Get Income Based Repayment Form

Navigating the financial responsibility of student loans can sometimes feel overwhelming, but the Income-Based Repayment (IBR) plan offers a potential solution for managing this burden relative to one's income and family size. Designed to make monthly loan payments more manageable, applicants are encouraged to review the application packet thoroughly and follow the included tips for completion. The process requires individuals to complete sections on personal information, indicate their choice for the IBR plan, provide spouse details if applicable, and skip unrelated sections. Crucially, documentation such as tax returns must accompany the application to verify income, alongside completing additional forms if recent tax filings were not made or if income has significantly changed or is non-existent. For those transitioning from deferment or forbearance, a specific request form is included to initiate payments under IBR. With paperwork in order, applications are mailed to FedLoan Servicing, with a clear reminder to double-check for common errors, especially regarding tax information and income verification, to ensure the application process proceeds smoothly. This structured approach to applying for IBR underscores its potential to alleviate some of the financial strain of student loans, offering a tailored plan that takes into consideration the unique circumstances of each borrower.

Income Based Repayment Example

The

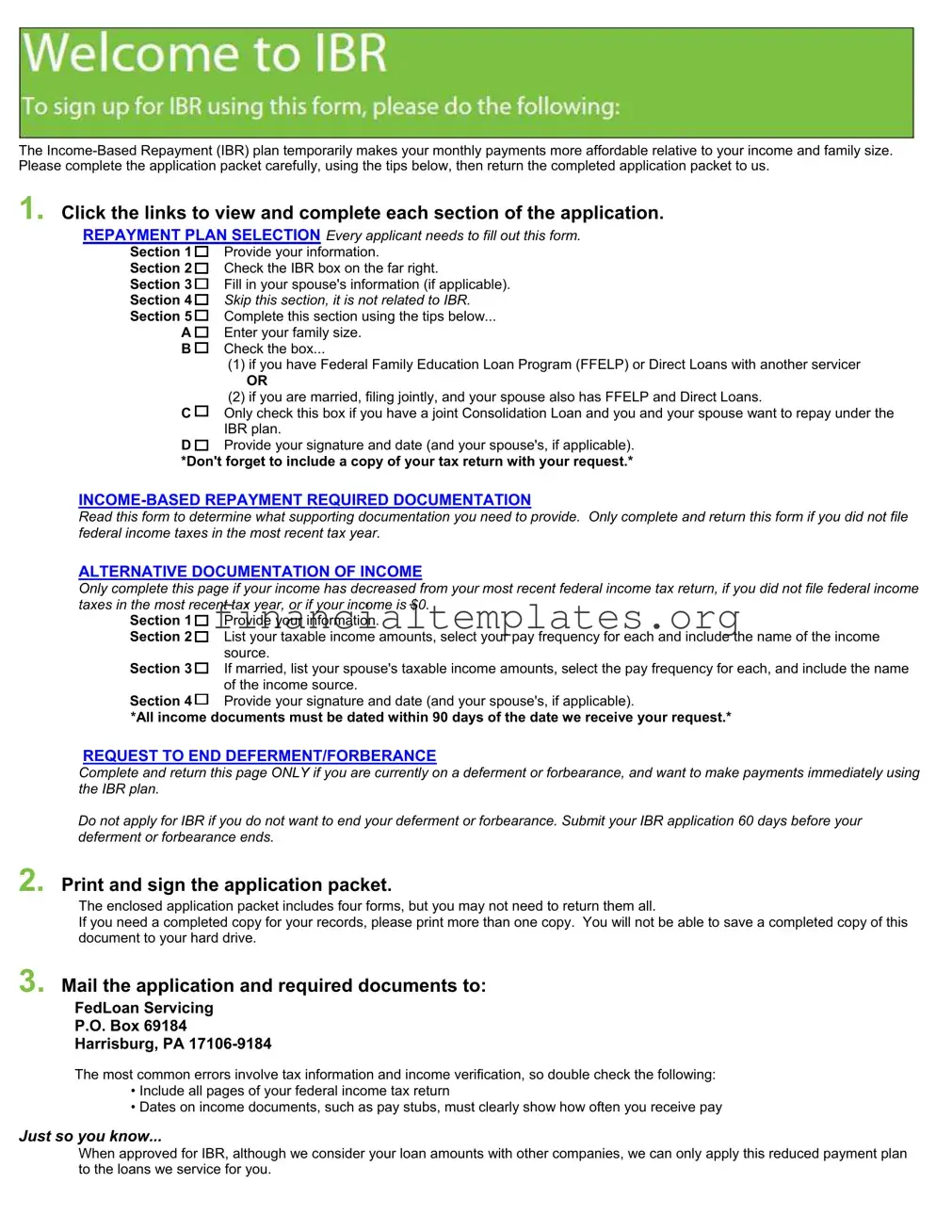

1. Click the links to view and complete each section of the application.

REPAYMENT PLAN SELECTION Every applicant needs to fill out this form.

Section 1 |

Provide your information. |

Section 2 |

Check the IBR box on the far right. |

Section 3 |

Fill in your spouse's information (if applicable). |

Section 4 |

Skip this section, it is not related to IBR. |

Section 5 |

Complete this section using the tips below... |

A |

Enter your family size. |

B |

Check the box... |

(1)if you have Federal Family Education Loan Program (FFELP) or Direct Loans with another servicer

OR

(2)if you are married, filing jointly, and your spouse also has FFELP and Direct Loans.

