Get City Of St Louis Tax Form

Navigating the intricate landscape of taxation within the cityscape of St. Louis demands a thorough understanding of the City of St. Louis Earnings and Payroll Tax, encapsulated meticulously in Form E-234. This essential document, crafted by the Office of the Collector of Revenue, serves as the keystone for both residents and non-residents engaging in an array of professional and business endeavors within St. Louis's boundaries. It not only mandates the annual financial disclosure from entities ranging from individuals and partnerships to corporations but also delineates the spectrum of income, including 1099-MISC, that requires reporting. Detailed instructions accompany stipulations regarding the filing location at the Earnings Tax Division, deadlines, penalties for tardiness, and avenues for requesting extensions, ensuring that taxpayers are well-equipped to fulfill their obligations. The form intricately details the process for computing taxable net profit, allowances and disallowances for business expense deductions, and the specifics of apportionment for businesses operating both within and outside the city limits. Moreover, it emphasizes compliance, with penalties for incomplete returns, and highlights the requirement for substantiating allocations or deductions through comprehensive documentation. The City of St. Louis makes it clear that while the federal extension might offer a reprieve on the national stage, it does not exempt taxpayers from adhering to city-specific deadlines, underscoring the city's commitment to ensuring that every entity contributes its fair share to the municipal coffers.

