b |

Mortgages, notes, bonds payable in 1 year or more . |

|

|

|

|

|

|

||

20 |

Other liabilities (attach statement) |

|

|

|

|

|

|

||

21 |

Partners’ capital accounts |

|

|

|

|

|

|||

22 |

Total liabilities and capital |

|

|

|

|

|

|

||

Schedule |

Reconciliation of Income (Loss) per Books With Income (Loss) per Return |

|

|

||||||

Note: The partnership may be required to file Schedule

1Net income (loss) per books . . . .

2Income included on Schedule K, lines 1, 2, 3c, 5, 6a, 7, 8, 9a, 10, and 11, not recorded on books this year (itemize):

3Guaranteed payments (other than health

insurance) . . . . . . . . . .

4Expenses recorded on books this year not included on Schedule K, lines 1 through 13d, and 21 (itemize):

aDepreciation $

bTravel and entertainment $

5Add lines 1 through 4 . . . . . .

Schedule

6Income recorded on books this year not included on Schedule K, lines 1 through 11 (itemize):

a

7Deductions included on Schedule K, lines 1 through 13d, and 21, not charged against book income this year (itemize):

aDepreciation $

8 Add lines 6 and 7 . . . . . . . .

9Income (loss) (Analysis of Net Income (Loss), line 1). Subtract line 8 from line 5

1 |

Balance at beginning of year . . . |

6 |

Distributions: a Cash |

|

2 |

Capital contributed: a Cash . . . |

|

|

b Property |

|

b Property . . |

7 |

Other decreases (itemize): |

|

3 |

Net income (loss) (see instructions) . |

|

|

|

4 |

Other increases (itemize): |

8 |

Add lines 6 and 7 |

|

5 |

Add lines 1 through 4 |

|

9 |

Balance at end of year. Subtract line 8 from line 5 |

Form 1065 (2021)

Document Specifics

| Fact Name | Description |

|---|---|

| Purpose of Form 1065 | Used by partnerships for the tax filing of their annual income, deductions, gains, losses, etc. |

| Due Date | Typically due on March 15th of each year for the preceding tax year. |

| Who Must File | Required for any partnership engaged in trade or business within the United States. |

| Schedule K-1 | Form 1065 includes Schedule K-1, which reports the share of income, deductions, and credits to each partner. |

| Governing Laws | Governed by federal tax law as enforced by the Internal Revenue Service (IRS). |

Guide to Writing IRS 1065

Filing the IRS 1065 form is a critical process for partnerships in the United States, as it facilitates the reporting of their income, gains, losses, deductions, and credits for the tax year. This form helps the Internal Revenue Service (IRS) assess the tax obligations of partnerships and ensures that partners report their share of income on their individual tax returns. To navigate this process efficiently, it's essential to understand the necessary steps. Below is a structured guide to assist you in completing the IRS 1065 form.

- Start by gathering all required financial records for the partnership, including income statements, balance sheets, and receipts for expenses. This comprehensive approach ensures accuracy in reporting.

- Obtain the latest version of the IRS 1065 form from the IRS website. This step is crucial to ensure compliance with current tax laws and regulations.

- Fill in basic information about the partnership at the top of the form, including the name, address, and Employer Identification Number (EIN). This information is vital for the IRS to identify your entity correctly.

- Enter the total income of the partnership in Section 1. This includes gross receipts or sales, minus returns and allowances. Accuracy in this section is paramount for correct tax calculation.

- In Section 2, list the deductions the partnership is claiming. Common deductions include business expenses, such as rent, salaries, and repairs. Documenting these accurately can significantly impact the partnership's taxable income.

- Complete Schedule K of the form, which summarizes the partnership's financial activities for the year. This section details the partners' distributive share items, such as income, losses, and credits.

- Fill out Schedule L, Balance Sheets per Books, if applicable. This requires information on the partnership's assets, liabilities, and capital accounts at the beginning and end of the year.

- If the partnership has any foreign transactions, interests in foreign partnerships, or foreign bank accounts, ensure to fill out the relevant sections or schedules related to these activities.

- Review the form thoroughly to ensure all information is accurate and complete. Errors or omissions can lead to processing delays or audits.

- Sign and date the form. An authorized partner must sign the IRS 1065, attesting to the accuracy of the information provided.

- File the form with the IRS by the deadline, which is typically March 15 for most partnerships. Consider electronic filing for a faster and more secure submission.

After submitting the IRS 1065 form, it's essential to distribute Schedule K-1 to each partner. This document outlines each partner's share of income, deductions, and credits, and is necessary for them to report their individual tax obligations. Staying organized and methodical throughout this process can alleviate stress and ensure compliance with tax obligations.