C |

Only check this box if you have a joint Consolidation Loan and you and your spouse want to repay under the |

|

IBR plan. |

D |

Provide your signature and date (and your spouse's, if applicable). |

*Don't forget to include a copy of your tax return with your request.*

Read this form to determine what supporting documentation you need to provide. Only complete and return this form if you did not file federal income taxes in the most recent tax year.

ALTERNATIVE DOCUMENTATION OF INCOME

Only complete this page if your income has decreased from your most recent federal income tax return, if you did not file federal income taxes in the most recent tax year, or if your income is $0.

Section 1 |

Provide your information. |

Section 2 |

List your taxable income amounts, select your pay frequency for each and include the name of the income |

|

source. |

Section 3 |

If married, list your spouse's taxable income amounts, select the pay frequency for each, and include the name |

|

of the income source. |

Section 4 |

Provide your signature and date (and your spouse's, if applicable). |

*All income documents must be dated within 90 days of the date we receive your request.*

REQUEST TO END DEFERMENT/FORBERANCE

Complete and return this page ONLY if you are currently on a deferment or forbearance, and want to make payments immediately using the IBR plan.

Do not apply for IBR if you do not want to end your deferment or forbearance. Submit your IBR application 60 days before your deferment or forbearance ends.

2. Print and sign the application packet.

The enclosed application packet includes four forms, but you may not need to return them all.

If you need a completed copy for your records, please print more than one copy. You will not be able to save a completed copy of this document to your hard drive.

3. Mail the application and required documents to:

FedLoan Servicing

P.O. Box 69184

Harrisburg, PA

The most common errors involve tax information and income verification, so double check the following:

•Include all pages of your federal income tax return

•Dates on income documents, such as pay stubs, must clearly show how often you receive pay

Just so you know...

When approved for IBR, although we consider your loan amounts with other companies, we can only apply this reduced payment plan to the loans we service for you.

REPAYMENT PLAN SELECTION

William D. Ford Federal Direct Loan Program

Records Code:

OMB No.

Form Approved

Exp. Date 11/30/2013

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on any accompanying documents is subject to penalties that may include fines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097.

Instructions

To understand your repayment options, carefully read this entire form, including the important notices in Section 7, and the enclosed information that describes the available repayment plans. After reviewing this information, complete the applicable sections below to select a repayment plan or to change your current repayment plan. Please print clearly using blue or black ink. If you need help completing this form, contact your servicer through one of the methods provided in Section 6 of this form. Return the completed form to the address shown in Section 6.

Section 1: Borrower Information – to be completed by ALL BORROWERS |

|

|

|

Borrower’s Last Name |

First Name |

Middle Initial |

Borrower’s Social Security Number: |

____________________________________________ |

_________________________ |

_________ |

|

|

|||

Section 2: Repayment Plan Selection – to be completed by ALL BORROWERS

•Place an “X” in the box in the chart below under the repayment plan that you wish to select for the types of loans that you owe. The enclosed information describes each of the repayment plans.

•You must choose the same repayment plan for all of your Direct Loans, unless you want to repay under the Income Contingent Repayment (ICR) Plan or

•In the chart below, the term “parent PLUS Loan” refers to a Direct PLUS Loan made under the William D. Ford Federal Direct Loan (Direct Loan) Program or a Federal PLUS Loan made under the Federal Family Education Loan (FFEL) Program that you borrowed to help pay for your dependent child’s undergraduate education. A “student PLUS Loan” is a Direct PLUS Loan or Federal PLUS Loan that you received to pay for your own graduate or professional education. A Direct PLUS Consolidation Loan is a Direct Consolidation Loan made before July 1, 2006 that repaid parent PLUS loans. No Direct PLUS Consolidation Loans have been made since July 1, 2006.

•To repay your loans under the IBR Plan, you must have a partial financial hardship (see Section 5).

•If you are beginning repayment of your loans for the first time and you do not select a repayment plan, or if you select the ICR Plan or IBR Plan but do not submit required additional forms and documentation, you will be placed on the Standard Repayment Plan.

•If you are requesting a change from another repayment plan to the ICR Plan or the IBR Plan and you do not submit required additional forms and documentation, you will remain on your current repayment plan.

•If you are requesting a change from your current repayment plan to a different plan, your servicer may grant you a forbearance for up to 60 days, if necessary, in order to collect and process documentation supporting your request (such as documentation required to process a request to repay under the ICR Plan or the IBR Plan). Unpaid interest that accrues during this maximum 60- day forbearance period will not be capitalized. (Capitalization is the addition of unpaid interest to the principal balance of your loan. This increases the principal balance and the total cost of your loan.)

•If you are delinquent in making payments under your current repayment plan at the time you request a change to a different plan, your servicer may grant you a forbearance to cover (1) any payments that are overdue at the time of your request, or (2) if you are requesting a change to the IBR Plan, any payments that would be overdue by the time your servicer determines whether you have a partial financial hardship (see Section 5), if it takes your servicer more than 60 days to make that determination. Unpaid interest that accrues during this forbearance period may be capitalized at the end of the forbearance period.