City Of St Louis Tax Example

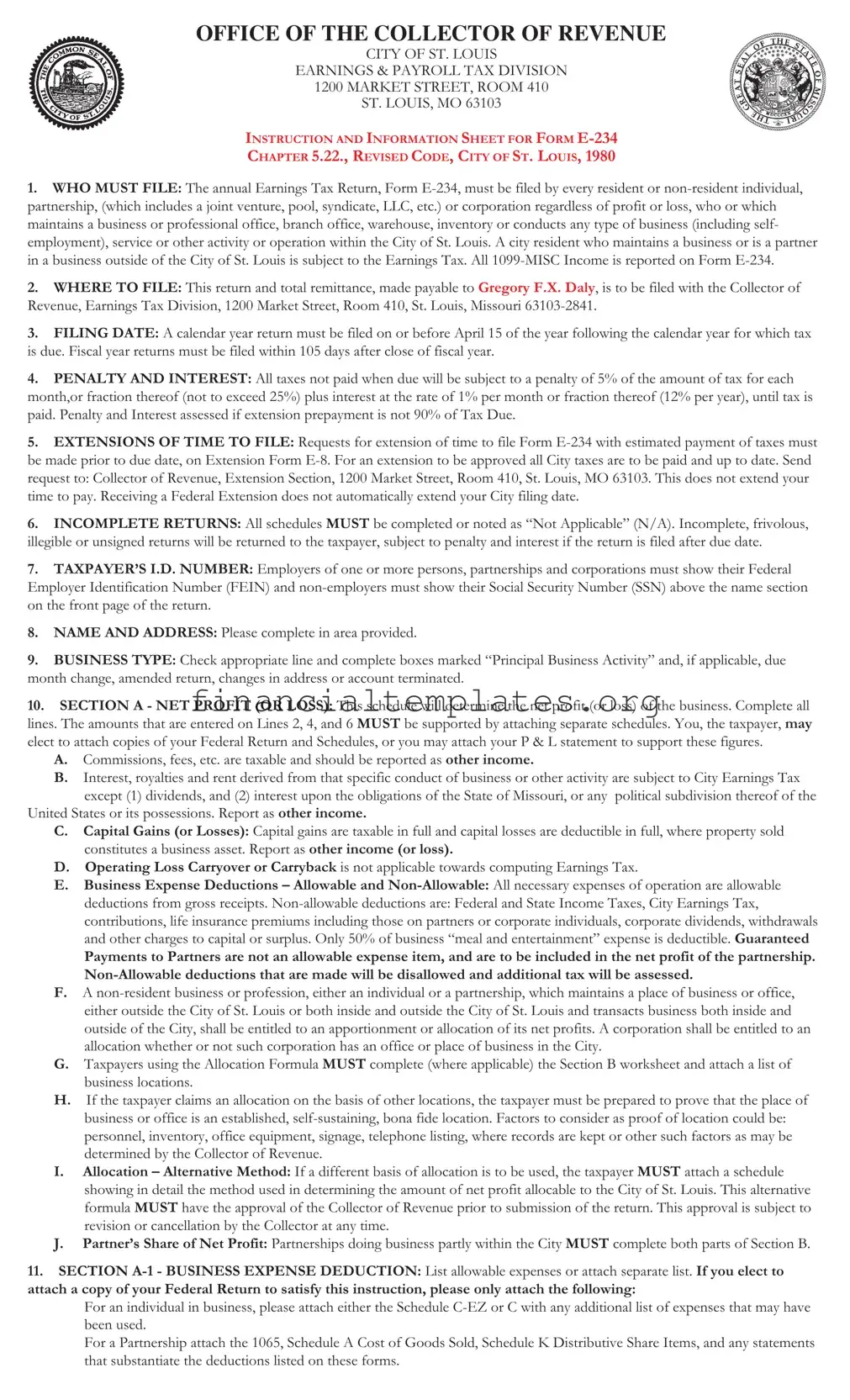

OFFICE OF THE COLLECTOR OF REVENUE

CITY OF ST. LOUIS

EARNINGS & PAYROLL TAX DIVISION

1200 MARKET STREET, ROOM 410

ST. LOUIS, MO 63103

INSTRUCTION AND INFORMATION SHEET FOR FORM

CHAPTER 5.22., REVISED CODE, CITY OF ST. LOUIS, 1980

1.WHO MUST FILE: The annual Earnings Tax Return, Form

2.WHERE TO FILE: This return and total remittance, made payable to Gregory F.X. Daly, is to be filed with the Collector of Revenue, Earnings Tax Division, 1200 Market Street, Room 410, St. Louis, Missouri

3.FILING DATE: A calendar year return must be filed on or before April 15 of the year following the calendar year for which tax is due. Fiscal year returns must be filed within 105 days after close of fiscal year.

4.PENALTY AND INTEREST: All taxes not paid when due will be subject to a penalty of 5% of the amount of tax for each month,or fraction thereof (not to exceed 25%) plus interest at the rate of 1% per month or fraction thereof (12% per year), until tax is paid. Penalty and Interest assessed if extension prepayment is not 90% of Tax Due.

5.EXTENSIONS OF TIME TO FILE: Requests for extension of time to file Form

6.INCOMPLETE RETURNS: All schedules MUST be completed or noted as “Not Applicable” (N/A). Incomplete, frivolous, illegible or unsigned returns will be returned to the taxpayer, subject to penalty and interest if the return is filed after due date.

7.TAXPAYER’S I.D. NUMBER: Employers of one or more persons, partnerships and corporations must show their Federal Employer Identification Number (FEIN) and

8.NAME AND ADDRESS: Please complete in area provided.

9.BUSINESS TYPE: Check appropriate line and complete boxes marked “Principal Business Activity” and, if applicable, due month change, amended return, changes in address or account terminated.

10.SECTION A - NET PROFIT (OR LOSS): This schedule will determine the net profit (or loss) of the business. Complete all lines. The amounts that are entered on Lines 2, 4, and 6 MUST be supported by attaching separate schedules. You, the taxpayer, may elect to attach copies of your Federal Return and Schedules, or you may attach your P & L statement to support these figures.

A.Commissions, fees, etc. are taxable and should be reported as other income.

B.Interest, royalties and rent derived from that specific conduct of business or other activity are subject to City Earnings Tax except (1) dividends, and (2) interest upon the obligations of the State of Missouri, or any political subdivision thereof of the

United States or its possessions. Report as other income.

