Get Annual Income Tax Return 1701 Form

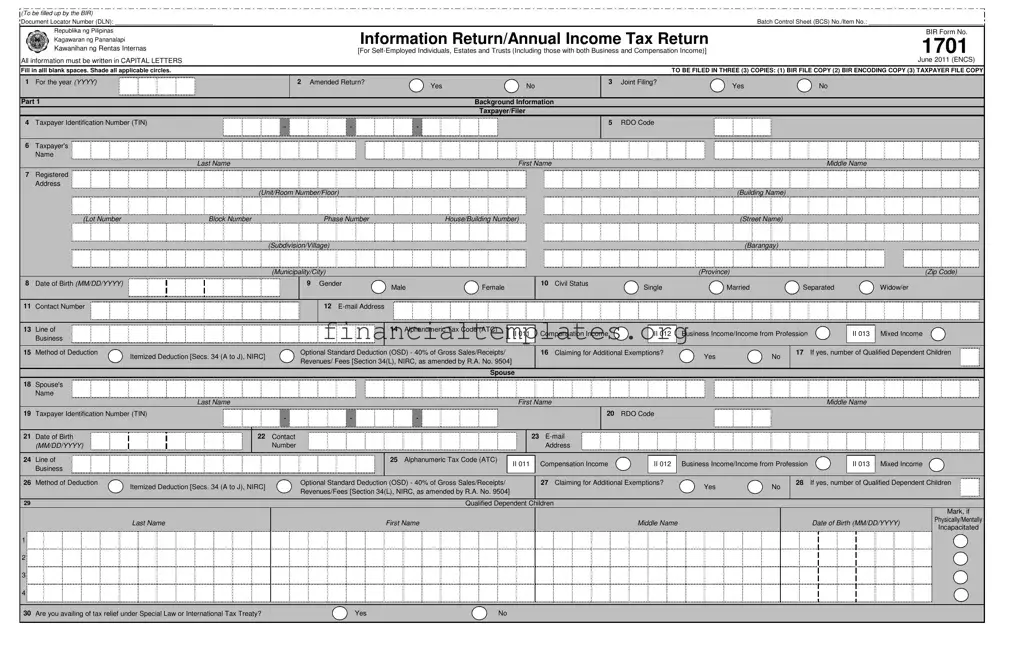

The Annual Income Tax Return 1701 form is a crucial document for self-employed individuals, estates, and trusts in the Philippines, including those with both business and compensation income. Mandated by the Bureau of Internal Revenue (BIR), this form is designed to facilitate the declaration and computation of annual income tax due. It requires comprehensive information, such as taxpayer identification, registered address, taxable income breakdown, the method of deduction preferred, and tax credits or payments. The form offers options for itemized or optional standard deductions, as well as provisions for claiming additional exemptions. Detailed sections guide filers through the computation of tax—including regular, special rates, and total income tax due—while ensuring tax relief under special laws or international tax treaties are applied where eligible. Taxpayers must prepare three copies, submitting them to respective BIR offices and keeping one for their records, reflecting the importance of accuracy and compliance in tax filing. It serves as a testament to the government's efforts in streamlining tax collection processes, thus facilitating a more efficient fiscal system that holds individuals and entities accountable for their share in nation-building.

Annual Income Tax Return 1701 Example

|

(To be filled up by the BIR) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Document Locator Number (DLN): _____________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Batch Control Sheet (BCS) No./Item No.: __________________________________ |

|||||||||||||||||||||||||

|

|

Republika ng Pilipinas |

|

|

|

|

|

|

|

|

|

|

|

|

|

Information Return/Annual Income Tax Return |

|

|

|

|

|

|

|

|

|

|

|

BIR Form No. |

|||||||||||||||||||||||||||

|

|

Kagawaran ng Pananalapi |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1701 |

|

|||||||||||||||||||||||||||

|

|

Kawanihan ng Rentas Internas |

|

|

|

|

|

|

|

|

|

|

|

[For |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

All information must be written in CAPITAL LETTERS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

