Get Income Based Repayment Plan Request Form

Navigating the financial responsibilities of student loans can often feel overwhelming, but understanding the options available for repayment can significantly ease this burden. For individuals grappling with Federal Family Education Loan Program (FFELP) loans, the Income-Based Repayment (IBR) Plan Request form serves as a crucial tool. It’s designed to assess eligibility for repayment under the IBR plan, either as a new applicant or for those undergoing the annual reassessment of their payment amounts. Importantly, this plan offers a repayment framework that aligns your monthly loan payments with your income, potentially making your financial obligations more manageable. The form itself requires detailed information, including personal identification, income details, and in some cases, the inclusion of spousal income data, to accurately calculate the repayment terms. It also incorporates stern warnings against the submission of false information, highlighting the legal consequences of such actions. Additionally, instructions included in the document emphasize the importance of thorough reading before completion and outline the necessary steps for submission. With eligibility hinging on criteria such as family size and proof of income, the quest for reduced payments under the IBR plan necessitates a careful compilation of required documentation. This approach not only aids in achieving a fair assessment but also underscores the commitment to making education debt more manageable for borrowers across the spectrum.

Income Based Repayment Plan Request Example

|

|

|

Federal Family Education Loan Program |

|

Use this form for initial determination of your eligibility to repay eligible Federal Family Education Loan Program (FFELP) loans under the |

|

|

IBR |

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on any accompanying documents is subject to |

|

penalties that may include ines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097. |

OMB No.