C.Capital Gains (or Losses): Capital gains are taxable in full and capital losses are deductible in full, where property sold constitutes a business asset. Report as other income (or loss).

D.Operating Loss Carryover or Carryback is not applicable towards computing Earnings Tax.

E.Business Expense Deductions – Allowable and

deductions from gross receipts.

Payments to Partners are not an allowable expense item, and are to be included in the net profit of the partnership.

F.A

G.Taxpayers using the Allocation Formula MUST complete (where applicable) the Section B worksheet and attach a list of business locations.

H.If the taxpayer claims an allocation on the basis of other locations, the taxpayer must be prepared to prove that the place of business or office is an established,

I.Allocation – Alternative Method: If a different basis of allocation is to be used, the taxpayer MUST attach a schedule showing in detail the method used in determining the amount of net profit allocable to the City of St. Louis. This alternative formula MUST have the approval of the Collector of Revenue prior to submission of the return. This approval is subject to revision or cancellation by the Collector at any time.

J.Partner’s Share of Net Profit: Partnerships doing business partly within the City MUST complete both parts of Section B.

11.SECTION

For an individual in business, please attach either the Schedule

For a Partnership attach the 1065, Schedule A Cost of Goods Sold, Schedule K Distributive Share Items, and any statements that substantiate the deductions listed on these forms.

For a Corporation attach the first page of either the 1120, 1120A, 1120S, whichever is appropriate. Schedule K Distributive Share Items for 1120S, Schedule A Cost of Goods Sold, and any statements that substantiate the deductions of these forms. Also include Schedule L,

For a LLC or LLP please attach the appropriate information based on the Federal return you file. We do not need copies of the individual shareholders

12.SECTION

In Column A - List name, address, city, state and zip code, Column B - The FEIN or SSN, Column C - Total amount paid during the year. Column D - Show the amount or a percent (%) of Column C that you estimate was earned in the City. If additional space is needed, please attach separate sheet. Failure to complete this section may result in the disallowance of these deductions. If you had no expenses that meet these criteria, print N/A in Section

13.RESIDENT BUSINESS TAXPAYER: A resident business of the City of St. Louis, individual proprietor or partnership, is subject to the City Earnings Tax on the entire net profit, regardless of where earned and cannot allocate its net profit.

14.SOLE STORE/OFFICE IS IN ST. LOUIS: A

15.SECTION B WORKSHEET - BUSINESS ALLOCATION OF TAXABLE NET PROFIT (PAGE 2):

A.A

B.Taxpayers using the Allocation Formula MUST complete (where applicable) the Section B worksheet and attach a list of business locations. The Section B worksheet consists of three factors; 1. Average Value of Real and Tangible Personal Property, including inventory (The value of real and tangible personal property is to be based on Original Cost. If the taxpayer is renting the tangible property used, then this value is Rent times 8). 2. Gross receipts; and 3. Wages and Salaries (Except Officers).

C.If the taxpayer claims an allocation on the basis of other locations, the taxpayer must be prepared to prove that the place of business or office is an established,

D.Allocation – Alternative Method: If a different basis of allocation is to be used, the taxpayer must attach a schedule showing in detail the method used in determining the amount of net profit allocable to the City of St. Louis. This alternative formula MUST have the approval of the Collector of Revenue prior to submission of the return. This approval is subject to revision or cancellation by the Collector at any time.

E.Partner’s Share of Net Profit: Partnerships doing business partly within the City MUST complete both parts of Section B.

16.SECTION C - COMPUTATION OF TAX:

A.Enter on Line 9 the taxable net profit, which is either Line 7, Section A, Line 8B, Section B or total of Column 3, Partner’s Share of Net Profit, on Section

B.Earnings Tax due is 1% of Line 9, enter on Line 10. No tax is due if amount is less than $1.00.

C.Payroll Expense Tax credit is an amount equal to 20% of the Payroll Expense Tax actually paid, but is not to exceed 25% of the earnings tax due. Calculate as provided in Section

D.Line 12 is net earnings tax due (Line 10 minus Line 11).

