Get IRS 1040-NR Form

Filing taxes in the United States can be a daunting task, especially for those who aren't familiar with the American tax system. Among the many forms the Internal Revenue Service (IRS) provides, there's one particularly important for individuals who have come to the U.S. from abroad and do not meet the criteria for resident taxpayers: the IRS Form 1040-NR. This form is designed for nonresident aliens to use when they need to report their income from U.S. sources. It covers a range of incomes including wages, salaries, tips, refunds, and scholarships. Not everyone who earns money in the U.S. is required to file a standard tax return using the Form 1040 or 1040-SR; the 1040-NR serves as an alternative that addresses the unique tax situations of nonresident aliens, ensuring they are taxed only on their U.S.-based income. Understanding when and how to correctly fill out this form is crucial for nonresident aliens wanting to stay compliant with U.S. tax laws, reducing the likelihood of facing penalties or missing out on potential refunds.

IRS 1040-NR Example

Form

Department of the |

(99) |

|

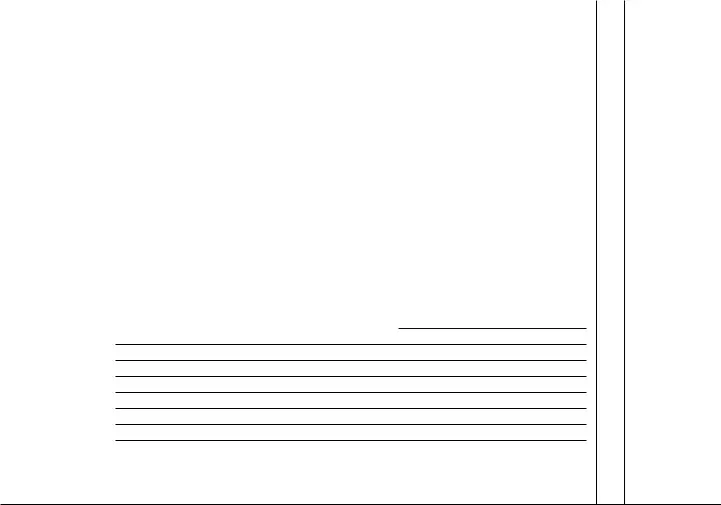

U.S. Nonresident Alien Income Tax Return |

||

2020

OMB No.

IRS Use

or staple in this space.

Filing Status

Check only one box.

Single |

Married filing separately (MFS) (formerly Married) |

Qualifying widow(er) (QW) |

If you checked the QW box, enter the child’s name if the qualifying person is a child but not your dependent ▶

Your first name and middle initial |

Last name |

|

|

Your identifying number |

||

|

|

|

|

|

(see instructions) |

|

|

|

|

|

|

|

|

Home address (number and street or rural route). If you have a P.O. box, see instructions. |

|

Apt. no. |

Check if: |

Individual |

||

|

|

|

|

|

|

Estate or Trust |

|

|

|

|

|

|

|

City, town, or post office. If you have a foreign address, also complete spaces below. |

State |

ZIP code |

|

|

||

|

|

|

|

|

|

|

Foreign country name

Foreign province/state/county

Foreign postal code

At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? |

Yes |

No |

|

|

|

Dependents

(see instructions):

If more than four dependents, see instructions and check here ▶

(1) First name |

Last name |

(2)Dependent’s identifying number

(3)Dependent’s relationship to you

(4)✔ if qualifies for (see instr.):

Child tax credit |

Credit for other |

|

dependents |

||

|

||

|

|

Income Effectively Connected With U.S. Trade or Business

1a Wages, salaries, tips, etc. Attach Form(s)

bScholarship and fellowship grants. Attach Form(s)