Understanding IRS 1065

What is the IRS 1065 form?

The IRS 1065 form is a document that partnerships use to report their financial information to the United States Internal Revenue Service (IRS). This report includes income, gains, losses, deductions, and credits of the business. The purpose of the form is for the IRS to assess the partnership's federal income tax liability correctly. However, it's crucial to note that partnerships themselves do not pay income taxes. Instead, this system allows the IRS to ensure that the partners are reporting their income correctly on their individual tax returns.

Who needs to file a Form 1065?

Generally, the requirement to file a Form 1065 applies to any domestic partnership. This term encompasses a broad range of business entities that have two or more owners and have not filed with the IRS to be treated as a corporation. In addition, certain entities with a single owner, classified as a "disregarded entity," that elect to be treated as a partnership for tax purposes must file this form. Foreign partnerships that earn income in the United States or participate in trade or business within the United States are also required to file a Form 1065.

What information do you need to complete Form 1065?

Completing Form 1065 requires detailed financial information about the partnership. Key pieces of information needed include the partnership's income statements, balance sheet data at the beginning and end of the tax year, a record of partners' shares of income, deductions, and credits, as well as information about the partners themselves. Partnerships must also report on allocations of income, gain, loss, deductions, and credits to the partners. Accurate record-keeping throughout the year is essential for efficiently preparing and filing this form.

How does a partnership file Form 1065?

Form 1065 is typically filed electronically through the IRS e-file system, which is efficient and provides immediate confirmation of receipt. However, partnerships that choose can still file paper forms through the mail. The IRS encourages electronic filing for its convenience and accuracy. Regardless of the method chosen, it is imperative that the form is complete and filed by the deadline to avoid penalties. The form's instructions provide a detailed guide on how and where to file, including addressing each line item and required schedules.

When is the deadline to file Form 1065?

The deadline for filing Form 1065 is the 15th day of the third month following the end of the partnership's tax year. For most partnerships operating on a calendar year, this means the deadline is March 15. If the due date falls on a weekend or legal holiday, the deadline is shifted to the next business day. Partnerships needing more time to gather information and complete their filing accurately can request an extension. This extension grants an additional six months to file, moving the deadline to September 15 for those on a calendar year. However, it's important to observe that this extension applies only to the filing of the form, not the payment of any taxes owed.

Common mistakes

-

Not reporting all income: A common mistake is failing to report all income from various sources. All income, including foreign income, should be accurately reported.

-

Mixing personal and business expenses: Sometimes, the expenses are not clearly separated, leading to personal expenses being mistakenly claimed as business deductions.

-

Inaccurate information about partners: Accurately reporting the details of all partners, including their share of profits and losses, is crucial. Errors here can lead to misallocation of income or deductions.

-

Incorrectly categorizing expenses: It's important to categorize expenses correctly to take advantage of various deductions. Miscategorizing can lead to missed deductions or penalties.

-

Overlooking carryover items: These can include net operating losses or capital losses that carry over from previous years. Forgetting these can result in a higher tax liability.

-

Failing to sign and date the form: It sounds simple, but forgetting to sign and date the form can result in it being considered invalid.

-

Misunderstanding partnership agreements: Misinterpreting the terms of a partnership agreement can lead to incorrect reporting of distributions and allocations.

-

Omitting foreign transactions: Not reporting transactions with foreign partners or operations can lead to penalties and interest on any unpaid taxes resulting from those earnings.

-

Miscalculating deductions: It's easy to make arithmetic errors or misunderstand what qualifies for a deduction, leading to an overstated or understated tax liability.

Addressing these mistakes requires attention to detail and a deep understanding of tax laws relevant to partnerships. Consulting a tax professional is always advisable when dealing with complex tax documents like the IRS Form 1065.

Documents used along the form

The IRS Form 1065 is a crucial document for partnerships, detailing their income, gains, losses, deductions, and credits to the Internal Revenue Service. This form helps ensure that partnerships comply with U.S. tax laws by reporting their financial activities accurately. Alongside the Form 1065, there are several other forms and documents that are frequently utilized to complete the partnership's tax obligations thoroughly and accurately. These documents play a vital role in giving a complete financial picture and ensuring compliance with tax laws and regulations.

- Schedule K-1 (Form 1065): This form is an extension of Form 1065 and reports the share of income, deductions, and credits for each partner in a partnership. It's used by the partners to file their individual tax returns.

- Form 4562: This document is used for reporting depreciation and amortization. Partnerships utilize this form to deduct the cost of assets over time on items such as equipment, vehicles, and buildings used in the business.