E.Line 13, enter amount paid with Extension or estimated payments.

F.Line 14,

G.Line 15 (penalty) and Line 16 (interest) should be completed, if applicable. See Instruction #4.

H.Line 17 is the total amount due (Line 12 or 14, plus Line 15 & 16, if applicable). Make remittance payable to:

Gregory F.X. Daly, Collector of Revenue

I.No refund due if under $1.00. Refunds are only valid if claimed within one year of payment. Refunds may be credited to the next year taxes by writing “Please credit refund to next year’s taxes” on Line 17, Form

J.Rounding is required on your tax return. Zeros have been placed in the cents column on your return. For 1 cent through 49 cents, round down to the previous whole dollar amount. For 50 cents through 99 cents, round up to the next whole dollar amount. Example: Round $2.49 to $2.00. Round $2.50 to $3.00.

17.CONSOLIDATED BUSINESS RETURNS ARE NOT PERMITTED.

18.TAXES ARE TO BE PAID WITH RETURN.

19.THE COLLECTOR IS AUTHORIZED TO EXAMINE BOOKS, PAPERS, AND RECORDS OF ANY TAXPAYER TO VERIFY THE ACCURACY OF ANY RETURN.

20.SIGNATURE: Make sure that the signature section is properly completed and is legible. If someone other than the taxpayer prepared the return, they must also sign the return.

NOTICE

Taxes paid after due date, April 15th (Calendar Year) or 105 days after close of fiscal year are delinquent and lines

15 and 16 under “Section C – Computation of Tax” must be completed.

Website Address: www.stlouiscollector.com |

Telephone: (314) |

(REV. 11/12)

Document Specifics

| Fact Number | Description |

|---|---|

| 1 | All individuals, partnerships, LLCs, and corporations engaged in any form of business within the City of St. Louis must file the annual Earnings Tax Return, Form E-234, regardless of profit or loss. |

| 2 | Form E-234 and the total remittance, payable to Gregory F.X. Daly, must be filed at the Collector of Revenue, Earnings Tax Division, 1200 Market Street, Room 410, St. Louis, Missouri. |

| 3 | A calendar year return is due by April 15 of the following year, while fiscal year returns are due within 105 days after the fiscal year ends. |

| 4 | Late payments will incur a penalty of 5% of the tax amount per month (up to 25%) and an interest of 1% per month (12% per year) until the tax is paid. |

| 5 | Extensions to file Form E-234 can be requested using Form E-8, with estimated tax payments made prior to the original due date, but extensions to pay are not granted. |

| 6 | Incomplete, frivolous, illegible, or unsigned returns will be returned to the taxpayer, subject to penalties and interest if filed after the due date. |

| 7 | The form is governed by Chapter 5.22 of the Revised Code, City of St. Louis, 1980, making it a specific requirement for conducting business within city limits. |

Guide to Writing City Of St Louis Tax

Filling out the City Of St Louis Tax form, Form E-234, is a mandatory process for individuals and entities conducting any form of business within the City of St Louis, including residents with businesses outside the city. These instructions guide you through each necessary step, ensuring accuracy and compliance with the city's tax requirements. Prior to beginning, gather all relevant financial records and documents to streamline the process.

- Identify if you must file by reviewing the criteria outlined in "WHO MUST FILE" to determine if your activities require the submission of Form E-234.

- Prepare your payment made payable to Gregory F.X. Daly, ensuring it aligns with the total remittance amount due.

- Note the filing deadline under "FILING DATE" to ensure timely submission either by April 15th for the calendar year or within 105 days after your fiscal year ends.

- Consider any penalties and interest you may owe for late payments as per "PENALTY AND INTEREST" and calculate accordingly.

- If needed, request an extension using Form E-8 under "EXTENSIONS OF TIME TO FILE" prior to the due date, with an estimated tax payment included.