cTotal income exempt by a treaty from Schedule OI (Form

|

L, line 1(e) |

. . . . . . . . . . |

1c |

|||

|

|

|

|

|

|

|

2a |

2a |

|

|

b Taxable interest |

||

3a |

Qualified dividends . . . |

3a |

|

|

b Ordinary dividends |

|

4a |

IRA distributions . . . . |

4a |

|

|

b Taxable amount |

|

5a |

Pensions and annuities . . |

5a |

|

|

b Taxable amount |

|

6 |

Reserved for future use |

|||||

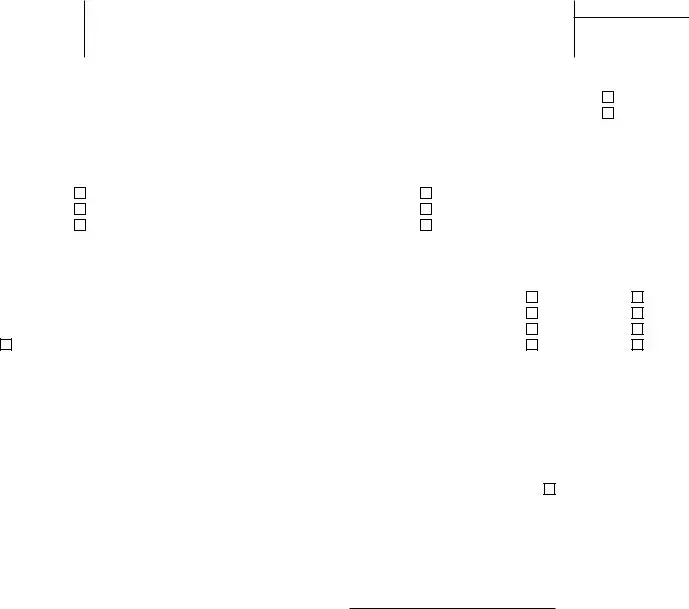

7Capital gain or (loss). Attach Schedule D (Form 1040) if required. If not required, check here . ▶

8 Other income from Schedule 1 (Form 1040), line 9 . . . . . . . . . . . . . . .

9Add lines 1a, 1b, 2b, 3b, 4b, 5b, 7, and 8. This is your total effectively connected income . . ▶

10Adjustments to income:

a |

From Schedule 1 (Form 1040), line 22 |

10a |

|

|

|

|

|

b |

Charitable contributions for certain residents of India. See instructions . |

10b |

|

|

|

|

|

c |

Scholarship and fellowship grants excluded |

10c |

|

|

|

|

|

d |

Add lines 10a through 10c. These are your total adjustments to income . |

. . |

. |

. |

. |

. |

▶ |

11 |

Subtract line 10d from line 9. This is your adjusted gross income . . . |

. . |

. |

. |

. |

. |

▶ |

12Itemized deductions (from Schedule A (Form

|

deduction. See instructions |

|||

13a |

Qualified business income deduction. Attach Form 8995 or Form |

|

13a |

|

|

|

|||

b |

Exemptions for estates and trusts only. See instructions |

|

13b |

|

c |

Add lines 13a and 13b |

|||

14 |

Add lines 12 and 13c |

|||

15 |

Taxable income. Subtract line 14 from line 11. If zero or less, enter |

|||

1a

1b

2b

3b

4b

5b

6

7

8

9

10d

11

12

13c

14

15

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11364D |

Form |

Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 2 |

||||

|

|

16 |

Tax (see instructions). Check if any from Form(s): 1 |

8814 |

2 |

4972 |

3 |

|

|

|

|

|

|

16 |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

17 |

Amount from Schedule 2 (Form 1040), line 3 |

. . . . . |

. . |

|

17 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

18 |

Add lines 16 and 17 |

. . . . . |

. . |

|

18 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

19 |

Child tax credit or credit for other dependents |

. . . . . |

. . |

|

19 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

20 |

Amount from Schedule 3 (Form 1040), line 7 |

. . . . . |

. . |

|

20 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

21 |

Add lines 19 and 20 |

. . . . . |

. . |

|

21 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

22 |

Subtract line 21 from line 18. If zero or less, enter |

. . . . . |

. . |

|

22 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

23a |

Tax on income not effectively connected with a U.S. trade or business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