Form Approved

Exp. Date 04/30/2013

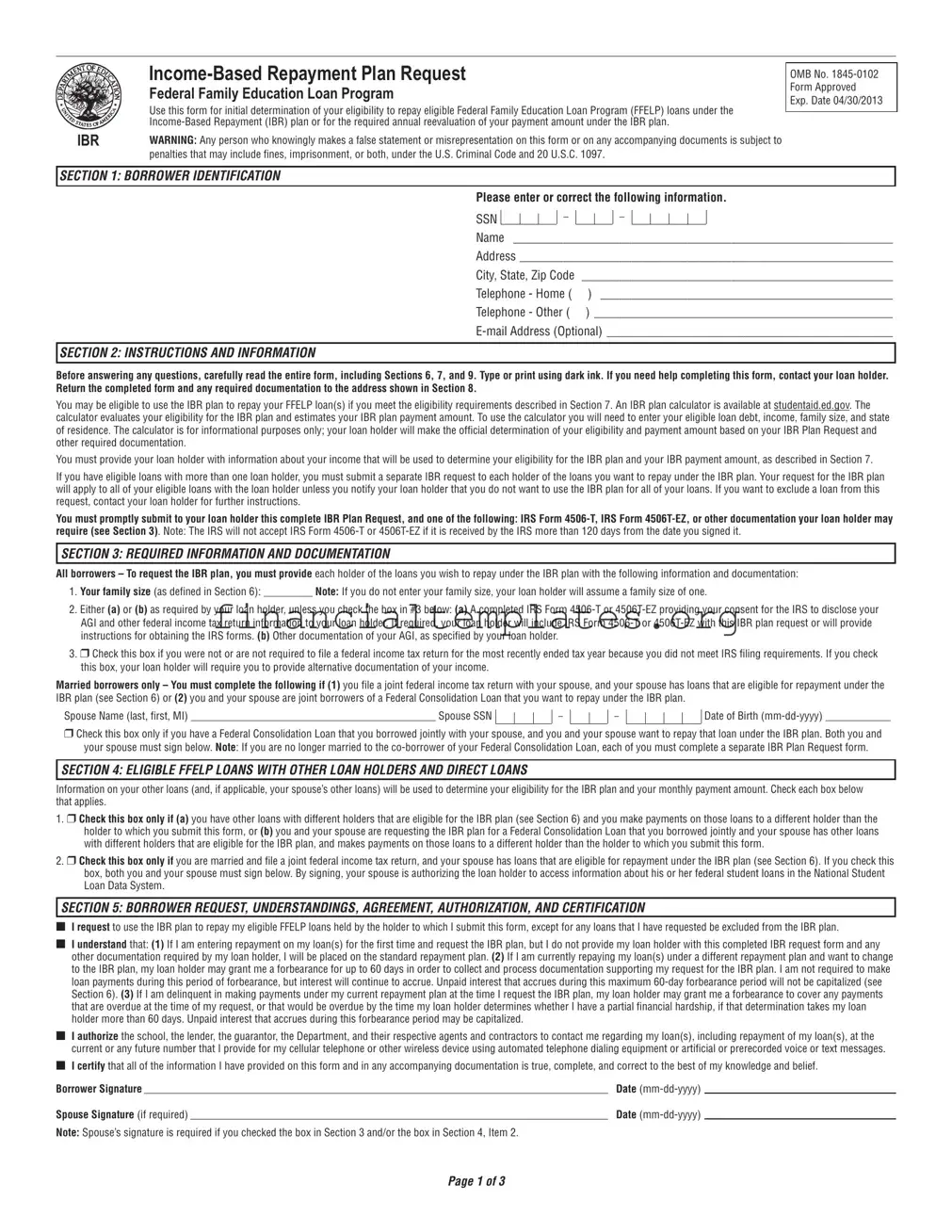

SECTION 1: BORROWER IDENTIFICATION

Please enter or correct the following information.

SSN

Name _____________________________________________________________

Address ____________________________________________________________

City, State, Zip Code __________________________________________________

Telephone - Home ( ) _______________________________________________

Telephone - Other ( ) ________________________________________________

SECTION 2: INSTRUCTIONS AND INFORMATION

Before answering any questions, carefully read the entire form, including Sections 6, 7, and 9. Type or print using dark ink. If you need help completing this form, contact your loan holder. Return the completed form and any required documentation to the address shown in Section 8.

You may be eligible to use the IBR plan to repay your FFELP loan(s) if you meet the eligibility requirements described in Section 7. An IBR plan calculator is available at studentaid.ed.gov. The calculator evaluates your eligibility for the IBR plan and estimates your IBR plan payment amount. To use the calculator you will need to enter your eligible loan debt, income, family size, and state of residence. The calculator is for informational purposes only; your loan holder will make the oficial determination of your eligibility and payment amount based on your IBR Plan Request and other required documentation.

You must provide your loan holder with information about your income that will be used to determine your eligibility for the IBR plan and your IBR payment amount, as described in Section 7.

If you have eligible loans with more than one loan holder, you must submit a separate IBR request to each holder of the loans you want to repay under the IBR plan. Your request for the IBR plan will apply to all of your eligible loans with the loan holder unless you notify your loan holder that you do not want to use the IBR plan for all of your loans. If you want to exclude a loan from this request, contact your loan holder for further instructions.

You must promptly submit to your loan holder this complete IBR Plan Request, and one of the following: IRS Form

require (see Section 3). Note: The IRS will not accept IRS Form

SECTION 3: REQUIRED INFORMATION AND DOCUMENTATION

All borrowers – To request the IBR plan, you must provide each holder of the loans you wish to repay under the IBR plan with the following information and documentation:

1.Your family size (as deined in Section 6): _________ Note: If you do not enter your family size, your loan holder will assume a family size of one.

2.Either (a) or (b) as required by your loan holder, unless you check the box in #3 below: (a) A completed IRS Form

3.r Check this box if you were not or are not required to ile a federal income tax return for the most recently ended tax year because you did not meet IRS iling requirements. If you check this box, your loan holder will require you to provide alternative documentation of your income.

Married borrowers only – You must complete the following if (1) you ile a joint federal income tax return with your spouse, and your spouse has loans that are eligible for repayment under the IBR plan (see Section 6) or (2) you and your spouse are joint borrowers of a Federal Consolidation Loan that you want to repay under the IBR plan.

Spouse Name (last, irst, MI) _____________________________________________ Spouse SSN

Date of Birth

r Check this box only if you have a Federal Consolidation Loan that you borrowed jointly with your spouse, and you and your spouse want to repay that loan under the IBR plan. Both you and your spouse must sign below. Note: If you are no longer married to the

SECTION 4: ELIGIBLE FFELP LOANS WITH OTHER LOAN HOLDERS AND DIRECT LOANS

Information on your other loans (and, if applicable, your spouse’s other loans) will be used to determine your eligibility for the IBR plan and your monthly payment amount. Check each box below that applies.

1.r Check this box only if (a) you have other loans with different holders that are eligible for the IBR plan (see Section 6) and you make payments on those loans to a different holder than the holder to which you submit this form, or (b) you and your spouse are requesting the IBR plan for a Federal Consolidation Loan that you borrowed jointly and your spouse has other loans with different holders that are eligible for the IBR plan, and makes payments on those loans to a different holder than the holder to which you submit this form.

2.r Check this box only if you are married and ile a joint federal income tax return, and your spouse has loans that are eligible for repayment under the IBR plan (see Section 6). If you check this box, both you and your spouse must sign below. By signing, your spouse is authorizing the loan holder to access information about his or her federal student loans in the National Student Loan Data System.