- Form 8825: Commonly associated with real estate operations within a partnership, this form reports income and expenses related to rental property owned by the partnership, similar to Schedule E used by individual taxpayers.

- Form 2848: This document gives an accountant, attorney, or other designated individual the authority to act on behalf of the partnership in tax matters, allowing them to represent the partnership before the IRS.

- Form 8865: Required for U.S. persons who are involved in certain foreign partnerships, this form reports the activities and financials of the foreign partnership, similar to how Form 1065 is used for domestic partnerships.

- Form 7004: This is an application for an automatic extension of time to file certain business income tax, information, and other returns, allowing partnerships more time to prepare accurate and complete tax documents.

Together, these forms and documents support and expand upon the information provided in Form 1065, ensuring partnerships meet all necessary tax reporting requirements. They assist in capturing the entirety of a partnership's financial activities and are critical for maintaining transparency and adherence to tax laws. Proper completion and submission of these forms help partnerships avoid penalties and ensure each partner pays the correct amount of taxes.

Similar forms

The IRS 1065 form is closely related to the Schedule K-1 (Form 1065), as both are integral to partnership tax filings. The Schedule K-1 is a document used to report each partner's share of the partnership's earnings, losses, deductions, and credits. Essentially, while the IRS 1065 form collects the partnership's aggregate financial information, the Schedule K-1 breaks down that information for each individual partner, ensuring that each partner can accurately report their income on their personal tax returns.

Similarly, the IRS 1120 form shares a connection with the 1065, albeit for corporations. The 1120 form is used by C corporations to report their income, gains, losses, deductions, and credits to the IRS. Like the 1065 form, it serves as a comprehensive report of the entity's financial status for the year. However, it differs as it is designed for corporate entities rather than partnerships, highlighting the tax liabilities based on corporate structures.

The IRS 1120S form is another document related to the 1065, specifically designed for S corporations. This form mimics the purpose of the 1065 by requiring S corporations to report income, losses, deductions, and credits. However, like the Schedule K-1 that accompanies the 1065 form for partnerships, the 1120S also utilizes Schedule K-1 to report each shareholder's share of the corporation's income, illustrating a shared mechanism for passing through income to the individual level.

The IRS 1040 form, commonly known as the U.S. Individual Income Tax Return, has a tangential relation to the 1065 form. Individuals who are partners in partnerships that file Form 1065 must report their share of the partnership's income or loss on their own Form 1040. This process underscores the pass-through nature of partnerships, where the responsibility of paying income tax is on the individual partners rather than on the partnership entity itself.

The Form 8832, Entity Classification Election, plays a pivotal role in how a business entity is taxed, and its election can ultimately determine if a business needs to file Form 1065. By electing to be treated as a different entity type, for example, from a partnership to a corporation, businesses have the flexibility to change how they are taxed, which in turn affects the forms they are required to submit, including possibly transitioning away from Form 1065 to a more appropriate form for their new classification.

Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, is a document required from U.S. persons who control foreign partnerships or hold significant interest in them. Similar to the domestic partnership reporting on Form 1065, Form 8865 collects detailed information about the partnership's financial activities. However, its focus on foreign partnership engagements distinguishes it, serving a critical function in the U.S.'s effort to tax international income.

Form 8995, Qualified Business Income Deduction, is associated with the IRS 1065 in that partnerships may often use this form to calculate the qualified business income deduction for their partners. This deduction, a component of the Tax Cuts and Jobs Act, potentially reduces the taxable income derived from business operations, showing the interplay between individual tax deductions and partnership earnings.

Last, Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations, bears resemblance to the 1065 in the context of reporting requirements for U.S. persons with interests in foreign entities. Though it pertains to corporations rather than partnerships, the principle of requiring detailed financial disclosures to the IRS holds. This ensures transparency and compliance in the international operations of U.S. taxpayers, mirroring the domestic objective of Form 1065 with partnerships.

Dos and Don'ts

Filling out the IRS 1065 form, which is essential for reporting the income, gains, losses, deductions, and credits of a partnership, requires careful attention to detail. To assist in this task, here are seven do’s and don’ts to consider:

Do:- Ensure all the information is accurate and complete. Double-check all entries for errors.

- Use the IRS’s instructions for the 1065 form as a guide. They provide valuable detailed information on how to fill out each part of the form correctly.

- Include all necessary schedules and attachments. Some sections of the 1065 form require detailed information that is provided on separate schedules.

- Provide the Employer Identification Number (EIN) clearly. This number is crucial for identifying the partnership.

- Sign and date the form. An authorized partner or LLC member should sign the 1065 form to validate it.