from Schedule NEC (Form |

|

23a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

b |

Other taxes, including |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

line 10 |

|

23b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

c |

Transportation tax (see instructions) |

|

23c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

d |

Add lines 23a through 23c |

. . . . . |

. . |

|

23d |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

24 |

Add lines 22 and 23d. This is your total tax |

. . . . . |

. |

|

▶ |

|

24 |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

25 |

Federal income tax withheld from: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

a |

Form(s) |

|

25a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

b |

Form(s) 1099 |

|

25b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

c |

Other forms (see instructions) |

|

25c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

d |

Add lines 25a through 25c |

. . . . . |

. . |

|

25d |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

e |

Form(s) 8805 |

. . . . . |

. . |

|

25e |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

f |

Form(s) |

. . . . . |

. . |

|

25f |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

g |

Form(s) |

. . . . . |

. . |

|

25g |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

26 |

2020 estimated tax payments and amount applied from 2019 return . . . |

. . . . . |

. . |

|

26 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

27 |

Reserved for future use |

|

27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

28 |

Additional child tax credit. Attach Schedule 8812 (Form 1040) . . . |

|

28 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

29 |

Credit for amount paid with Form |

|

29 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

30 |

Reserved for future use |

|

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

31 |

Amount from Schedule 3 (Form 1040), line 13 |

|

31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

32 |

Add lines 28 through 31. These are your total other payments and refundable credits . . |

. |

|

▶ |

|

32 |

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

33 |

Add lines 25d, 25e, 25f, 25g, 26, and 32. These are your total payments . |

. . . . . |

. |

|

▶ |

|

33 |

|

|

|

|

|

|

|

|

|

|

|||||||||||

Refund |

34 |

If line 33 is more than line 24, subtract line 24 from line 33. This is the amount you overpaid |

. . |

|

34 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

35a |

Amount of line 34 you want refunded to you. If Form 8888 is attached, check here . . . |

▶ |

|

|

35a |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Direct deposit? |

▶ b |

Routing number |

|

|

|

|

▶ c Type: |

|

Checking |

Savings |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

See instructions. |

▶ d |

Account number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ e |

If you want your refund check mailed to an address outside the United States not shown on page 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

enter it here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36 |

Amount of line 34 you want applied to your 2021 estimated tax |

. |

▶ |

36 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Amount |

37 |

Amount you owe. Subtract line 33 from line 24. For details on how to pay, see instructions . |

. |

|

▶ |

|

37 |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You Owe |

38 |

Estimated tax penalty (see instructions) . |

. . . . . . . . |

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Third Party |

|

Do you want to allow another person (other than your paid preparer) to discuss this |

|

Yes. Complete below. |

|

|

|

No |

||||||||||||||||||||||

Designee |

|

return with the IRS? See instructions |

▶ |

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Other than |

|

Designee’s |

|

|

Phone |

|

|

|

|

Personal identification |

|

|

|

|

|

|

|

|

|

|

||||||||||

paid preparer) |

|

name ▶ |

|

|

no. ▶ |

|

|

|

|

number (PIN) |

|

▶ |

|

|

|

|

|

|

|

|

|

|

||||||||

Sign |

|

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and |

||||||||||||||||||||||||||||

Here |

|

belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

||||||||||||||||||||||||||||

|

Your signature |

|

|

Date |

|

Your occupation |

|

|

|

|

|

|

|

If the IRS sent you an Identity |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

▲ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Protection PIN, enter it here |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(see inst.) ▶ |

|

|

|

|

|

|

|

|

|

|

||

|

|

Phone no. |

|

|

Email address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Paid |

|

Preparer’s name |

|

Preparer’s signature |

|

|

|

|

Date |

PTIN |

|

|

Check if: |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Firm’s name ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s address ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Go to www.irs.gov/Form1040NR for instructions and the latest information. |

Form |

Document Specifics

| Fact Name | Description |

|---|---|

| Form Designation | The IRS Form 1040-NR is designated for nonresident aliens to file their income tax return in the United States. |

| Primary Users | This form is primarily used by individuals who are not U.S. citizens or permanent residents, and who have not passed the green card test or substantial presence test. |

| Income Reporting | Nonresident aliens use Form 1040-NR to report types of income that are subject to U.S. income tax but not effectively connected with a U.S. trade or business. |

| Deductions and Credits | The form allows nonresident aliens to claim deductions and credits that are applicable to them, which may differ from those available to U.S. citizens and residents. |

| Governing Laws | Form 1040-NR is governed by U.S. federal law, specifically the Internal Revenue Code (IRC). |