SECTION 5: BORROWER REQUEST, UNDERSTANDINGS, AGREEMENT, AUTHORIZATION, AND CERTIFICATION

nI request to use the IBR plan to repay my eligible FFELP loans held by the holder to which I submit this form, except for any loans that I have requested be excluded from the IBR plan.

nI understand that: (1) If I am entering repayment on my loan(s) for the irst time and request the IBR plan, but I do not provide my loan holder with this completed IBR request form and any other documentation required by my loan holder, I will be placed on the standard repayment plan. (2) If I am currently repaying my loan(s) under a different repayment plan and want to change to the IBR plan, my loan holder may grant me a forbearance for up to 60 days in order to collect and process documentation supporting my request for the IBR plan. I am not required to make loan payments during this period of forbearance, but interest will continue to accrue. Unpaid interest that accrues during this maximum

nI authorize the school, the lender, the guarantor, the Department, and their respective agents and contractors to contact me regarding my loan(s), including repayment of my loan(s), at the current or any future number that I provide for my cellular telephone or other wireless device using automated telephone dialing equipment or artiicial or prerecorded voice or text messages.

nI certify that all of the information I have provided on this form and in any accompanying documentation is true, complete, and correct to the best of my knowledge and belief.

Borrower Signature |

|

Date |

|

Spouse Signature (if required) |

|

Date |

|

Note: Spouse’s signature is required if you checked the box in Section 3 and/or the box in Section 4, Item 2. |

|

||

Page 1 of 3

SECTION 6: DEFINITIONS

n Capitalization is the addition of unpaid interest to the principal balance of your loan. This will increase the principal balance and the total cost of your loan.

n Eligible loans for the IBR plan are FFELP and Direct Loan Program loans other than: (1) a loan that is in default, (2) a Federal or Direct PLUS Loan made to a parent borrower, or (3) a Federal or Direct Consolidation Loan that repaid a Federal or Direct PLUS Loan made to a parent borrower. Federal Perkins Loans, HEAL loans or other health education loans, and private education loans are not eligible for the IBR plan. To access information on all of your federal student loans, check the National Student Loan Data System at www.nslds.ed.gov.

n Family size includes you, your spouse, and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you. It includes other people only if they live with you now, they receive more than half their support from you now, and they will continue to receive this support from you for the year that you certify your family size. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, and payment of college costs.

n The Federal Family Education Loan Program (FFELP) includes Federal Stafford Loans (both subsidized and unsubsidized), Federal PLUS Loans, Federal Consolidation Loans, and Federal Supplemental Loans for Students (SLS).

n The holder of your FFELP loan(s) may be a lender or the U.S. Department of Education (the Department). The holder of Direct Loan Program loans is the Department. Your loan holder may use a servicer to handle billing and other communications related to your loan(s). If your loan holder uses a servicer, the term “holder” as used throughout this form may also refer to the servicer.

n

n Partial inancial hardship is when the annual amount due on all of your eligible loans or, if you are married and ile a joint federal income tax return, the annual amount due on all of your eligible loans and your spouse’s eligible loans, exceeds 15% of the difference between your adjusted gross income (AGI), as shown on your most recently iled federal income tax return, and 150% of the annual poverty guideline amount for your family size and state of residence:

Annual amount of payments due > 15% [AGI – (150% x applicable poverty guideline amount)]

The annual amount of payments due is calculated based on the greater of (1) the total amount owed on eligible loans at the time those loans initially entered repayment or

(2)the total amount owed on eligible loans at the time you or, if applicable, your spouse requested the IBR plan. The annual amount of payments due is calculated using a standard repayment plan with a

ile a joint federal income tax return, the amount owed on your spouse’s eligible loans. If you are married and ile a joint federal income tax return, your AGI includes your spouse’s income.

n Poverty guideline amount is the igure for your state and family size from the poverty guidelines published annually by the U.S. Department of Health and Human Services (HHS). The HHS poverty guidelines are used for purposes such as determining eligibility for certain federal beneit programs. If you are not a resident of a state identiied in the poverty guidelines, your poverty guideline amount is the amount used for the 48 contiguous states.

n The William D. Ford Federal Direct Loan (Direct Loan) Program includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

SECTION 7: ELIGIBILITY CRITERIA

Important information about the IBR plan includes:

n You may use the IBR plan to repay your eligible FFELP loan(s), as deined in Section 6.

n To initially qualify to repay your loan(s) under the IBR plan and to continue to qualify to make

n You must submit required information about your income to your loan holder for determination of your eligibility for the IBR plan and your IBR payment amount. You must provide your loan holder with Internal Revenue Service (IRS) Form

n When you have a partial inancial hardship, your monthly payment amount under the IBR plan will not exceed 15% of the amount by which your AGI exceeds 150% of the poverty guideline amount for your family size and state of residence, divided by 12:

Monthly payment = 15% [AGI – (150% x applicable poverty guideline amount)] ÷ 12

n After entry into the IBR plan, you must annually certify your family size and provide income documentation for determination of whether you have a partial inancial hardship. Your monthly payment amount for the IBR plan may be adjusted annually. It may be higher or lower, depending on the income documentation and family size information you provide each year. Your loan holder will notify you when you are required to provide this documentation.

n For any year you do not have a partial inancial hardship, your payment amount will be the payment amount for your loan(s) under the standard repayment plan with a

n In some circumstances your IBR plan monthly payment amount may not cover all interest that accrues, and your debt may increase. While you are in repayment under IBR, if your monthly payment amount does not cover all interest that accrues each month, the U.S. Department of Education will pay the unpaid interest on your subsidized Stafford loan(s) and on the subsidized portion of your Federal Consolidation Loan(s) for not more than the irst 3 consecutive years after you initially enter the IBR plan. If you receive an economic hardship deferment during this

n Accrued interest is capitalized at the time you choose to leave the IBR plan or no longer have a partial inancial hardship.

n If your loan(s) is not repaid in full after you have made the equivalent of 25 years of qualifying monthly payments and at least 25 years have elapsed, any remaining debt will be eligible for forgiveness. If you receive an economic hardship deferment, any months of economic hardship deferment are considered the equivalent of qualifying payments. Months for which you receive any other type of deferment or months of forbearance are not counted as qualifying payments, and do not count toward the

SECTION 8: WHERE TO SEND THE COMPLETED

Return the completed IBR Plan Request and any required documentation to: (If no address is shown, return to your loan holder.)

NELNET

P.O. BOX 82565

LINCOLN, NE

FAX: 1.866.545.9196

If you need help completing this form, call:

(If no telephone number is shown, call your loan holder.)

Page 2 of 3

SECTION 9: IMPORTANT NOTICES

Privacy Act Notice

The Privacy Act of 1974 (5 U.S.C. 552a) requires that the following notice be provided to you:

The authority for collecting the requested information from and about you is §428(b)(2)(A) et seq. of the Higher Education Act (HEA) of 1965, as amended (20 U.S.C. 1078(b)(2)(A) et seq.) and the authorities for collecting and using your Social Security Number (SSN) are §484(a)(4) of the HEA (20 U.S.C. 1091(a)(4)) and 31 U.S.C. 7701(b). Participating in the Federal Family Education Loan (FFEL) Program and giving us your SSN are voluntary, but you must provide the requested information, including your SSN, to participate.

The principal purposes for collecting the information on this form, including your SSN, are to verify your identity, to determine your eligibility to receive a loan or a beneit on a loan (such as a deferment, forbearance, discharge, or forgiveness) under the FFEL Program, to permit the servicing of your loan(s), and, if it becomes necessary, to locate you and to collect and report on your loan(s) if your loan(s) become delinquent or in default. We also use your SSN as an account identiier and to permit you to access your account information electronically. The information in your ile may be disclosed, on a

in order to verify your identity, to determine your eligibility to receive a loan or a beneit on a loan, to permit the servicing or collection of your loan(s), to enforce the terms of the loan(s), to investigate possible fraud and to verify compliance with federal student inancial aid program regulations, or to locate you if you become delinquent in your loan payments or if you default. To provide default rate calculations, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to state agencies. To provide inancial aid history information, disclosures may be made to educational institutions. To assist program administrators with tracking refunds and cancellations, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to federal or state agencies. To provide a standardized method for educational institutions eficiently to submit student enrollment status, disclosures may be made to guaranty agencies or to inancial and educational institutions. To counsel you in repayment efforts, disclosures may be made to guaranty agencies, to inancial and educational institutions, or to federal, state, or local agencies.

In the event of litigation, we may send records to the Department of Justice, a court, adjudicative body, counsel, party, or witness if the disclosure is relevant and necessary to the litigation. If this information, either alone or with other information, indicates a potential violation of law, we may send it to the appropriate authority for action. We may send information to members of Congress if you ask them to help you with federal student aid questions. In circumstances involving employment complaints, grievances, or disciplinary actions, we may disclose relevant records to adjudicate or investigate the issues. If provided for by a collective bargaining agreement, we may disclose records to a labor organization recognized under 5 U.S.C. Chapter 71. Disclosures may be made to our contractors for the purpose of performing any programmatic function that requires disclosure of records. Before making any such disclosure, we will require the contractor to maintain Privacy Act safeguards. Disclosures may also be made to qualiied researchers under Privacy

Act safeguards.