- Forget to report all income and financial activities. Every piece of income and expense must be reported to avoid issues with the IRS.

- Ignore the deadlines. Submitting the 1065 form late can result in penalties and interest charges.

Misconceptions

The IRS Form 1065 is a crucial document for partnerships in the United States, detailing their profits, losses, deductions, and credits. However, several misconceptions surround this form, leading to confusion and potential issues for filers. Here are ten common misconceptions about the IRS 1065 form, explained to help clear up any confusion.

- Only Large Partnerships Need to File: Regardless of size, any entity operating as a partnership must file Form 1065. This includes small partnerships without significant revenue.

- Filing Form 1065 Means Paying Taxes: Form 1065 itself does not result in a tax bill. It's an informational return that shows how income and losses are allocated among partners, who then report these figures on their individual returns.

- All Partnerships Have the Same Deadlines: Generally, partnerships must file Form 1065 by March 15th for the previous tax year. However, certain partnerships, like fiscal year partnerships, have different deadlines based on their specific fiscal year end.

- Electronic Filing Is Optional: As of recent tax years, partnerships with more than 100 partners are required to file Form 1065 electronically. Smaller partnerships are strongly encouraged to file electronically but may still file paper returns.

- Penalties Are Rare: The IRS imposes penalties for late filing of Form 1065, failure to provide complete information, or both. These penalties can be substantial, emphasizing the importance of timely, accurate filing.

- Personal Information Isn't Required: While Form 1065 is an informational return for the partnership, it requires personal information about the partners, including names, Social Security numbers (or individual taxpayer identification numbers), and addresses, to properly allocate income and loss.

- Amendments Are Unnecessary: If a partnership discovers errors or omissions after filing Form 1065, it should file an amended return. This is crucial to ensure that all partners' tax liabilities are accurate.

- State Filing Isn't Affected: Many states require partnerships to file similar returns at the state level. The information on Form 1065 can affect state tax obligations, making it essential for partnerships to understand their state filing requirements.

- Foreign Partnerships Are Exempt: Foreign partnerships generating income in the U.S. or with U.S. partners must file Form 1065. The global nature of business makes understanding and complying with U.S. tax law critical for international partnerships.

- Profit Distribution Affects Filing Requirements: The requirement to file Form 1065 is not based on whether a partnership distributes profits to its partners. Even if profits are reinvested or held within the partnership, Form 1065 is still required.

Understanding the nuances of Form 1065 is essential for partnerships to comply with U.S. tax law and avoid unnecessary penalties. With clear, accurate information and meeting all filing deadlines, partnerships can ensure they meet their tax obligations without issue.

Key takeaways

The IRS Form 1065 is a requirement for most partnerships and LLCs classified as partnerships for tax purposes in the United States. Its primary function is to report the partnership's income, gains, losses, deductions, and credits to the IRS. Here are six key takeaways regarding filling out and using the IRS 1065 form:

- Understand the Purpose: The Form 1065 is vital for partnerships because it helps determine the share of income or loss each partner should report on their individual tax returns. This form does not calculate tax but allocates income or loss among partners.

- Gather Necessary Information: Before starting the form, ensure you have all requisite financial statements and records for the partnership. This includes items such as the income statement, balance sheet, and documents for deductions or credits.

- Follow Instructions Carefully: The IRS provides instructions for Form 1065 that detail how to fill out each part of the form. It is crucial to follow these instructions closely to avoid mistakes that could lead to audits or penalties.

- Take Note of Deadlines: Generally, the Form 1065 must be filed by the 15th day of the third month following the end of the partnership's tax year. If this deadline cannot be met, it is possible to request an extension using Form 7004.

- Understand the Requirements for Schedules: The Form 1065 includes various schedules that must be completed, depending on the partnership's activities and structure. These schedules report additional financial details, so it's essential to understand which ones apply to your partnership.

- Maintain Accurate Records: Keeping thorough and accurate records is crucial for filling out Form 1065 correctly. This includes not only financial documentation but also partnership agreements and records of each partner's capital contributions and distributions.

Completing the IRS Form 1065 can be complex, but careful attention to these key takeaways can help partnerships comply with tax obligations efficiently. Remember, seeking the assistance of a tax professional is advisable to navigate the intricacies of partnership taxation and ensure accurate and timely filing.

Popular PDF Documents

Form 1099-c - The specific date of the debt’s cancellation is reported on the 1099-C, which is critical for determining tax implications in the relevant year.

How to Issue 1099 - Explanation of benefits and encouragements for electronic filing for filers with fewer than 250 returns, promoting efficiency and accuracy.