June 2011 (ENCS) |

||||||||

|

Fill in alll blank spaces. Shade all applicable circles. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TO BE FILED IN THREE (3) COPIES: (1) BIR FILE COPY (2) BIR ENCODING COPY (3) TAXPAYER FILE COPY |

|||||||||||||||||||||||

|

1 |

For the year (YYYY) |

|

|

|

|

|

|

|

|

|

|

2 Amended Return? |

|

|

|

Yes |

|

|

No |

|

3 |

Joint Filing? |

|

|

|

|

Yes |

|

|

|

|

No |

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Part 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Background Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer/Filer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

4 |

Taxpayer Identification Number (TIN) |

|

|

|

|

|

- |

|

|

|

|

- |

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

5 |

RDO Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Taxpayer's |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

|

|

|

Middle Name |

|

|

|

|

|

|

||||||||||||||

|

7 |

Registered |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Unit/Room Number/Floor) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Building Name) |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

(Lot Number |

|

|

|

Block Number |

|

|

Phase Number |

|

|

|

House/Building Number) |

|

|

|

|

|

|

|

|

|

|

(Street Name) |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

(Subdivision/Village) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Barangay) |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

(Municipality/City) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Province) |

|

|

|

|

|

|

|

|

|

|

(Zip Code) |

||||||||||||||

|

8 |

Date of Birth (MM/DD/YYYY) |

|

|

|

|

|

|

|

|

|

9 Gender |

Male |

|

Female |

|

|

|

|

10 Civil Status |

Single |

|

|

|

|

Married |

|

|

Separated |

Widow/er |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Contact Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

13 |

Line of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Alphanumeric Tax Code (ATC) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

II 011 |

|

Compensation Income |

|

II 012 |

Business Income/Income from Profession |

|

|

II 013 |

Mixed Income |

|||||||||||||||||||||||||

|

|

Business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

15 |

Method of Deduction |

Itemized Deduction [Secs. 34 (A to J), NIRC] |

Optional Standard Deduction (OSD) - 40% of Gross Sales/Receipts/ |

|

|

|

|

16 Claiming for Additional Exemptions? |

|

Yes |

|

|

No |

17 |

If yes, number of Qualified Dependent Children |

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

Revenues/ Fees [Section 34(L), NIRC, as amended by R.A. No. 9504] |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

18 |

Spouse's |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

|

|

|

Middle Name |

|

|

|

|

|

|

||||||||||||||

|

19 |

Taxpayer Identification Number (TIN) |

|

|

|

|

|

- |

|

|

|

|

- |

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

20 |

RDO Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

21 |

Date of Birth |

|

|

|

|

|

|

|

|

22 Contact |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

(MM/DD/YYYY) |

|

|

|

|

|

|

|

|

Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

24 |

Line of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 Alphanumeric Tax Code (ATC) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

II 011 |

|

Compensation Income |

|

II 012 |

Business Income/Income from Profession |

|

|

II 013 |

Mixed Income |

|||||||||||||||||||||||||

|

|

Business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

26 |

Method of Deduction |

Itemized Deduction [Secs. 34 (A to J), NIRC] |

Optional Standard Deduction (OSD) - 40% of Gross Sales/Receipts/ |

|

|

|

|

27 Claiming for Additional Exemptions? |

|

Yes |

|

|

No |

28 |

If yes, number of Qualified Dependent Children |

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

Revenues/Fees [Section 34(L), NIRC, as amended by R.A. No. 9504] |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

29 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qualified Dependent Children |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mark, if |

||

|

|

|

|

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Name |

|

|

|

|

|

|

|

|

Middle Name |

|

|

|

|

Date of Birth (MM/DD/YYYY) |

Physically/Mentally |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Incapacitated |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2