Guide to Writing IRS 1040-NR

Filling out IRS Form 1040-NR is a critical process for certain taxpayers who have U.S. income but are not citizens or resident aliens. This form ensures compliance with U.S. tax laws and can help in reporting income correctly to avoid penalties. The process involves providing detailed information about your income, deductions, and credits applicable to non-resident aliens. By following the steps outlined below, you can complete this form accurately and efficiently.

- Begin by downloading the latest version of Form 1040-NR from the IRS website. Ensure you have the correct tax year's form.

- Enter your personal information in the designated section at the top of the form. This includes your name, current address, SSN (Social Security Number), or ITIN (Individual Taxpayer Identification Number).

- Go through the Income section carefully. Report all types of income received from U.S. sources, according to the instructions provided for each line.

- In the Deductions section, enter any applicable expenses that you're allowed to claim. Remember, some deductions available to U.S. residents might not be available to non-residents.

- Calculate your Adjusted Gross Income (AGI) by subtracting the deductions from your total income.

- Review the Tax and Credits section. Here, you can claim any credits you're eligible for, which will reduce the total tax due. Calculate the total tax owed following the guidelines provided.

- If applicable, complete the sections for other taxes and payments. This includes any estimated tax payments you have made during the year or payments made when requesting an extension of time to file.

- Subtract your credits and prepayments from the total tax owed to determine if you have a balance due or a refund coming.

- Double-check your form for accuracy. Errors can delay processing and potentially result in penalties.

- Sign and date the form. If you're filing jointly with a spouse, make sure they also sign.

- Attach any required documentation, such as W-2 forms from employers or 1099 forms for other types of income.

- Mail your completed Form 1040-NR to the IRS at the address provided in the form's instructions. The mailing address depends on whether you're enclosing a payment or not.

Completing Form 1040-NR accurately and on time is crucial for maintaining compliance with U.S. tax laws as a non-resident. If you're unsure about any part of the process, consider seeking assistance from a tax professional who is familiar with the tax obligations of non-resident aliens in the U.S. This can help ensure that you're taking advantage of all applicable deductions and credits, ultimately reducing your tax liability where possible.

Understanding IRS 1040-NR

-

What is the IRS 1040-NR form used for?

The IRS 1040-NR form is a document specifically designed for non-resident aliens to file their income tax return in the United States. This form is necessary for individuals who have earned income in the U.S. but do not meet the criteria for being considered a resident for tax purposes. It covers various types of income, deductions, and credits applicable to non-residents.

-

Who needs to file a 1040-NR?

Individuals who need to file a 1040-NR include non-resident aliens engaged in business or trade in the U.S., those who have received income from U.S. sources and are not covered by treaty exemptions, and representatives or agents filing on behalf of a non-resident. Additionally, scholars, students, and certain other visa holders who have received income in the U.S. may also need to file this form.

-

What types of income are reported on the 1040-NR?

- Wages, salaries, or tips earned in the U.S.

- Dividends or interest from U.S. sources.

- Rents or royalties from U.S. properties.

- Scholarships or fellowship grants.

- Gains or losses from the sale of U.S. property.

-

Can I claim any deductions or credits on the 1040-NR?

Yes, non-resident aliens can claim certain deductions and credits on their 1040-NR. These might include expenses related to the income earned in the U.S., such as business expenses, and certain itemized deductions like state and local income taxes or charitable contributions to U.S. organizations. However, the ability to claim these deductions and credits may be limited compared to U.S. residents.

-

How and when do I file the IRS 1040-NR form?

The IRS 1040-NR form can be filed electronically through the IRS website or mailed in paper form. The deadline for filing is typically April 15 of the year following the reported income year. However, if you earned wages subject to withholding, the deadline extends to June 15. It’s important to check the latest IRS guidelines, as deadlines and filing methods may change.