• |

Loan Types |

Standard |

Graduated |

Extended |

Income Contingent |

|

Direct Subsidized Loans |

|

|

|

|

|

|

• |

Direct Unsubsidized Loans |

|

|

|

|

|

• |

Student Direct PLUS Loans |

|

Fixed Payments |

Graduated Payments |

|

|

•Direct Consolidation Loans that did not repay any parent PLUS loans

•Direct Consolidation Loans made on or after July

1, 2006 that repaid one or more parent PLUS loans |

Fixed Payments |

Graduated Payments |

|

Not Available |

|

|

|

||

• Parent Direct PLUS Loans |

|

|

|

|

• Direct PLUS Consolidation Loans |

Fixed Payments |

Graduated Payments |

Not Available |

Not Available |

Section 3: Spouse Information – to be completed by SOME MARRIED BORROWERS

Complete this section only if you are married and are (1) selecting the ICR Plan (unless you are separated from your spouse), (2) selecting the IBR Plan and you and your spouse file a joint federal income tax return, and your spouse has loans that are eligible for repayment under the IBR Plan (see Section 5), or (3) selecting any repayment plan for a Direct Consolidation Loan held jointly by you and your spouse. If you are required to complete this section, your spouse must also sign this form.

Spouse’s Last Name |

First Name |

Middle Initial |

______________________________ |

________________________ |

_______ |

Spouse’s Social Security Number:

Spouse’s Date of Birth

Section 4: Additional ICR Information – to be completed by BORROWERS WHO SELECT THE INCOME CONTINGENT REPAYMENT PLAN

Complete this section only if you are selecting the ICR Plan.

Note: To repay under the ICR Plan, you must complete a consent form authorizing the Internal Revenue Service to disclose your adjusted gross income (AGI) and other tax return information, or you must provide other documentation of your AGI, such as a copy of your most recently filed federal income tax return, as specified by your servicer in documentation accompanying this form. In some cases, you may also be required to complete an ICR & IBR Plan Alternative Documentation of Income form. Your servicer will include the required additional forms with this Repayment Plan Selection form or will provide instructions for obtaining the forms. Complete and return the required form(s) or other required documentation along with this Repayment Plan Selection form.

Until your servicer receives the information needed to calculate your ICR Plan payment amount, your initial payment amount will be the full amount of interest that accumulates on your loan each month. If you are beginning repayment of your Direct Loan for the first time and you cannot afford the initial interest payment, you may request a forbearance until you are notified of your actual ICR payment. During a forbearance you are not required to make any payments of principal or interest, but interest continues to accumulate on your loan. Interest that you do not pay during this forbearance period will be capitalized at the end of the forbearance. To request a forbearance, contact your servicer.

A. Family Size. Enter your family size on the line below. Your family size includes you and your spouse. It includes your children if they get more than half their support from you. It includes other people only if (1) they now live with you, and (2) they now get more than half their support from you and they will continue to get this support from you. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, payment of college costs, etc. If your family size changes, notify your servicer in writing at the mailing address or the Web site address shown in Section 6.

Family Size: ________________

B. ICR Joint Repayment Option. If you and your spouse each have Direct Loans and both of you want to repay the loans under the ICR Plan, you may choose to repay your loans jointly (see ICR Plan description in the enclosed Repayment Plan Choices sheet). If you choose to repay jointly, place an “X” in the box below and have your spouse sign and date this form.

I wish to repay my loan(s) jointly with my spouse under the ICR Plan.

C. Certification. Read the certification statement below, then sign and date this form.

All of the information I provided on this form is true and complete to the best of my knowledge. If asked by an authorized official, I agree to provide proof of the information that I have provided on this form.

Borrower’s Signature |

|

Date |

|

Spouse’s Signature (if required; see Section 3) |

|

Date |

|

REVISED 04/2011

Section 5: Additional IBR Information – to be completed by BORROWERS WHO SELECT THE

Complete this section only if you are selecting the IBR Plan.

To initially qualify to repay your loans under the IBR Plan and to continue to make

Annual amount of payments due > 15% [AGI – (150% x applicable poverty guideline amount)]

The annual amount of payments due is calculated based on the greater of (1) the total amount owed on eligible loans at the time those loans initially entered repayment or (2) the total amount owed on eligible loans at the time you or, if applicable, your spouse requested the IBR Plan. The annual amount of payments due is calculated using a Standard Repayment Plan with

Section 7: Important Notices

PRIVACY ACT NOTICE

The Privacy Act of 1974 (5 U.S.C. 552a) requires that the following notice be provided to you:

The authority for collecting the requested information from and about you is §451 et seq. of the Higher Education Act (HEA) of 1965, as amended (20 U.S.C. 1087a et seq.) and the authorities for collecting and using your Social Security Number (SSN) are §484(a)(4) of the HEA (20 U.S.C. 1091(a)(4)) and 31 U.S.C. 7701(b). Participating in the William D. Ford Federal Direct Loan (Direct Loan) Program and giving us your SSN are voluntary, but you must provide the requested information, including your SSN, to participate.

The principal purposes for collecting the information on this form, including your SSN, are to verify your identity, to determine your eligibility to receive a loan or a benefit on a loan (such as a deferment, forbearance, discharge, or forgiveness) under the Direct Loan Program, to permit the servicing of your loan(s), and, if it becomes necessary, to locate you and to collect and report on your loan(s) if your loan(s) become delinquent or in default. We also use your SSN as an account identifier and to permit you to access your account information electronically.

The information in your file may be disclosed, on a

In the event of litigation, we may send records to the Department of Justice, a court, adjudicative body, counsel, party, or witness if the disclosure is relevant and necessary to the litigation. If this information, either alone or with other information, indicates a potential violation of law, we may send it to the appropriate authority for action. We may send information to members of Congress if you ask them to help you with federal student aid questions. In circumstances involving employment complaints, grievances, or disciplinary actions, we may disclose relevant records to adjudicate or investigate the issues. If provided for by a collective bargaining agreement, we may disclose records to a labor organization recognized under 5 U.S.C. Chapter 71. Disclosures may be made to our contractors for the purpose of performing any programmatic function that requires disclosure of records. Before making any such disclosure, we will require the contractor to maintain Privacy Act safeguards. Disclosures may also be made to qualified researchers under Privacy Act safeguards.