3

4

|

|

|

|

|

30 Are you availing of tax relief under Special Law or International Tax Treaty? |

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

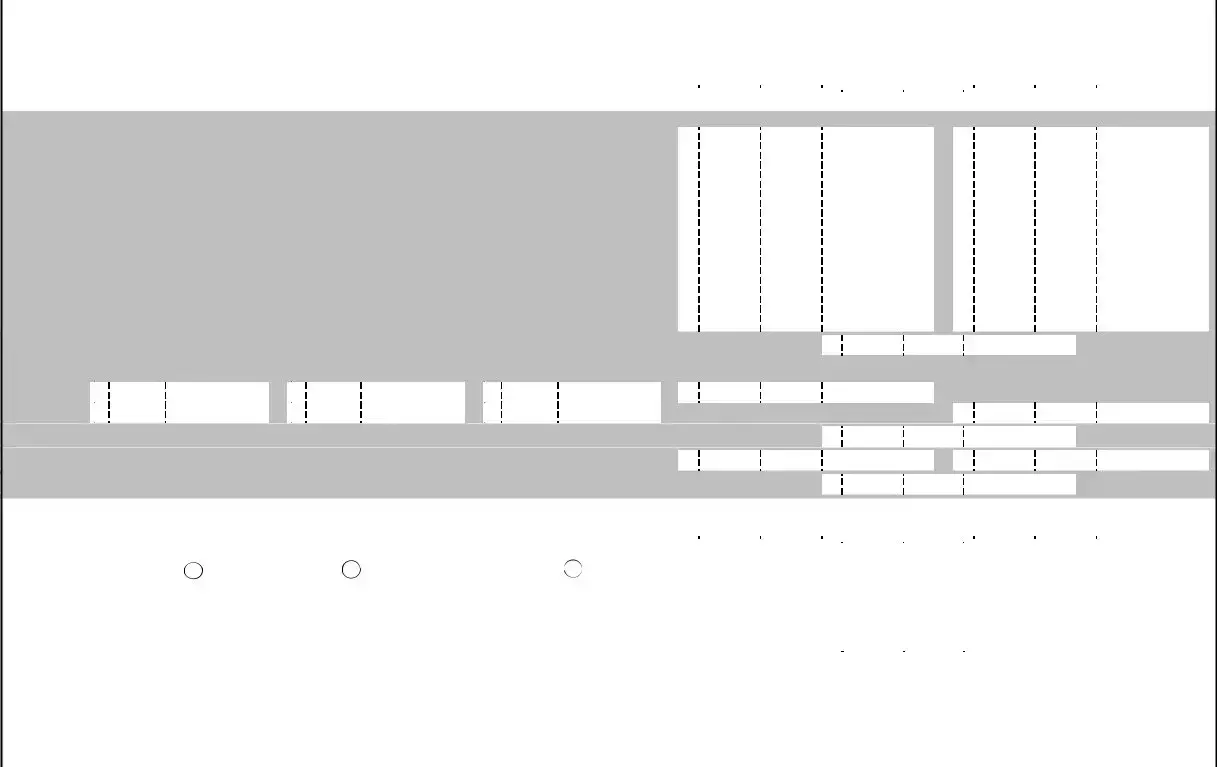

BIR Form No. 1701 - page 2 |

||

Part II |

Computation of Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer/Filer |

|

|

|

|

Spouse |

||||||

31 |

Income Tax Due under Regular Rate (from Item 69C/ 69D of Part V) |

31A |

|

|

|

|

• |

31B |

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

32 |

Add: Income Tax Due under Special Rate (from Item 69A/ 69B of Part V) |