Common mistakes

Filing tax returns can be daunting, and when it comes to the IRS 1040-NR form, specifically designed for nonresident aliens to file their U.S. tax returns, common mistakes can lead to unnecessary problems or delays. Awareness and careful attention to detail can help avoid these pitfalls. Here are nine mistakes to watch out for:

- Not understanding residency status: Many people get confused about their tax residency status. It's important to correctly determine whether you should file as a resident or nonresident for tax purposes.

- Incorrectly reporting income: Sometimes, individuals mistakenly report their income incorrectly. It's crucial to include all sources of U.S.-sourced income as the IRS has ways to track most financial transactions.

- Forgetting to claim tax treaty benefits: Many countries have tax treaties with the U.S. that could reduce or exempt certain types of income from U.S. tax. Forgetting to claim these benefits can lead to overpayment of taxes.

- Missing the deadline: Missing the tax filing deadline can result in penalties and interest. Nonresidents should mark their calendars for April 15, or the next business day if it falls on a weekend or holiday.

- Failing to report worldwide income: If you're considered a resident alien for any part of the tax year, you might need to report global income. This mistake can cause significant legal and financial issues.

- Not including required forms: Filing the 1040-NR often requires additional forms depending on individual circumstances, such as Form 8833 for treaty-based positions. Omission of these forms can lead to processing delays.

- Omitting dependents: Nonresidents might be eligible to claim dependents. Failing to do so can result in a higher tax liability than necessary.

- Incorrect filing status: Choosing the wrong filing status affects your tax rates and available deductions, potentially leading to higher tax bills or future complications with the IRS.

- Overlooking state tax obligations: Finally, it's a common error to ignore state tax filing requirements. Many states have their own tax laws, and filing a federal tax return does not exempt you from state filing obligations.

By steering clear of these errors, you can streamline the process of filing your 1040-NR form, prevent unwelcome surprises, and ensure you pay no more in taxes than you are legally required to.

Documents used along the form

Individuals who are filing Form 1040-NR, the U.S. Nonresident Alien Income Tax Return, may find they need additional forms to accurately complete their tax obligations. This is because the financial situations and sources of income for nonresidents can vary significantly. The forms accompanying the 1040-NR often provide the detailed information necessary for specific types of income, deductions, and credits that affect how much tax is owed or refunded. Understanding these forms can make the filing process smoother and help ensure compliance with U.S. tax laws.

- Form 8843: Statement for Exempt Individuals and Individuals with a Medical Condition. This form is for certain nonresident aliens, including those with F, J, M, or Q visas, to explain why they are exempt from the substantial presence test for considering residency status.

- Form 2555: Foreign Earned Income. Nonresidents who have earned income from foreign sources may use this form to report that income and possibly exclude it from U.S. taxation if certain conditions are met.

- Form 8962: Premium Tax Credit. This form is used to calculate the amount of premium tax credit (PTC) nonresidents are eligible for if they purchased health insurance through the Health Insurance Marketplace, enabling them to either lower their monthly premium payments or claim the credit on their tax return.

- Schedule NEC (Form 1040-NR): Tax on Income Not Effectively Connected with a U.S. Trade or Business. This schedule is specifically for reporting income types that are not connected with a U.S. business, such as dividends, interest, and royalties, which may be taxed at different rates.

- Form 8233: Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual. Nonresidents who earn income as independent contractors or from certain dependent personal services may use this form to claim exemption from withholding if they meet specific criteria based on tax treaty benefits.

- Form 8621: Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund. This form is necessary for nonresidents who have investments in passive foreign investment companies (PFICs) to report earnings and calculate tax liabilities related to those investments.

- Form 1042-S: Foreign Person's U.S. Source Income Subject to Withholding. This document is typically provided by the payer and not filled out by the taxpayer. It reports amounts paid to nonresidents, including wages, scholarships, and fellowship grants, that are subject to U.S. tax withholding.