PAPERWORK REDUCTION NOTICE

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. The valid OMB control number for this information collection is

If you have questions about the status of your individual submission of this form, contact your servicer (see Section 6).

|

||

|

REQUIRED DOCUMENTATION |

|

|

NOTE: The attached Repayment Plan Selection form can be |

|

IBRD |

||

used to request IBR for both Direct and FFELP loans. |

Records Code:

Version Date: 06/01/11

NAME: ____________________________________________ |

ACCOUNT NUMBER: ______________________________ |

|

|

ELIGIBLE LOAN TYPES

Review the eligibility information below to determine if your loan type(s) is eligible for the IBR plan.

Parent PLUS loans, including Direct or FFELP parent PLUS Loans, Direct PLUS Consolidation Loans or Direct or FFELP Consolidation Loans that repaid parent PLUS loans, are not eligible for this repayment plan.

REQUIRED DOCUMENTATION

You must provide a signed Repayment Plan Selection Form AND a copy of your most recently filed federal income tax return*. Select IBR on the Selection Form, complete the appropriate section, and include all additional documentation based on your situation described below. Failure to provide any of the required documentation may result in denial of your request.

|

IF YOU… |

THEN PROVIDE… |

|

|

|

|

are currently employed, but your income has recently changed |

a completed, signed Alternative Documentation of Income |

|

|

form, and |

|

|

proof of your current income, such as a pay stub |

|

|

|

|

currently receive only untaxed income (SSI/Child Support) |

a completed, signed Alternative Documentation of Income |

|

|

form with the appropriate box checked in Section 2 |

|

|

|

|

currently have no taxable or untaxed income |

a completed, signed Alternative Documentation of Income |

|

|

form |

|

|

|

|

are currently in a period of deferment or forbearance and are |

a completed Request to End Deferment/Forbearance form |

|

requesting to enter the IBR plan before the deferment or |

|

|

forbearance period ends |

|

|

|

|

|

|

|

* CERTIFICATION SECTION FOR

Complete the signature section below ONLY if you were not required to file a federal income tax return for the most recent tax year.

I certify that I was not required to file a federal income tax return for the most recent tax year because I did not meet the IRS filing requirements.

Borrower’s Signature: ______________________________________________________ |

Date: ______________________ |

Records Code: |

||

Income Contingent Repayment Plan & |

|

|

|

OMB No. |

|

Alternative Documentation of Income |

|

|

|

Form Approved |

|

William D. Ford Federal Direct Loan Program |

|

Exp. Date 06/30/2012 |

Federal Direct Stafford/Ford Loans, Federal Direct Unsubsidized Stafford/Ford Loans, |

|

|

Federal Direct Subsidized Consolidation Loans, Federal Direct Unsubsidized Consolidation Loans

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form shall be subject to penalties which may include fines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097.

Section 1: Identifying Information

Before completing this form, carefully read the instructions in Section 5.

All borrowers must provide the Borrower Information below.

Borrower Information:

Borrower’s Name (please print clearly):

________________________________________________

Last Name First NameMiddle Initial

Borrower’s Social Security Number:

If you are married, you must also provide the Spouse Information below if

(1)you are repaying under the ICR Plan, or (2) you are repaying under the IBR Plan and you and your spouse file a joint federal tax return.

Spouse Information:

Your Spouse’s Name (please print clearly):

________________________________________________________

Last Name First NameMiddle Initial

Your Spouse’s Social Security Number:

Section 2: Borrower’s Income Information – to be completed by ALL BORROWERS

All borrowers must complete this section.

You must list all taxable income you are currently receiving (i.e., income from employment, unemployment income, dividend income, interest income, tips, alimony). Include the amount of money received, how often you receive this money, and your employer (if any) or the source of your income if you are not employed. You must attach supporting documentation for all income reported in this section (e.g., pay stubs, letters from your employer stating your income, interest or bank statements, dividend statements, canceled checks, or, when these forms of documentation are unavailable, a signed statement explaining your income source(s) and giving the addresses of these sources). Copies are acceptable, but all supporting documentation must be no more than 90 days old. If you have more than two sources of income, provide the information requested in this section on a separate piece of paper and mail it with this form. Do not report untaxed income such as Supplemental Security Income, child support, or federal or state public assistance. If your income or the income of your spouse changes significantly after your submission of this form, you must notify your servicer of this change (see contact information in Section 5).

Amount of |

|

Frequency of Payment (Please check the appropriate box.) |

|

Employer or Source of Income |

|||

Income |

Weekly |

Monthly |

Yearly |

||||

|

|||||||

$

$

Check this box if you do not have any taxable income and receive only untaxed income such as Supplemental Security Income, child support, or federal or state public assistance.

Section 3: Spouse’s Income Information – to be completed by SOME MARRIED BORROWERS

If you are married, you must provide your spouse’s income information if:

1.You are repaying under the ICR Plan, or

2.You are repaying under the IBR Plan and you and your spouse file a joint federal tax return.

If you are required to complete this section, you must provide the same information and supporting documentation for your spouse’s income that is required for your own income, as explained above in Section 2.

Amount of |

|

Frequency of Payment (Please check the appropriate box.) |

|

Employer or Source of Income |

|||

Income |

Weekly |

Monthly |

Yearly |

||||

|

|||||||

$

$

Check this box if your spouse does not have any taxable income and receives only untaxed income such as Supplemental Security Income, child support, or federal or state public assistance.