- Ensure all sections of the form are complete, marking any inapplicable sections with "N/A," as incomplete submissions will be returned.

- Provide your Taxpayer’s I.D. Number, using either your FEIN or SSN as applicable, at the designated spot on the form.

- Clearly fill in your name and address in the area provided.

- Indicate your business type, checking the appropriate line and completing the "Principal Business Activity" accordingly.

- Calculate the net profit or loss of your business in Section A as instructed, attaching supporting schedules or documents.

- In Section A-1, list or attach a breakdown of your business expense deductions, following the guidance for what to include from your Federal Return or other financial statements.

- Complete Section A-2 if claiming deductions for specific expenses like subcontracting fees or legal fees, listing all necessary details.

- Review the provisions for a resident business taxpayer under "RESIDENT BUSINESS TAXPAYER" to understand your tax obligations.

- If you are a non-resident with the sole store or office in St. Louis, note that you cannot allocate net profit as detailed under "SOLE STORE/OFFICE IS IN ST. LOUIS".

- Fill out the Section B worksheet if you are entitled to business allocation of taxable net profit, and attach any required documentation.

- Calculate your tax in Section C according to your taxable net profit, applying any earned payroll tax credits, and including penalty or interest if applicable.

- Ensure that consolidated business returns are not attempted, as per "CONSOLIDATED BUSINESS RETURNS ARE NOT PERMITTED".

- Remember to pay the taxes with your return submission, adhering to the instructions under "TAXES ARE TO BE PAID WITH RETURN".

- Sign the form, ensuring your signature is legible. If someone else prepared the form, they must also sign.

Once completed, review your form for accuracy and completeness before mailing it to the specified address. Late payments and submissions require additional calculation for penalties and interest. For any queries or further instructions, consider visiting the official website or contacting the provided telephone number.

Understanding City Of St Louis Tax

Frequently Asked Questions about the City Of St Louis Tax Form E-234

Who needs to file a City of St. Louis Earnings Tax Return (Form E-234)?

Any resident or non-resident individual, partnership, or corporation that maintains a business, professional office, branch office, warehouse, has inventory, or conducts any type of business activity, service, or operation within the City of St. Louis must file the Form E-234. This includes all forms of earnings such as profits from self-employment and all 1099-MISC Income.

Where and how can the City of St. Louis Earnings Tax Return be filed?

Completed returns and any payments should be made payable to Gregory F.X. Daly and sent to the Collector of Revenue, Earnings Tax Division, located at 1200 Market Street, Room 410, St. Louis, Missouri 63103-2841.

What is the deadline for filing Form E-234?

For returns based on a calendar year, the deadline is April 15th of the following year. If filing for a fiscal year, the return must be submitted within 105 days after the fiscal year closes.

Are there penalties for late filing or payment?

Yes, taxes not paid by the due date are subject to a penalty of 5% of the unpaid tax for each month or part of a month that the return is late, up to a maximum of 25%. Interest is also charged at a rate of 1% per month (or 12% per year) until the tax is paid in full. If an extension is granted but the prepaid tax is less than 90% of the total tax due, penalties and interest will be assessed on the unpaid amount.

Can I request an extension for filing the E-234 form?

Requests for an extension must be made before the original due date using Extension Form E-8, along with an estimated tax payment. All city taxes must be current to be granted an extension. It's important to note that an extension to file does not extend the payment deadline. Also, receiving a federal extension does not automatically extend the city filing requirement.

For more detailed assistance or if your question wasn't covered, please contact the Collector of Revenue's office or visit www.stlouiscollector.com.

Common mistakes

When individuals or businesses fill out the City of St. Louis Tax Form, common mistakes can often lead to unnecessary delays, penalties, or incorrect tax liabilities. Understanding and avoiding these errors can help ensure a smoother and more accurate tax filing process. Here are seven common mistakes:

- Not filing on time: Missing the April 15 deadline for calendar year returns or the 105-day deadline for fiscal year returns results in penalties and interest charges.