Paperwork Reduction Notice

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. The valid OMB control number for this information collection is

U.S. Department of Education, Washington, DC

If you have any comments or concerns regarding the status of your individual submission of this form, write directly to the address shown in Section 8.

Page 3 of 3

Document Specifics

| Fact Name | Description |

|---|---|

| Form Purpose | Used for the initial determination of eligibility for the Income-Based Repayment (IBR) plan or for the annual reevaluation of the payment amount under the IBR plan for loans under the Federal Family Education Loan Program (FFELP). |

| Warning for Misrepresentation | Submitting false information on the form or any accompanying documents can result in fines, imprisonment, or both under the U.S. Criminal Code and 20 U.S.C. 1097. |

| OMB Approval | The form is approved with OMB No. 1845-0102 and had an expiration date of 04/30/2013. |

| Eligibility for IBR Plan | Eligibility is based on the borrower demonstrating a partial financial hardship, with eligibility and payment amounts determined by the borrower's income, family size, and state of residence. |

| Documentation Required | Borrowers must provide income documentation using IRS Form 4506-T, IRS Form 4506T-EZ, or other documentation as required for determining eligibility and payment amount. |

| Privacy and Paperwork Reduction Notices | Outlines how the collected information is used, including verification of identity and eligibility for benefits, and mentions the Paperwork Reduction Act of 1995, indicating the OMB control number and the estimated time to complete the form. |

Guide to Writing Income Based Repayment Plan Request

Filling out the Income-Based Repayment Plan Request form is a pivotal step for those with Federal Family Education Loan Program (FFELP) loans seeking relief in their monthly student loan payments. The process demands attention to detail to ensure accurate completion and submission. Remember, providing false information can lead to severe penalties. Here is how you can successfully navigate through the form:

- Section 1 - Borrower Identification: Start by providing your social security number (SSN), full name, address, city, state, zip code, home phone number, and an alternative number if applicable. An email address is optional but recommended.

- Read Through the Form: Before jumping into filling out the sections, thoroughly read all instructions and information presented, especially Sections 6, 7, and 9. This will help in understanding the eligibility criteria and what the form entails.

- Section 2 - Instructions and Information: No action needed here, but ensure you comprehend the details about eligibility, required documentation, and where to return the completed form.

- Section 3 - Required Information and Documentation:

- Indicate your family size.

- Choose either option (a) or (b) for income verification. Option (a) involves completing IRS Form 4506-T or 4506T-EZ. Option (b) requires providing alternative documentation of your adjusted gross income (AGI) as specified by your loan holder.

- Tick the box if you were not required to file a federal income tax return for the most recent tax year.

- Married Borrowers: If applicable, fill out the spouse's section with their name, SSN, and date of birth. Check the box if you have a Federal Consolidation Loan that you borrowed jointly with your spouse and wish to repay under the IBR plan.

- Section 4 - Eligible FFELP Loans With Other Loan Holders and Direct Loans: Identify if you or your spouse, if married filing jointly, have other loans eligible for the IBR plan or if payments are made to different holders.

- Section 5 - Borrower Request, Understandings, Agreement, Authorization, and Certification: Review the understandings and agreements, then sign and date the form. If a spouse’s information is included, their signature is also required.

After thoroughly completing the form and gathering any necessary documentation, such as the IRS Form 4506-T or alternative income documents, submit everything to the address listed in Section 8. Keep in mind, a detailed review of the instructions and accurate reporting of information will smoothly facilitate the processing of your Income-Based Repayment Plan Request.

Understanding Income Based Repayment Plan Request

Who is eligible for the Income-Based Repayment Plan?

Eligibility for the Income-Based Repayment Plan (IBR) primarily depends on whether you have a partial financial hardship. This is determined by comparing your income to your family size and state of residence, against the debt of your eligible Federal Family Education Loan Program (FFELP) loans. To qualify, the annual amount due on all of your eligible loans must exceed 15% of the difference between your adjusted gross income (AGI) and 150% of the poverty guideline for your state and family size.

What loans are eligible for repayment under the IBR plan?

Eligible loans under the IBR plan include most FFELP and Direct Loan Program loans, excluding loans that are in default, Federal or Direct PLUS Loans made to parent borrowers, or Federal or Direct Consolidation Loans that repaid a Federal or Direct PLUS Loan made to a parent borrower. Federal Perkins Loans, HEAL loans, other health education loans, and private education loans are not eligible.

How do I apply for the IBR plan?

To apply for the IBR plan, you must submit a completed Income-Based Repayment Plan Request form to each holder of the loans you wish to repay under the IBR plan. You need to provide documentation of your income, which might include a completed IRS Form 4506-T or 4506T-EZ, alternative documentation of your income if you didn't file a tax return, or other documentation as specified by your loan holder.