Check this box if your spouse does not have any taxable income and receives only untaxed income such as Supplemental Security Income, child support, or federal or state public assistance.

Section 4: Certification and Signature

All borrowers must complete this section. If you are married, your spouse must sign and date below only if (1) you are repaying under the ICR Plan, or (2) you are repaying under the IBR Plan and you and your spouse file a joint federal tax return.

Certification: I certify that all of the information reported in Section 2 and, if applicable, Section 3 is true and complete to the best of my knowledge. I agree to provide to the U.S. Department of Education (the Department) on an annual basis (or as required by the Department) alternative documentation of my income for the purpose of determining my appropriate repayment amount under the ICR Plan or IBR Plan. I understand that (1) if I do not provide this information the Department will base my ICR or IBR amount on my AGI, as reported by the IRS, or, in some instances, I will not be allowed to repay my loan(s) under the ICR or IBR Plan; (2) the Department may request my income information from the IRS even if alternative documentation of my income is accepted; and (3) if I am married, my spouse’s income information, documentation, and signature are also required if I am repaying under the ICR Plan, or if I am repaying under the IBR Plan and my spouse and I file a joint federal tax return.

Borrower’s Signature |

Date of Borrower’s Signature |

Spouse’s Signature |

Date of Spouse’s Signature |

Section 5: Instructions and Where to Send the Completed Form

INSTRUCTIONS:

YOU ARE REQUIRED to complete this form if you are repaying your Direct Loans under the Income Contingent Repayment (ICR) or the

•

•

•

You are in your first year of repayment;

You are in your second year of repayment and have been notified that alternative documentation of your income is required; or

You have been notified that the Internal Revenue Service (IRS) is unable to provide the U.S. Department of Education (the Department) with your Adjusted Gross Income (AGI) or that of your spouse (if applicable).

YOU MAY complete this form if:

•You are repaying your Direct Loans under the ICR Plan and your AGI (and your spouse’s AGI, if you are married), as reported on your most recently filed federal tax return, does not reasonably reflect your current income (e.g., due to circumstances such as loss or change in employment by you or your spouse).

•You are repaying your Direct Loans under the IBR Plan and your AGI (and your spouse’s AGI, if you and your spouse file a joint federal tax return), as reported on your most recently filed federal tax return, does not reasonably reflect your current income (e.g., due to circumstances such as loss or change in employment by you or your spouse).

In cases where alternative documentation of your income is used, the amount of your monthly payment under the ICR or IBR Plan is based on the current income information you and your spouse (if applicable) provide and is reevaluated annually. Your monthly payment may be adjusted more frequently than annually if you notify your servicer that your AGI (or your spouse’s AGI, if you file a joint federal tax return) has changed significantly since your most recent submission of this form and you provide supporting documentation showing this change. To submit alternative documentation of your income, you must attach the required documentation, complete and sign this form, and return it to the address below. If you are married, your spouse must also complete and sign the applicable sections of this form and submit the required documentation if (1) you are repaying your loans under the ICR Plan, or (2) you are repaying your loans under the IBR Plan and you and your spouse file a joint federal tax return. If you need assistance, please call

.

Return this form to:

U.S. Department of Education

FedLoan Servicing

P.O. Box 69184

Harrisburg, PA

If you need assistance completing this form, call

Section 6: Important Notices

PRIVACY ACT NOTICE

The Privacy Act of 1974 (5 U.S.C. 552a) requires that the following notice be provided to you:

The authority for collecting the requested information from and about you is §451 et seq. of the Higher Education Act (HEA) of 1965, as amended (20 U.S.C. 1087a et seq.) and the authorities for collecting and using your Social Security Number (SSN) are §484(a)(4) of the HEA (20 U.S.C. 1091(a)(4)) and 31 U.S.C. 7701(b). Participating in the William D. Ford Federal Direct Loan (Direct Loan) Program and giving us your SSN are voluntary, but you must provide the requested information, including your SSN, to participate.

The principal purposes for collecting the information on this form, including your SSN, are to verify your identity, to determine your eligibility to receive a loan or a benefit on a loan (such as a deferment, forbearance, discharge, or forgiveness) under the Direct Loan Program, to permit the servicing of your loan(s), and, if it becomes necessary, to locate you and to collect and report on your loan(s) if your loan(s) become delinquent or in default. We also use your SSN as an account identifier and to permit you to access your account information electronically.

The information in your file may be disclosed, on a

In the event of litigation, we may send records to the Department of Justice, a court, adjudicative body, counsel, party, or witness if the disclosure is relevant and necessary to the litigation. If this information, either alone or with other information, indicates a potential violation of law, we may send it to the appropriate authority for action. We may send information to members of Congress if you ask them to help you with federal student aid questions. In circumstances involving employment complaints, grievances, or disciplinary actions, we may disclose relevant records to adjudicate or investigate the issues. If provided for by a collective bargaining agreement, we may disclose records to a labor organization recognized under 5 U.S.C. Chapter 71. Disclosures may be made to our contractors for the purpose of performing any programmatic function that requires disclosure of records. Before making any such disclosure, we will require the contractor to maintain Privacy Act safeguards. Disclosures may also be made to qualified researchers under Privacy Act safeguards.