32A |

|

|

|

|

• |

32B |

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

33 |

Total Income Tax Due (Sum of Items 31A & 32A/ 31B & 32B) |

33A |

|

|

|

|

33B |

|

|

|

|

|

|

|||

|

|

|

|

• |

|

|

|

|

|

• |

|

|||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

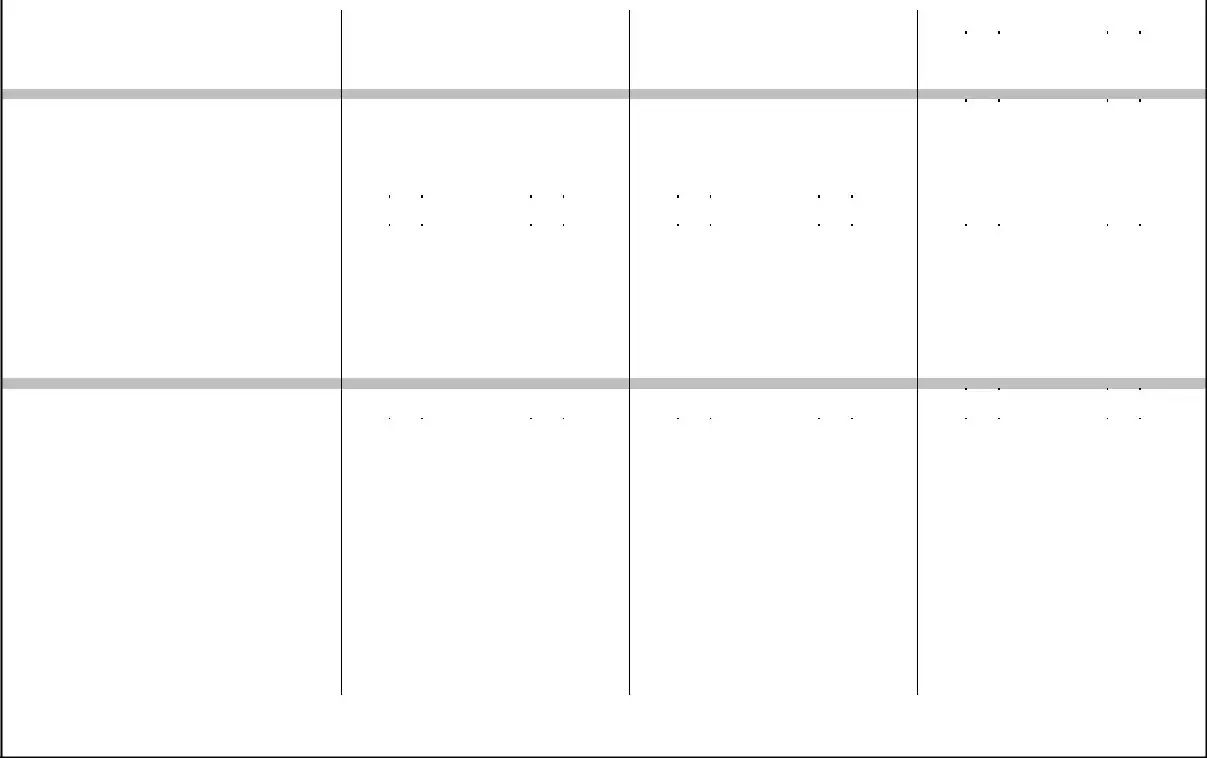

34 |

Aggregate Income Tax Due (Sum of Item 33A & 33B) |

|

34 |

|

|

|

|

|

|

• |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||||||

35Less: Tax Credits/Payments (attach proof)