What if my income has changed since my last tax return?

If your current income doesn't accurately reflect what's reported on your most recent tax return, or you weren't required to file a tax return, you must provide your loan holder with alternative documentation of your income. This could involve detailed information about your current income level, as required by your loan holder, to make an accurate assessment of your eligibility for the IBR plan.

What happens if I am eligible for the IBR plan?

If you're eligible for the IBR plan, your monthly payment will not be more than 15% of the difference between your AGI and 150% of the poverty guideline, divided by 12. This ensures your payments are manageable based on your income and family size. Additionally, if your annual income changes, you must recertify your information annually, which might adjust your monthly payments.

What if my spouse also has student loans?

If you're married and file a joint federal income tax return, you must include information about your spouse's eligible loans if they are applying for the IBR plan as well. Your spouse's signature will also be required on the IBR Plan Request form. If you have a joint Federal Consolidation Loan, both you and your spouse must agree to repay under the IBR plan.

What happens to the interest if my monthly payments under IBR do not cover it?

If your IBR payment amount does not cover the monthly interest that accrues on your loans, the unpaid interest may be capitalized or added to the principal balance of your loans, increasing the total cost. However, for the first three years of your IBR plan, the U.S. Department of Education may pay the unpaid interest on your subsidized loans. After this period, any accruing but unpaid interest could capitalize.

Common mistakes

Filling out an Income Based Repayment (IBR) Plan Request form for the Federal Family Education Loan Program (FFELP) requires careful attention to detail. Unfortunately, people often make mistakes that can delay or affect their eligibility for the IBR plan. Here are eight common errors:

- Not reading the entire form carefully before starting: The form comes with specific instructions and information in various sections that are essential for accurately completing the request.

- Incorrect or incomplete borrower identification information: It's vital to ensure that all personal information, including Social Security Number, name, address, and contact information, is filled out correctly and completely.

- Failing to accurately report family size: Your family size affects your payment calculation. Missing or incorrect family size can lead to incorrect payment calculations.

- Skipping income documentation: Proper documentation of your Adjusted Gross Income (AGI) is crucial. Whether it's through the IRS Form 4506-T, 4506T-EZ, or alternative documentation, failing to submit any of these can stall the application process.

- Overlooking the requirement for annual reevaluation: The IBR plan requires annual submission of income and family size documentation to adjust the payment amount. Neglecting this requirement can lead to unexpected payment amounts.

- Not submitting separate requests for loans with different loan holders: If you have eligible loans with more than one holder, each must receive a separate IBR Request form.

- Incorrectly handling spousal information: For married borrowers who file jointly and have eligible loans, it is crucial to provide accurate information about both spouses. Errors or omissions here can affect eligibility and payment calculations.

- Failing to provide required signatures: The form requires the borrower's signature and, in some cases, the spouse's signature. Missing signatures can invalidate the request.

To avoid these mistakes, applicants should thoroughly review the form, gather all necessary information before starting, and carefully follow all instructions provided. By doing so, borrowers can ensure a smoother process in determining their eligibility and payment amount under the IBR plan.

Documents used along the form

When applying for an Income-Based Repayment Plan for federal student loans, applicants must often provide additional documentation to support their request. This ensures an accurate assessment of their financial situation, enabling them to receive a payment plan that reflects their ability to pay. This can be a stressful process, but understanding the required forms and documents can ease some of that burden.

- IRS Form 4506-T (Request for Transcript of Tax Return): This form allows the loan servicer to request a transcript of your tax return directly from the IRS. It's used to verify your income if you don't have a copy of your recent tax return or if the loan servicer requires more detailed information about your financial situation.

- Alternative Documentation of Income: For applicants who don't file taxes or whose current income significantly differs from their most recently filed tax return, loan servicers may allow for alternative documentation. This could include pay stubs, a letter from your employer detailing your income, or other documents that prove current earnings.

- Employment Certification Form: For those working in public service and interested in the Public Service Loan Forgiveness (PSLF) program, this form certifies your employment with a qualifying employer. While not directly part of the IBR application, it’s often submitted in conjunction to ensure that payments count towards PSLF qualifying payments.

- Income-Driven Repayment Plan Annual Recertification Form: Once enrolled in an income-driven repayment plan like IBR, borrowers must recertify their income and family size each year. This form collects updated financial information to adjust the payment plan according to any changes in income or family size.

- Family Size Documentation: If your family size changes or differs from the last tax filing, you may need to provide evidence of this change. Documents such as birth certificates or court orders for dependents can support claims of an increased family size, which can lower monthly payment amounts.