- Form 5472: Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business. Nonresident aliens who are involved in such businesses may need to file this form to provide information about their business activities and ownership.

- Form 8833: Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b). This form is used by nonresidents who take a tax position based on a treaty between the U.S. and their country of residence, providing details about the position and the relevant treaty articles.

In sum, the forms listed offer a comprehensive snapshot of various scenarios and financial activities that might affect a nonresident's U.S. tax filing requirements. Utilizing these forms in conjunction with Form 1040-NR helps individuals accurately report their income, claim benefits for which they are eligible, and comply with U.S. tax law. It is always advisable for taxpayers to consult with a tax professional to ensure that all applicable forms are correctly completed and submitted.

Similar forms

The IRS 1040-NR form, designated for non-resident aliens to file their U.S. tax returns, shares similarities with several other IRS forms, each tailored to specific financial and residency situations. One notable parallel is with the standard IRS 1040 form, the go-to document for U.S. residents to report their annual income. While both forms are used to report income and calculate taxes owed or refunds due, the 1040 form is broader, catering to U.S. citizens and residents, whereas the 1040-NR is specifically designed for those who do not pass the green card or substantial presence tests but have earned income from U.S. sources.

Another close relative is the IRS 1040-SR form, which is essentially a version of the standard 1040 form but tailored for senior citizens, aged 65 and older. This form offers a larger, easier-to-read font and includes a standard deduction chart that takes into account the taxpayer's age. The similarity to the 1040-NR lies in the intent to simplify the filing process for a specific group of taxpayers, albeit serving different populations with distinct needs related to their age or residency status.

The 1040-NR also mirrors the 1040-NR-EZ, a simpler alternative designed for non-resident aliens with more straightforward tax situations. The 1040-NR-EZ was phased out after the 2018 tax year and incorporated into the 1040-NR, but when it was in use, it offered a streamlined approach for non-residents who had no dependents and only earned wages, salaries, tips, refunds, credits, or scholarships. Its design aimed to make tax filing less daunting, focusing on those with clear-cut income sources and deductions, much like the 1040-NR streamlines filing for non-resident individuals today.

Additionally, the Form 1040-SS closely aligns with the 1040-NR in its purpose to cater to specific segments of filers. The 1040-SS is for residents of U.S. territories, including Puerto Rico, Guam, the U.S. Virgin Islands, the Northern Mariana Islands, and American Samoa. It's for those who are self-employed in these territories and need to report self-employment income. Like the 1040-NR, it addresses a unique taxpayer segment by providing a tailored form that meets their specific reporting requirements and tax situations, acknowledging the distinct financial scenarios faced by residents outside the continental U.S.

Dos and Don'ts

Filling out the IRS 1040-NR form, used by nonresident aliens to file U.S. tax returns, requires careful attention to detail. Here are essential dos and don'ts to consider:

Do:

- Double-check your residency status to ensure the 1040-NR form is the correct form for your situation. Mistakes regarding residency status could result in filing the wrong tax form.

- Gather all necessary documentation, including your income statements, any applicable tax treaties, and identification numbers, before beginning the form. Having all relevant information at hand streamlines the process.

- Use the IRS instructions for the 1040-NR form to guide your completion of the form. These instructions provide valuable information on each section and help clarify any confusion.

- Consider consulting with a tax professional experienced with nonresident tax issues. Tax laws can be complex, and professional guidance can help navigate them more effectively.

Don't:

- Overlook reporting all sources of U.S. income, including wages, scholarships, and dividends. Complete and accurate income reporting is mandatory.

- Forget to claim any applicable treaty benefits that could exempt or reduce your U.S. tax liability. Not taking advantage of these benefits could result in overpaying taxes.

- Misunderstand the due date for filing the 1040-NR form, typically April 15 for the previous year's income. Late submissions may incur penalties and interest charges.

- Ignore the IRS notices regarding your tax return. If the IRS contacts you for additional information or to clarify certain points on your return, timely responding is crucial to avoid further complications.