Paperwork Reduction Notice. According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a currently valid OMB control number. The valid OMB control number for this information collection is

If you have questions about the status of your application, contact us at the following address:

U.S. Department of Education

FedLoan Servicing

P.O. Box 69184

Harrisburg, PA

Records Code:

Version Date: 06/01/10

RDF

BORROWER NAME: ____________________________________________

ACCOUNT NUMBER: ________________________________

_____________________________________________________________________________________________________________

I am requesting to have my deferment/forbearance terminated on my eligible loan(s) for the purpose of allowing FedLoan Servicing to process my request for IBR/ICR.

I understand that I am only requesting the termination of my current deferment/forbearance if I qualify for the requested repayment plan. I also understand that if my current deferment / forbearance is ended, any unpaid accrued interest will be capitalized (added to the balance) and my loan(s) will be placed into repayment.

__________________________________________ |

__________________ |

Borrower’s Signature |

Date |

Document Specifics

| Fact Name | Description |

|---|---|

| Plan Purpose | The Income-Based Repayment (IBR) plan is designed to lower monthly student loan payments relative to the borrower's income and family size. |

| Application Process | Applicants must complete the entire application packet and return it, including any required documentation. |

| Repayment Plan Selection | All applicants must fill out the Repayment Plan Selection form, indicating their choice of the IBR plan. |

| Required Documentation | Documentation necessary includes a copy of the most recent federal income tax return and possibly an Alternative Documentation of Income form depending on the borrower's income situation. |

| Eligible Loans | The IBR plan covers most federal student loans except for parent PLUS loans, loans in default, and certain consolidation loans. |

| Importance of Tax Information | Accuracy of tax information and income verification is essential, requiring careful attention to documentation details. |

| Penalties for False Statements | Providing false information on the application or accompanying documents may result in fines, imprisonment, or both under U.S. law. |

Guide to Writing Income Based Repayment

The process of applying for an Income-Based Repayment (IBR) plan involves several documents and careful attention to detail to ensure that all aspects of your financial situation are accurately represented. This plan offers the possibility to lower your monthly student loan payments based on your income and family size. Following the steps below will guide you through completing the application packet. Remember, after filling out the application, include the required documentation to avoid delays in processing. Here are the steps you’ll need to take:

- Repayment Plan Selection: Begin by reviewing the entire application form. Make sure you understand each section and how it relates to your personal circumstances.

- Section 1 - Provide Your Information: Enter your full name, social security number, and contact details as requested.

- Section 2 - Check the IBR Box: Indicate that you are applying for the IBR plan by checking the corresponding box.

- Section 3 - Spouse’s Information: If you are married, fill out this section with your spouse's information. This is necessary if you file taxes jointly and your spouse also has eligible loans.

- Section 4 - Skip: This section does not apply to the IBR application, so you can move on without filling it in.

- Section 5 - Complete With Additional Information:

- Enter your family size.

- Check the appropriate box if you have eligible FFELP or Direct Loans with another servicer, are married filing jointly with a spouse who also has such loans, or if you both wish to repay under the IBR plan via a joint Consolidation Loan.

- Sign and date the form, ensuring your spouse does as well if applicable.

- Include a copy of your tax return: Attach all pages of your most recent federal income tax return to your application.

- Income-Based Repayment Required Documentation: Complete this form if you did not file taxes in the most recent year, if your income has significantly changed, or if you currently have no income.

- Alternative Documentation of Income: Fill out this section by providing details about your (and your spouse’s, if applicable) taxable income and frequency of pay, including the source of this income.

- Request to End Deferment/Forbearance: Only complete this section if you are currently in deferment or forbearance but wish to start making payments under the IBR plan.

- Print and sign the application packet: Ensure all information is correct and complete before signing. If you need a copy for your records, print an extra before mailing it.

- Mail the completed application and documents: Send your application packet to the provided address of FedLoan Servicing.

Accuracy in completing these forms and including all necessary documentation, like your tax return and any required proof of current income, is crucial. This ensures your application for the IBR plan will be processed smoothly and efficiently. If approved, remember that this plan may adjust your monthly payments, making them more manageable based on your current financial situation.

Understanding Income Based Repayment

-

What is the Income-Based Repayment (IBR) Plan?

The IBR plan is designed to lower your monthly student loan payments in accordance with your income and family size. It aims to make your loan repayment more manageable by adjusting payments based on your financial situation.

-

How do I apply for the IBR Plan?

To apply, complete the Repayment Plan Selection form provided in your application packet. Ensure you select the IBR option, fill out all required sections including personal, spouse (if applicable), and income information. Attach a copy of your most recent tax return for income verification.

-

What if my income has changed recently or I haven't filed a tax return?

If your income has significantly decreased since your last tax return, or if you did not file a tax return in the most recent tax year, you will need to submit Alternative Documentation of Income. This involves completing a form detailing your current income levels and providing corresponding proof, such as recent pay stubs.

-

Are all loans eligible for IBR?

Not all loan types qualify for IBR. Eligible loans include Direct Subsidized and Unsubsidized Loans, Direct Consolidation Loans that did not repay any parent PLUS loans, and more. Loans that are not eligible include parent PLUS loans, loans in default, and Direct PLUS Loans made to a parent borrower, among others.

-

What do I need to include with my IBR application?

- A completed Repayment Plan Selection form with the IBR option selected.

- Your most recent tax return, unless your income has changed or you did not file.

- Alternative Documentation of Income form and proof of income, if applicable.

- If applying to exit deferment or forbearance early, a completed request form is required.

-

How often do I need to recertify my income and family size for IBR?

You must recertify your income and family size annually to stay on the IBR plan. Your loan servicer will contact you with instructions on how to recertify. Failure to recertify could result in your payment amount reverting to the amount you would pay under the Standard Repayment Plan.