Collecting and submitting these forms and documents can be the first steps toward gaining peace of mind regarding federal student loan payments. Borrowers are encouraged to approach this process with care to ensure all provided information is accurate and complete, which helps in receiving the most beneficial repayment terms for their situation.

Similar forms

The Public Service Loan Forgiveness (PSLF) Application for Forgiveness closely mirrors the Income-Based Repayment Plan Request form in purpose and structure. Both documents are designed for individuals seeking relief from their federal student loan debt under specific criteria. While the IBR Request Form helps borrowers adjust their monthly payment based on their income and family size, the PSLF Application targets borrowers employed in public service jobs, offering loan forgiveness after 120 qualifying payments. Each form requires detailed borrower information, loan data, and employment verification to assess eligibility.

Revised Pay As You Earn (REPAYE) Plan application forms are similarly structured to the Income-Based Repayment Plan Request form. REPAYE, like IBR, is another income-driven repayment plan that adjusts borrowers’ monthly payments based on their income and family size. Both forms necessitate borrowers to provide personal information, financial details, and sometimes spouse’s information to calculate the payment amount. They both involve certifying family size and providing documentation of income to determine the borrower's payment obligation.

The Income-Contingent Repayment (ICR) Plan application also shares several commonalities with the IBR Request Form. ICR is designed for Direct Loan Program borrowers and calculates payments based on adjusted gross income, family size, and total federal student loan balance. Both forms are crucial for borrowers seeking a repayment plan that accommodates their financial situation, requiring comprehensive financial information and authorization for the Department of Education to access tax return information for income verification.

The Pay As You Earn (PAYE) Plan application is alike in its requirements and objectives to the IBR Plan Request form. Both are intended for borrowers with a high debt-to-income ratio, offering manageable monthly payments that are a percentage of discretionary income. These forms similarly ask borrowers to document their income, family size, and federal student loan debt to evaluate eligibility for lower payment options under federal guidelines.

The Application for Deferment of Student Loans is similar in the sense that it also provides a form of financial relief for borrowers, though through a different mechanism. While IBR offers the opportunity to reduce monthly payment amounts based on income, deferment temporarily suspends payments due to particular life circumstances such as unemployment or economic hardship. Both applications require proof of the borrower's current financial state and detailed personal information.

The Economic Hardship Deferment Request form parallels the IBR Request Form in its aim to assist borrowers facing difficult financial situations. It allows for a temporary suspension of payment obligations under certain conditions of economic hardship. Both forms demand a demonstration of financial circumstances, with the Economic Hardship form specifically focusing on income, family size, and employment status to qualify for deferment.

The Federal Loan Consolidation Application shares a likeness with the IBR Request Form in terms of managing student loan debt. Consolidation allows borrowers to combine multiple federal student loans into one, potentially lowering monthly payments or qualifying for income-driven repayment plans like IBR. Both applications involve providing detailed loan information, personal details, and often a re-evaluation of financial status to determine new payment terms.

The Forbearance Request Forms for federal student loans similarly help borrowers struggling with loan payments. While forbearance, like deferment, offers a pause on payments, it differs from IBR’s approach to reduce payments based on income. Nonetheless, both forms require borrowers to disclose their financial hardship and personal information to be granted relief.

The Total and Permanent Disability Discharge (TPD) application is akin to the IBR Request Form in its purpose to alleviate the burden of student loans under specific conditions. TPD discharge applies to borrowers who are unable to work due to a disability, while IBR is tailored to those with financial hardship. Both necessitate substantial documentation to prove the borrower's condition - financial or medical - to qualify for loan forgiveness or reduced payments.

The Teacher Loan Forgiveness Application also shares similarities with the IBR Request Form, focusing on the theme of loan relief for eligible applicants. It targets teachers working in low-income schools or educational service agencies, offering forgiveness after five consecutive years of service. Like the IBR form, it requires detailed employment verification, borrower information, and understanding of the program criteria to forgive a portion of the borrower's federal student loan debt.

Dos and Don'ts

Applying for an Income-Based Repayment (IBR) Plan requires careful attention to detail and completeness to ensure your request is processed accurately and efficiently. Below are 10 essential dos and don'ts to consider when filling out your IBR Plan Request form.

- Do read the entire form carefully before filling it out, including Sections 6, 7, and 9, to ensure you understand all requirements and instructions.

- Do use dark ink if you are filling out the form by hand to ensure all information is legible.

- Do provide accurate and updated borrower identification, including your Social Security Number, address, and contact details, as requested in Section 1.

- Do accurately report your family size in Section 3 since it significantly impacts your payment calculation under the IBR plan.