- Incorrect Taxpayer Identification Number: Failing to provide the correct Federal Employer Identification Number (FEIN) for employers or Social Security Number (SSN) for non-employers can delay processing.

- Incomplete Returns: Omitting schedules or not marking sections as "Not Applicable" (N/A) when they do not apply results in the return being returned to the taxpayer.

- Failing to Attach Required Documentation: Not attaching supporting schedules for items entered on Lines 2, 4, and 6 of Section A or the correct parts of the Federal Return when electing to attach it can lead to disallowed deductions.

- Incorrect Deduction Claims: Including non-allowable deductions such as Federal and State Income Taxes, City Earnings Tax, life insurance premiums, and incorrect calculations for meal and entertainment expenses can result in additional tax assessments.

- Improper Calculation of Net Profit Allocations: Failure to accurately complete the Section B worksheet or to provide proof of business locations when claiming allocations based on operations outside the City can lead to errors in tax calculation.

- Payments for Independent Contractors and Other Expenses: Not correctly filling out Section A-2 for payments over $1,000 to subcontractors and other specified service providers can result in the disallowance of these deductions.

Avoiding these mistakes involves careful review of the tax form instructions, ensuring all required information and documentation are complete, and understanding the specifics of allowable deductions and profit allocations. Consideration of these factors helps in accurately determining tax liabilities and avoiding potential penalties.

Documents used along the form

When dealing with taxes in the City of St. Louis, the primary form used is Form E-234, a comprehensive document designed for individuals, partnerships, and corporations engaged in business activities within the city. However, this form doesn't stand alone. To ensure full compliance with tax laws and regulations, and to maximize accuracy in tax reporting, taxpayers often find themselves needing additional forms and documents. Here's a look at some of these essential documents.

- Extension Form E-8: This document is crucial for any taxpayer who anticipates needing more time to file their E-234 form. It is not, however, a means to delay payment. Timely payment of estimated taxes is required, and this form must be filed before the original due date to avoid penalties.

- Federal Tax Return: Copies of the taxpayer's federal tax return and schedules can be attached to the E-234 form to support figures entered, especially in the net profit or loss section. This includes, but is not limited to, Schedule C for sole proprietors, Schedule K for partnerships, and the first page of Form 1120 for corporations.

- W-2 and 1099 Forms: These documents report income from employment and miscellaneous income, respectively. They are essential for accurately reporting earnings and for substantiating entries on the E-234 form, particularly for taxpayers with diverse sources of income.

- Schedule A-2 Supporting Documentation: For the deductions listed under Section A-2 of the E-234 form, detailed documentation including invoices and contracts may be required. This supports deductions for subcontracting, professional fees, and other specified categories.

- Allocation Worksheets: Businesses that operate both within and outside of St. Louis may need to complete additional worksheets for the allocation of net profit. These documents help determine what portion of income is subject to city taxes based on property value, gross receipts, and wages.

- Proof of Extension for Federal Taxes: Although a federal extension does not extend the city tax filing deadline, proof of such an extension may be required for taxpayers who have also applied for a St. Louis city tax extension. This ensures that all tax obligations are transparent and accounted for.

Collectively, these documents work in tandem with the City of St. Louis Tax Form E-234 to paint a complete picture of a taxpayer's obligations and contributions to the city's fiscal health. While the tax form itself captures the essence of one's taxable activities, the supporting documents and forms are indispensable in fulfilling the legal and procedural aspects of tax filing. This careful documentation ensures compliance, aids in accurate tax calculation, and helps in avoiding penalties for underpayment or late filing.

Similar forms

The City of St. Louis Earnings Tax form shares similarities with the IRS Form 1040, used for individual income tax filing. Both require taxpayers to report their annual income, calculate deductions, and determine the tax owed or refund due. They cater to different tax structures—federal versus city—but fundamentally serve the purpose of ensuring taxpayers contribute to public funds according to their income levels. Each form mandates reporting of various types of income, such as wages, commissions, and capital gains, and allows for certain deductions and credits to calculate net tax liability.