Misconceptions

Filing taxes in the United States can feel like navigating a labyrinth, particularly for non-residents. The IRS 1040-NR form, exclusively designed for non-resident aliens to report their U.S. source income, is shrouded in complexity and misconceptions. It's crucial to understand what's true and what's not to avoid potential pitfalls. Here are five common misconceptions about the IRS 1040-NR form that need clarifying:

- All non-residents must file the 1040-NR form. Contrary to popular belief, not all non-residents are required to file a 1040-NR form. The need to file depends on various factors, such as the source and type of income received during the tax year. If the income does not meet certain thresholds or criteria set by the IRS, filing may not be necessary.

- The 1040-NR form is only for individuals. While it's primarily used by individuals, it's also pertinent for representatives of deceased individuals, trusts, and estates that need to report income connected with the United States. Understanding the applicability of the 1040-NR form is fundamental to ensuring compliance.

- Filing the 1040-NR form is an annual requirement. This misconception can cause unnecessary stress. The requirement to file the 1040-NR form is contingent on your income, visa status, and other specific tax treaties between the United States and your home country for the given tax year. Always review your circumstances each year to determine if you need to file.

- The process for filing the 1040-NR form is the same each year. Tax laws are dynamic, and changes can affect how forms are completed and submitted. For instance, deductions, credits, and income exclusions evolve, impacting the filing process. It's essential to stay informed about current regulations to ensure accurate filing.

- Married individuals must always file separate 1040-NR forms. While generally true, there are exceptions. Some non-resident aliens, based on tax treaties or specific circumstances, may have the option to file jointly with a spouse. However, this requires careful consideration of the implications and eligibility requirements.

Dispelling these misconceptions about the IRS 1040-NR form is the first step toward smoother navigation of U.S. tax obligations for non-residents. For accurate and tailored advice, consulting with tax professionals knowledgeable about non-resident tax issues is advisable. Staying informed and diligent is key to managing your tax responsibilities without added anxiety.

Key takeaways

Filing taxes in the United States can seem daunting, especially for those who are not citizens but find themselves needing to do so. The IRS 1040-NR form is specifically designed for nonresident aliens to file their U.S. tax returns. Understanding the essentials of filling out and utilizing this form can help simplify the process. Here are seven key takeaways to consider:

- Who Should Use It: The IRS 1040-NR form is intended for nonresident aliens engaged in business in the U.S. or receiving income from U.S. sources. Determining residency status is crucial before starting this form.

- Income Reporting: All types of income received from U.S. sources must be reported. This includes wages, dividends, scholarships, and any other income earned within the U.S.

- Deductions and Credits: Some deductions and credits available to U.S. residents are not available to nonresident filers. However, deductions such as state and local income taxes paid, and certain itemized deductions may still be claimed.

- Dual-Status Taxpayers: Individuals who have both nonresident and resident status during the same tax year may need to file a special form, in addition to the 1040-NR, to account for their dual status.

- Treaty Benefits: Tax treaties between the United States and certain countries can significantly impact how much tax is owed. If an applicable treaty exists, it could reduce or eliminate U.S. tax obligations for some nonresident aliens.

- Deadlines and Extensions: The deadline for filing the 1040-NR form is typically April 15, following the end of the tax year. Nonresident aliens outside the U.S. on the filing deadline are granted an automatic 2-month extension. Further extensions are available but must be requested using the appropriate form.

- State Tax Returns: The requirement to file a state tax return depends on the state where the income was earned. Many states have their own tax forms and rules for nonresidents.

Thoroughly familiarizing oneself with these aspects can help alleviate some of the stress associated with tax filing for nonresident aliens. It's always recommended to seek guidance from a tax professional or the IRS if uncertainties or unique situations arise. By understanding and properly using the IRS 1040-NR form, nonresident aliens can ensure compliance with U.S. tax laws while potentially minimizing their tax liability.

Popular PDF Documents

Ptax 203 - PTAX-203-A's structure supports due diligence, compelling sellers and buyers to verify information that impacts legal and tax obligations.

Driver Contract Agreement With Vehicle Owner - A document that outlines the agreement between AAA Cab Services, Inc. and an individual for the lease of a taxi vehicle.