- Do provide complete documentation of your income as detailed in Section 3, which might include IRS Forms 4506-T or 4506T-EZ, or alternative documentation if you weren't required to file a tax return.

- Do contact your loan holder if you need assistance completing the form or have questions. Their contact information is provided in Section 8.

- Do include information about all eligible loans you wish to be considered under the IBR plan, following instructions in Section 4.

- Don't leave sections blank. If a section does not apply to you, indicate this with "N/A" or "0" as appropriate. Incomplete forms may delay processing.

- Don't forget to sign and date the form in Section 5. If applicable, your spouse’s signature is also required.

- Don't withhold information or make false statements. As noted under the IBR WARNING, doing so could lead to penalties, including fines or imprisonment, under U.S. law.

By following these guidelines, you'll help ensure your Income-Based Repayment Plan Request is completed accurately and efficiently, paving the way for a smoother processing of your application.

Misconceptions

When it comes to managing student loan debt, many borrowers consider Income-Based Repayment (IBR) plans as a viable option. However, misconceptions about the IBR Plan Request form can lead to confusion and missteps. Let's clear up some of these misunderstandings:

- Eligibility is only based on income: While income is a critical factor in determining eligibility for the IBR plan, it's not the only one. Family size and state of residence also play significant roles in the calculation. This misconception might lead some borrowers to think they don't qualify when they might, or vice versa. The formula considers the borrower's income relative to their family size and the poverty guideline for their state to determine a potential partial financial hardship.

- Submitting the form guarantees enrollment in IBR: Simply submitting the IBR Plan Request form does not ensure enrolment in the plan. Approval depends on several factors, including the verification of income and family size and meeting the eligibility criteria for a partial financial hardship. The form is the first step in the process, but borrowers must provide all required documentation and meet the specific requirements outlined in the form.

- Marriage status does not matter: If borrowers are married and file taxes jointly, their spouse's income and federal student loan debt are considered in the IBR eligibility and payment calculation. This aspect can significantly affect the payment amount and eligibility for the plan, contrary to the belief that marriage status is irrelevant. Therefore, it's important for married borrowers to understand how their and their spouse's financial information will impact their IBR application.

- IBR payments cover all accrued interest: Under the IBR plan, it's possible for the monthly payment amount to not fully cover the accrued interest on the loan. For subsidized loans, the government may pay the unpaid interest for up to three consecutive years if the IBR payment doesn't cover it. After this period, or for unsubsidized loans, the unpaid interest could capitalize, adding to the total loan balance. Many borrowers mistakenly believe that their IBR payments will always cover interest charges, not realizing the potential for their balance to grow if not all interest is paid.

Navigating student loan repayment plans can be tricky, and understanding the nuances of each option is crucial for making informed decisions. By debunking these common myths about the IBR Plan Request form, borrowers can better evaluate if the IBR plan is the right choice for their financial situations.

Key takeaways

When considering the Income-Based Repayment Plan Request for Federal Family Education Loan Program (FFELP) loans, it is important to understand several key points:

- Eligibility and Documentation: Eligibility for the Income-Based Repayment (IBR) plan is determined based on your income, family size, and state of residence. You must provide accurate income information through IRS Form 4506-T, 4506T-EZ, or alternative documentation as required by the loan holder to assess your eligibility and calculate your repayment amount.

- Annual Reevaluation: Enrollment in the IBR plan requires an annual reevaluation of your payment amount. This involves yearly submission of your income and family size information to continue qualifying for income-based payments. Failure to recertify annually can result in removal from the IBR plan and adjustment to a different repayment plan, potentially increasing your monthly payment.

- Accuracy and Honesty: It is critical to provide truthful and complete information on the IBR Plan Request and accompanying documents. False statements or misrepresentations can lead to severe penalties, including fines and imprisonment, under the U.S. Criminal Code and 20 U.S.C. 1097.

- Impact on Loan Forgiveness: The IBR plan offers a path to loan forgiveness after making the equivalent of 25 years of qualifying monthly payments. Accurate reporting and compliance with annual reevaluation requirements are essential to remain on track for forgiveness.

- Spousal Information: If you are married and file a joint federal income tax return, you must include your spouse's income and loan information if they also have eligible FFELP loans. This can affect your payment calculation and eligibility for the IBR plan.

By adhering to these key points, borrowers can navigate the requirements of the IBR Plan Request form effectively, ensuring they make the most of their repayment options for FFELP loans.

Popular PDF Documents

Ptax 203 - By compiling months on the market and occupancy rates, PTAX-203-A assists in gauging the property's appeal and market conditions.

Form 500 Instructions - Clarifies the importance of specifying the fiscal year-end and accounting method for your Georgia business.