|

35A/B Prior Year's Excess Credits |

|

|

|

|

|

35A |

• |

35B |

• |

|

|

|

|

|

|

|

|

|

|

|

||

|

35C/D Tax Payment for the First Three Quarters |

|

|

|

|

|

35C |

• |

35D |

• |

|

|

|

|

|

|

|

|

|

|

|

||

|

35E/F Creditable Tax Withheld for the First Three Quarters |

|

|

|

|

35E |

• |

35F |

• |

||

|

|

|

|

|

|

|

|

|

|

||

|

35G/H Creditable Tax Withheld per BIR Form No. 2307 for the 4th Quarter |

|

|

|

35G |

• |

35H |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

|

35I/J Tax withheld per BIR Form No. 2316 |

|

|

|

|

|

35I |

• |

35J |

• |

|

|

|

|

|

|

|

|

|

|

|

||

|

35K/L Tax Paid in Return Previously Filed, if this is an Amended Return |

|

|

|

35K |

• |

35L |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

|

36M/N Foreign Tax Credits |

|

|

|

|

|

35M |

• |

35N |

• |

|

|

|

|

|

|

|

|

|

|

|

||

|

35O/P Other Payments/Credits, specify____________________________ |

|

|

|

35O |

• |

35P |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

|

35Q/R Total Tax Credits/Payments (Sum of Items 35A, C, E, G, I, K, M & O/ 35B, D, F, H, J, L, N & P) |

|

|

|

35Q |

• |

35R |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

36 |

Net Tax Payable/(Overpayment) (Item 33A less 35Q/ 33B less 35R) |

|

|

|

36A |

• |

36B |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

37 |

Aggregate Tax Payable/(Overpayment) (Sum of Item 36A & 36B) |

|

|

|

|

|

37 |

|

• |

||

|

|

|

|

|

|

|

|

|

|

|

|

38 |

Add: Penalties |

|

|

|

|

|

|

|

|

|

|

|

Taxpayer/Filer |

38A |

• |

38B |

• |

38C |

• |

38D |

• |

|

|

|

|

|

|

|

|

|

|

||||

|

Spouse |

38E |

• |

38F |

• |

38G |

• |

|

|

38H |

• |

|

|

|

|

|

|

|

|

||||

39 Aggregate Penalties (Sum of Item 38D & 38H) |

|

|

|

|

|

|

39 |

|

• |

||

|

|

|

|

|

|

|

|

|

|

|

|

40 |

Total Amount Payable/(Creditable/Refundable)(Sum of Item 36A & 38D/ 36B & 38H) |

|

|

|

40A |

• |

40B |

• |

|||

|

|

|

|

|

|

|

|

|

|

||

41 |

Aggregate Amount Payable/(Creditable/Refundable)(Sum of Item 40A & 40B) |

|

|

|

|

41 |

|

• |

|||

|

|

|

|

|

|

|

|

|

|

|

|

42 |

Less Portion of Tax Payable Allowed for 2nd Installment Payment to be paid on or before July 15(not less than 50% of Item 33A/ 33B) |

|

|

42A |

|

|

|

|

|

|

|

• |

42B |

|

|

|

|

|

|

• |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

43 |

Amount of Tax Required to be Paid Upon Filing this Return(Item 40A less 42A/ 40B less 42B) |

|

|

|

|

43A |

|

|

|

|

|

|

|

• |

43B |

|

|

|

|

|

|

• |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

44 |

Net Aggregate Amount of Tax Required to be Paid/(Creditable/Refundable) Upon Filing of this Return(Sum of Item 43A & 43B) |

44 |

|

|

|

|

|

|

|

|

• |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

If overpayment, mark one box only: |

To be Refunded |

To be issued a Tax Credit Certificate (TCC) |

To be carried over, as tax credit for the next year/quarter |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Part III |

|

|

|

|

|

Availment of Tax Income Incentives/Exemptions |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer/Filer |

|

|

|

|

|

|

|

|

Spouse |

|

|||

45 |

Total Tax Relief/Savings (from Item 98J/ 98K of Part VII) |

|

|

|

|

45A |

|

|

|

|

|

|

|

• |

45B |

|

|

|

|

|

|

• |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

46 |

Aggregate Amount of Tax Relief/Savings (Sum of Item 45A & 45B) |

|

|

46 |

|

|

|

|

|

|

|

|

• |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part IV |

|

|

|

|

|

Details of Payment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stamp of Receiving Office/AAB and Date of Receipt |

|

|||||

|

Particulars |

|

|

Drawee Bank/Agency |

|

|

Number |

|

Date (MM/DD/YYYY) |

|

|

|

|

Amount |

|

|

|

|

|

(RO's Signature/Bank Teller's Initial) |

|

||||||||

47 |

Cash/Bank |

47A |

|

|

47B |

|

|

47C |

|

|

|

|

|

47D |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Debit Memo |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