-

What happens if I no longer qualify for IBR due to an income increase?

If your income increases to a point where you no longer demonstrate a partial financial hardship, your payments will no longer be based on your income. However, your payments will be capped at what you would have paid under the standard 10-year repayment plan, even if your recalculated IBR payment is higher.

Common mistakes

Not marking the IBR selection box correctly in the Repayment Plan Selection section can lead to the application being processed under the wrong repayment plan. It's essential to place an "X" in the IBR box to ensure the application is considered for income-based repayment.

Omitting spouse's information when applicable is another common mistake. If married and filing taxes jointly, or if both individuals have qualifying loans for the IBR plan, failing to include the spouse’s information may result in the incorrect calculation of the monthly payment amount. Both the applicant and the spouse's income are taken into consideration for determining the payment under IBR, making accurate and complete information critical.

Skipping the family size declaration or inaccurately reporting family size can have significant implications. The family size is a major determinant in calculating the monthly payment amount under IBR, as it impacts the poverty guideline calculation used in determining the payment. Therefore, accurately entering the number of family members is crucial.

Forgetting to sign and date the form can lead to processing delays or outright denial. The personal declaration and consent are necessary steps in the application process, requiring both the borrower's and the spouse's signatures when applicable. This mistake can be easily avoided by double-checking the form before submission.

Not including required documents, specifically the most recent federal income tax return or alternative documentation of income, can hinder the processing of the application. These documents are vital for verifying income and family size, both of which are essential in calculating the appropriate monthly repayment amount under the IBR plan. Ensuring all necessary paperwork is included with the application packet is fundamental for a smooth processing experience.

Documents used along the form

When navigating the waters of managing student loan debt, understanding and compiling the necessary documents for an Income-Based Repayment (IBR) plan can be quite the odyssey. It’s not just about the IBR application itself; several other documents are often part of this journey, each playing a unique role in the process. Let’s explore these documents that frequently accompany an IBR application, shedding light on their purposes and why they are indispensable.

- Federal Income Tax Return: This is a critical document for the IBR application process. It provides proof of income, allowing the loan servicer to calculate your monthly payment based on your current earnings and family size.

- Alternative Documentation of Income: For those whose recent income may not accurately be reflected through a tax return – whether due to a change in employment, a decrease in income, or other reasons – this form serves as a way to document current earnings and ensure your IBR payment reflects your present financial situation.

- Request to End Deferment/Forbearance: If you’re looking to transition from a period of deferment or forbearance to making payments under the IBR plan, this form signals your intent to end that period of paused payments, allowing you to start repaying your loans based on your income.

- Employment Certification for Public Service Loan Forgiveness (PSLF): For borrowers working in public service looking to qualify for PSLF, this form verifies your employment in a qualifying position. By pairing IBR with PSLF, borrowers can have their remaining loan balance forgiven after 10 years of qualifying payments.

- Income-Driven Repayment Plan Annual Recertification: To remain on the IBR plan, borrowers must annually recertify their income and family size. This ensures that your payment continues to match your financial reality, adjusting as your circumstances change.

- Consolidation Loan Application: For borrowers with multiple federal student loans, consolidating them into a single loan can simplify repayment. When opting for an IBR plan, consolidation can be a strategic move to streamline your loans, potentially leading to a lower monthly payment under IBR.

Understanding each of these documents is key to navigating the IBR plan application process smoothly. Whether it’s providing proof of income, making changes to your repayment plan, or aiming for loan forgiveness, each form plays a vital role in helping borrowers manage their student loan debt more effectively. Remember, the goal of the IBR plan is affordability and sustainability, enabling borrowers to make their student loan payments without compromising their financial well-being.

Similar forms

The Federal Application For Student Aid (FAFSA) form shares similarities with the Income-Based Repayment (IBR) form in that both are integral for students seeking financial assistance for education. The FAFSA form is the first step in accessing federal financial aid, while the IBR form comes into play when managing loan repayment based on income after graduation. Both forms require detailed personal and financial information to calculate eligibility for either aid or reduced repayment plans, emphasizing the importance of accurate and comprehensive income documentation.

The Employment Verification form, similar to sections of the IBR form that require proof of income, serves to validate an individual's employment status and income level. This verification process is crucial in both contexts for determining financial eligibility—whether for loan repayment adjustments under the IBR plan or establishing qualification for various employment benefits or credits. The submission of accurate employment and income information ensures that calculations related to payments or benefits are correct.

Income Tax Return forms are directly referenced within the IBR form as a required piece of documentation for individuals who have filed taxes in the most recent tax year. Both sets of documents necessitate a thorough accounting of an individual’s financial picture. Income Tax Returns serve as a comprehensive snapshot of an individual's financial status, mirroring how the IBR form utilizes this information to determine a borrower's eligibility for reduced monthly loan payments based on their income and family size.

The Alternative Documentation of Income, a specific part of the IBR application, shares similarities with various financial forms like the Proof of Income Statement or 1099 forms. They all aim to substantiate an individual’s earnings through documentation other than traditional wages, such as freelance income, benefits, or other sources. This is especially relevant when recent income levels or employment status do not fully capture one’s current financial scenario, thereby affecting their repayment capabilities or eligibility for certain financial programs.

The Deferment and Forbearance Request forms for student loans bear resemblance to parts of the IBR form that deal with exiting deferment or forbearance to enter an income-based repayment plan. These forms all address changes to a borrower’s repayment strategy due to shifts in their financial situation or income. Each form requires the borrower to provide detailed information that supports the need for a modification to their repayment terms, whether to reduce monthly payments, pause them, or temporarily halt accrual of interest.