Similar to the Schedule C (Profit or Loss from Business) form utilized by sole proprietors filing with the IRS, the City of St. Louis form requires detailed reporting of business income and expenses. Both forms are designed to calculate the net profit or loss from business operations, requiring supporting documentation for revenue and deductible expenses. However, while Schedule C is for federal tax purposes, detailing the specifics of business financial activity for income tax assessment, the City form specifically addresses earnings within St. Louis, highlighting the local tax obligations of business activities.

The City of St. Louis Tax form and the IRS Form 1120 (U.S. Corporation Income Tax Return) are paralleled through their requirement for corporations to report income, deductions, and compute their taxes due. Both documents are tailored to entities structured as corporations, focusing on their unique aspects of taxation, such as dividends and corporate profits. The key difference lies in their scope, with Form 1120 addressing federal taxes while the City of St. Louis form focuses on local earnings tax obligations.

This form also bears resemblance to the IRS Form 1065, used for partnership returns. Both require financial disclosures of partnerships, including income, losses, and deductions. They are structured to provide a comprehensive view of a partnership’s financial status for tax assessment purposes but differ in their tax jurisdiction—Form 1065 at a federal level and the City of St. Louis form for local tax obligations. The allocation of net profit and the reporting of partnership income are essential elements for both, illustrating their intent to tax entities based on their operational earnings.

The City of St. Louis Earnings Tax form and the IRS Form 1099-MISC share a common ground in reporting miscellaneous income, including fees, commissions, royalties, and rent. These forms are integral to tracking income that may not be subject to regular withholding taxes, ensuring that all earnings are accounted for in tax assessments. While Form 1099-MISC serves to inform the IRS and taxpayers about miscellaneous income at a federal level, the City of St. Louis form captures this information within the scope of city taxes, emphasizing the comprehensive inclusion of all income sources for accurate tax liability determination.

Dos and Don'ts

Filing your City of St. Louis Tax Form correctly is crucial to avoid unnecessary penalties, interest charges, or errors in your tax obligations. Here are seven guidelines to help you navigate the process efficiently and accurately.

- Do: Ensure all schedules are completed or marked as "Not Applicable" (N/A). Incomplete returns can lead to delays and potential penalties.

- Don't: Ignore the specific instructions regarding attachments to your return. For instance, attaching unnecessary documents can complicate the review process. Only include the specific schedules and documents requested.

- Do: Report all required types of income, including commissions, fees, and other taxable earnings as outlined under Section A — Net Profit (Or Loss).

- Don't: Attempt to claim non-allowable deductions such as contributions, life insurance premiums, or federal and state income taxes. Stick to the deductible expenses as delineated in the form.

- Do: Accurately complete the Section B Worksheet if your business qualifies for tax apportionment or allocation, based on business activities both within and outside the City of St. Louis.

- Don't: Forget to sign your form. An unsigned return is considered incomplete and can result in the form being returned to you, possibly incurring penalties and interest if resubmitted past the due date.

- Do: Make your payment to Gregory F.X. Daly, Collector of Revenue, and ensure your remittance accompanies your tax return form to avoid delinquency.

By adhering to these do's and don'ts, taxpayers can streamline their filing process, comply with local tax laws, and mitigate the risk of penalties. Always refer to the most current instruction sheet provided by the City of St. Louis Collector of Revenue's office to keep abreast of any changes or updates to the tax filing requirements.

Misconceptions

Understanding the City of St. Louis Tax Form E-234 can be complex, and there are several misconceptions people often have about this document. Clarification of these misconceptions can help taxpayers better navigate their tax obligations in the City of St. Louis.

Misconception #1: Only businesses operating physically within the City of St. Louis need to file Form E-234. In reality, this form must be filed by any individual, partnership, or corporation conducting any form of business or professional activity within the city limits, regardless of their physical office location.