48 |

48A |

|

|

48B |

|

|

48C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check |

|

|

|

|

|

|

|

|

|

48D |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

49 |

Tax Debit Memo |

|

|

|

49A |

|

|

49B |

|

|

|

|

|

49C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

50 |

Others |

50A |

|

|

50B |

|

|

50C |

|

|

|

|

|

50D |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BIR Form No. 1701 - page 3 |

|||||

Part V |

Breakdown of Income (attach additional sheet/s, if necessary) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

E X E M P T |

S P E C I A L R A T E |

|

|

|

|

|

R E G U L A R R A T E |

|||||||

|

Taxpayer/Filer |

Spouse |

Taxpayer/Filer |

Spouse |

|

|

Taxpayer/Filer |

|

|

|

Spouse |

|||||

51 |

Gross Compensation Income (from Schedule 1) |

|

|

|

51A |

|

|

|

• |

51B |

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||||

52 |

Less: |

|

|

|

52A |

|

|

|

52B |

|

|

|

|

|

||

|

|

|

|

|

|

• |

|

|

|

|

• |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

53 |

Gross Taxable Compensation Income (Item 51A less 52A/ 51B less 52B) |

|

|

|

53A |

|

|

|

53B |

|

|

|

|

|

||

|

|

|

|

|

|

• |

|

|

|

|

• |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

54Less: Deductions

|

54A/B |

Premium on Health and/or Hospitalization Insurance (not to exceed P 2,400/year) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54A |

|

|

• |

54B |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

54C/D |

Personal Exemption/Exemption for Estate and Trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54C |

|

|

54D |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

• |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

54E/F |

Additional Exemption |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54E |

|

|

54F |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

• |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

54G/H Total Deductions (Sum of Items 54A, C & E/ 54B, D & F) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54G |

|

|

54H |

|

|

|

||||

55 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

• |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Total Compensation Income/(Excess of Deductions) (Item 53A less 54G/ 53B less 54H) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

55A |

|

|

55B |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

• |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

56 |

Sales/Revenues/Receipts/Fees (net of sales returns, allowances and discounts) |

56A |

|

|

|

56B |

|

|

|

56C |

|

|

|

56D |

|

|

|

56E |

|

|

56F |

|

|

|

||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

57 |

Add: Other Taxable/Exempt Income from Operations, not subject to Final Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

57A/B/C/D/E/F |

|

57A |

|

|

• |

57B |

|

|

• |

57C |

|

|

• |

57D |

|

|

• |

57E |

|

|

• |

57F |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

57G/H/I/J/K/L |

|

57G |

|

|

57H |

|

|

57I |

|

|

57J |

|

|

57K |

|

|

57L |

|

|

|

|||||||

|

|

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

58 |

57M/N/O/P/Q/R Total (Sum of Item 57A & 57G/ 57B & 57H/ 57C & 57I/ 57D & 57J/ 57E & 57K/ 57F & 57L) |

57M |

|

|

• |

57N |

|

|

• |

57O |

|

|

• |

57P |

|

|

• |

57Q |

|

|

• |

57R |

|

|

• |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Total Sales/Revenues/Receipts/Fees (SUM OF ITEM 56A & 57M/ 56B & 57N/ 56C & 57O/ 56D & 57P/ 56E & 57Q/ 56F & 57R) |