The Loan Consolidation Application has parallels with the IBR application process in the sense that both deal with restructuring existing loan terms to potentially alleviate financial strain. Where consolidation might combine multiple loans into a single loan with new terms, the IBR plan adjusts monthly payment amounts based on income and family size. Both processes require borrowers to provide detailed financial information and consider the implications on their long-term financial commitments.

Last, the Public Service Loan Forgiveness (PSLF) application, while catering to a specific subset of borrowers, shares a core similarity with the IBR form through its focus on offering relief based on certain criteria, such as employment in public service and income level. Each form assesses the borrower's employment and income information to determine eligibility for reduced payments or loan forgiveness, highlighting the importance of carefully documented financial and employment histories in seeking loan relief or forgiveness.

Dos and Don'ts

When you are applying for the Income-Based Repayment (IBR) plan, you are navigating a process that is designed to ease your monthly student loan payments based on your income and family size. To ensure a smooth application process, here are some important dos and don'ts:

- Do click the links to view and complete each section of the application carefully.

- Do check the IBR box to indicate your selected repayment plan.

- Do include your family size accurately, as it plays a critical role in calculating your payment.

- Do provide your signature and the date (and your spouse's, if applicable) to verify the information.

- Do include all pages of your federal income tax return, as failing to do so is a common error.

- Don't leave out your spouse's information if you are married, filing jointly, and if your spouse also has qualifying loans.

- Don't forget to check the box indicating whether you have loans with another servicer or if you are considering joint consolidation loan repayment options.

- Don't submit the form without ensuring all income documents are dated within 90 days of the date the application is received.

- Don't ignore the request to provide alternative documentation of income if your income has decreased since your last federal income tax return or if you did not file taxes in the most recent tax year.

Following these guidelines will help avoid delays or issues with your application. Remember, the IBR plan is designed to be flexible and accommodating to your financial situation, so providing accurate and complete information is key to receiving the full benefits of the program.

Misconceptions

There are several misunderstandings about the Income-Based Repayment (IBR) form and process that can lead to confusion for applicants. Addressing these misconceptions can help ensure that borrowers are better informed and can make decisions that align with their financial situations.

One common misconception is that the IBR plan is automatically available to all borrowers with federal student loans. In reality, eligibility for the IBR plan is based on the borrower's specific loan type, income, and family size. Not all federal loans qualify, and the applicant must demonstrate a partial financial hardship to be eligible.

Many believe that applying for the IBR plan is a complex and lengthy process. However, while the application does require accurate and detailed information, it is designed to be straightforward. Applicants need to carefully fill out the Repayment Plan Selection form and provide the required documentation, including a recent tax return or alternative documentation of income if their income has changed significantly since the last tax filing.

Another misunderstanding is that once under the IBR plan, the payment amount is fixed for the life of the loan. This is not the case; the payment amount under the IBR plan can change annually based on changes in the borrower's income and family size. Borrowers must recertify their income and family size each year to adjust the payment amount accordingly.

Finally, some borrowers think that submitting an IBR application will automatically defer or forbear their loan payments until the application is processed. The truth is, borrowers must continue making their current loan payments until their IBR application is approved and their loan servicer notifies them of their new reduced payment amount. Failing to do so could result in late payments or delinquency.

Understanding these misconceptions about the IBR form and process can help borrowers manage their federal student loans more effectively and avoid potential pitfalls.

Key takeaways

Filling out the Income-Based Repayment (IBR) form can significantly reduce monthly student loan payments for those who qualify. Here are seven key takeaways to ensure the process is smooth and successful:

- Understand Your Eligibility: The IBR plan is available for most federal student loans, including Direct Subsidized and Unsubsidized Loans, and Federal Family Education Loan Program loans. However, loans such as Direct or FFELP Parent PLUS Loans and loans in default are not eligible.

- Accurately Determine Family Size: Your family size affects your payment calculation under the IBR plan. Include yourself, your spouse, your children if they receive more than half of their support from you, and anyone else who lives with you and receives more than half of their support from you.

- Provide Complete and Accurate Income Information: Your monthly payment is based on your income and family size. Use the most recent tax return for income verification. If your income has changed significantly since then, or if you didn't file a tax return, you may need to submit alternative documentation of your income.

- Check Required Boxes Correctly: Ensure you accurately complete the IBR section of the application, including checking the box if you have loans with another servicer or if you are married and filing jointly and your spouse also has federal student loans.

- Include All Necessary Documentation: Failing to provide required documents like your federal income tax return or alternative documentation of income if you haven't filed taxes could delay processing your application or lead to a denial.

- Submit the Form in a Timely Manner: If you're currently in deferment or forbearance but wish to switch to IBR, submit your form 60 days before your current status ends. This ensures a smooth transition to the IBR plan without gaps in your payment schedule.

- Re-certification is Annual: To remain on the IBR plan, you must re-certify your income and family size each year. Failing to do so can result in increased payments, as the plan defaults back to the standard repayment plan amount.

Correctly completing and submitting the IBR application can provide significant financial relief for borrowers struggling with student loan payments. Paying close attention to the details and promptly updating your income and family size annually are crucial steps to take full advantage of the IBR plan.

Popular PDF Documents

Transcript Id Me - Assists executors in understanding the estate and generation-skipping transfer tax obligations for nonresident non-citizens.

What Is Form 8453 Used for - The IRS 8453 form is a document used for electronic filing of federal tax returns, acting as a signature authorization.