Misconception #2: 1099-MISC Income is exempt from being reported on Form E-234. Contrary to this belief, all 1099-MISC Income must be reported on Form E-234, reflecting the city’s broad definition of taxable earnings.

Misconception #3: Extensions for filing automatically extend the payment due date. Requesting an extension only prolongs the filing deadline; it does not grant additional time to pay the tax due. Taxes not paid by the original due date will accrue penalties and interest.

Misconception #4: A Federal Extension also extends the city tax filing deadline. Although you may receive a federal extension, a separate request must be submitted for the City of St. Louis to extend the filing deadline for Form E-234.

Misconception #5: Capital losses can offset other income forms for city earnings tax purposes. Unlike federal tax guidelines, the City of St. Louis does not allow operating loss carryovers or carrybacks to be applied against earnings, making capital losses unable to offset other taxable income.

Misconception #6: All business expenses are deductible on Form E-234. The form stipulates specific non-allowable deductions, such as federal and state income taxes, life insurance premiums, and 50% of meal and entertainment expenses. Compliance with these regulations is necessary to avoid disallowed deductions and additional taxes.

Misconception #7: Non-resident businesses without a physical presence in St. Louis are not required to file or allocate earnings. Regardless of physical presence, non-resident businesses must file Form E-234 and are entitled to apportion their net profits based on business conducted within the city.

Misconception #8: Taxpayers can freely choose their method of profit allocation without prior approval. An alternative profit allocation method must be approved by the Collector of Revenue before submitting the return. This ensures that all allocations are properly validated and meet city criteria.

Misconception #9: Consolidated business returns are allowed for entities with multiple business operations. Each entity or division that meets the city’s filing criteria must submit an individual Form E-234, as consolidated business returns are not permitted.

Understanding these common misconceptions and accurately completing the City of St. Louis Tax Form E-234 can help taxpayers avoid errors, penalties, and interest charges, ensuring compliance with local taxation requirements.

Key takeaways

Filling out and using the City of St. Louis Tax Form, known as Form E-234, is crucial for residents, non-residents, and businesses engaged in financial activities within the city. Here are seven key takeaways to guide you through the process:

- Every individual or entity doing business within St. Louis, regardless of their profit or loss status, must file Form E-234. This includes residents with businesses outside the city as well as various forms of partnerships and corporations.

- All forms along with the total payment should be directed to the Collector of Revenue, Earnings Tax Division, located at 1200 Market Street, Room 410, St. Louis, Missouri 63103-2841. Payments should be made out to Gregory F.X. Daly.

- The deadline for filing is April 15 for calendar year returns and 105 days after the close of the fiscal year for others. It's important to file on time to avoid penalties, which include a 5% penalty per month for late taxes, plus interest.

- If more time is needed to file, requests for extension must be made before the due date using Form E-8. However, an extension to file does not extend the time to pay owed taxes.

- Ensure completeness and accuracy in your return to avoid it being returned. This includes filling out all schedules or marking them as “Not Applicable” (N/A) and remembering to sign the form.

- For non-resident businesses that operate both within and outside of St. Louis, an allocation or apportionment of net profits may be claimed, which requires complete documentation and potentially an alternative method approved by the Collector of Revenue.

- Finally, taxes are due with the return and must be paid in order to avoid interest and penalties. It's also essential to complete the payment, signature, and any accompanying documentation accurately to ensure your form is processed efficiently.

Following these guidelines will help streamline the filing process and ensure compliance with the City of St. Louis's tax requirements. For further details or assistance, the Collector of Revenue's office can be contacted directly.

Popular PDF Documents

IRS 1098 - Merging tax planning with the details provided on your 1098 forms can lead to significant savings during tax season.

Form 1095 a - It's particularly important for families, as it outlines coverage for each family member and assists in calculating the household’s overall health insurance expenses.