58A |

|

|

58B |

|

|

58C |

|

|

58D |

|

|

58E |

|

|

58F |

|

|

|

|||||||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

59 |

Less: Cost of Sales/Services |

59A |

|

|

59B |

|

|

59C |

|

|

59D |

|

|

59E |

|

|

59F |

|

|

|

||||||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

60 |

Net Sales/Revenues/Receipts/Fees (Item 58 less 59) |

60A |

|

|

60B |

|

|

60C |

|

|

60D |

|

|

60E |

|

|

60F |

|

|

|

||||||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

61 |

Add: |

61A |

|

|

61B |

|

|

61C |

|

|

61D |

|

|

61E |

|

|

61F |

|

|

|

||||||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

62 |

Gross Income (Sum of Item 60 & 61) |

62A |

|

|

62B |

|

|

62C |

|

|

62D |

|

|

62E |

|

|

62F |

|

|

|

||||||||

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

|

• |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

63Less: Deductions

|

63A/B |

Optional Standard Deduction (OSD) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

63A |

|

|

|

• |

|

63B |

|

|

|

• |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

OR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

63C/D/E/F/G/H Regular Allowable Itemized Deductions |

|

|

63C |

|

|

• |

63D |

|

|

• |

63E |

|

|

|

• |

|

63F |

|

|

|

• |

|

63G |

|

|

|

• |

|

63H |

|

|

|

• |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Special Allowable Itemized Deductions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Description |

Legal Basis |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

63I/J/K/L/M/N |

|

|

|

|

63I |

|

|

• |

63J |

|

|

• |

63K |

|

|

|

• |

|

63L |

|

|

|

• |

|

63M |

|

|

|

• |

|

63N |

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

63O/P/Q/R/S/T |

|

|

|

|

63O |

|

|

• |

63P |

|

|

• |

63Q |

|

|

|

• |

|

63R |

|

|

|

• |

|

63S |

|

|

|

• |

|

63T |

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

63U/V/W/X/Y/Z Allowance for NOLCO (from Item 83) |

|

|

63U |

|

|

• |

63V |

|

|

• |

63W |

|

|

|

• |

|

63X |

|

|

|

• |

|

63Y |

|

|

|

• |

|

63Z |

|

|

|

• |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

63AA/AB/AC/AD/AE/AF Total Allowable Itemized Deductions (Sum of Items 63C, I, O & U/ 63D, J, P & V |

63AA |

|

|

• |

63AB |

|

|

• |

63AC |

|

|

|

• |

|

63AD |

|

|

|

• |

|

63AE |

|

|

|

• |

|

63AF |

|

|

|

• |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

63E, K, Q & W/ 63F, L, R & X/ 63G, M, S & Y/ 63H, N, T & Z) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

64 |

Net Income |

(Item 62A less 63AA/ 62B less 63AB/ 62C less 63AC/ 62D less 63AD/ |

|

64A |

|

|

• |

64B |

|

|

• |

64C |

|

|

|

• |

|

64D |

|

|

|

• |

|

64E |

|

|

|

• |

|

64F |

|

|

|

• |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

62E less 63AE/ 62F less 63AF) (to Item 90 of Part |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

65 |

Less: Excess of Deductions over Taxable Compensation Income (FROM ITEM 55A/55B) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

65A |

|

|

|

• |

|

65B |

|

|

|

• |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

OR the Total Deductions (FROM ITEM 54G/54H) , if there is no Compensation Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

66 |

Taxable/Exempt Business Income/Income from Profession (Item 64 less 65) |

|

66A |

|

|

• |

66B |

|

|

• |

66C |

|

|

|

• |

|

66D |

|

|

|

• |

|

66E |

|

|

|

• |

|

66F |

|

|

|

• |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

67 |

Total Taxable Income (Sum of Item 55 & 66) |

|

|

67A |

|

|

• |

67B |

|

|

• |

67C |

|

|

|

• |

|

67D |

|

|

|

• |

|

67E |

|

|

|

• |

|

67F |

|

|

|

• |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

68 |

Applicable Tax Rate (i.e. special/regular rate) |

|

|

|

|

|

|

|

|

|

|

|

|

68A |

• |

% |

|

|

68B |

• |

% |

|

|

68C |

• |

% |

|

|

68D |

• |

% |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|